The new federal housing plan

Ever since polling numbers collapsed last summer, the federal government has been on a speedrun to reverse the (arguably well justified) perception that they have done a disastrous job on housing. Though I would argue...

New listings have been on a tear in April, and it’s worth looking at what might be behind the increase. Ever since rates jumped two years ago and people started facing huge increases in their...

Ever since polling numbers collapsed last summer, the federal government has been on a speedrun to reverse the (arguably well justified) perception that they have done a disastrous job on housing. Though I would argue...

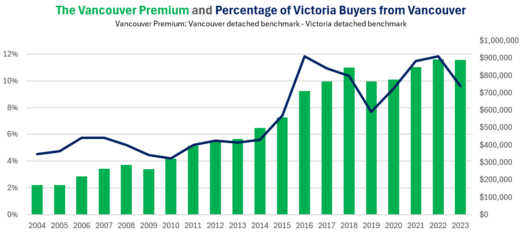

After 6+ years of price stagnation following the Great Financial Crisis, two things turned the market around in 2014/15: the improvement of affordability from years of dropping rates and rising incomes, and the start of...

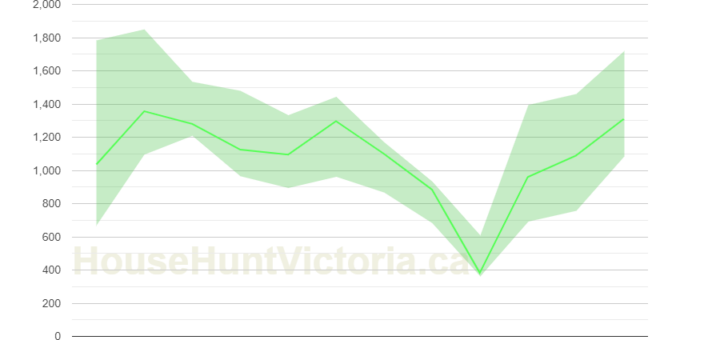

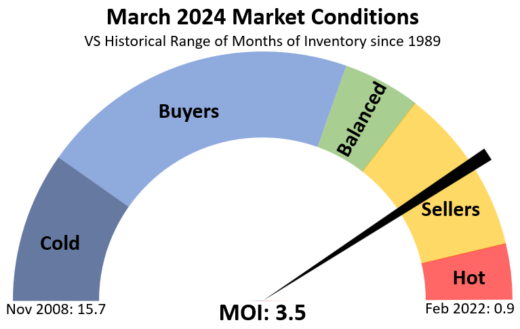

It’s the start of the spring market, and so far it’s a little lacklustre. Sales in March came in exactly where they were a year ago, which is a relative level they’ve been stuck at...

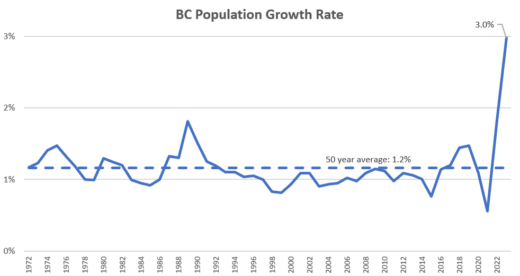

Much has been written about the surge in population growth in recent years, and indeed year over year growth in B.C. has spiked to levels that we have not seen in many decades. Many have...

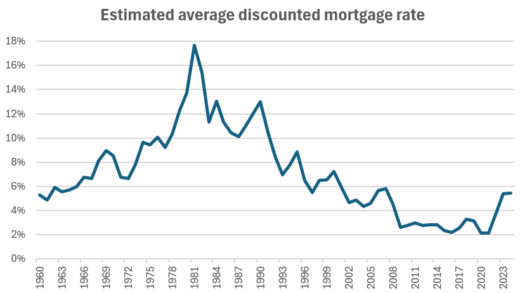

From 1981 to 1991, interest rates dropped by 43%. From 1991 to 2001, interest rates dropped by 42%. From 2001 to 2011, interest rates dropped by 54%. From 2011 to 2021, interest rates dropped by...

A while back Gregor Craigie (local CBC radio host and author) reached out to discuss my take on some of the root causes of the housing crisis. We’d discussed some aspects before on his show...

The leap year saved the market from year over year sales declines, with 29 sales reported on the 29th bringing us to 470 total for February, just 10 over the year ago figures. So...

It’s election season and that means the vote-buying goodies are starting to flow. First time buyers have long been able to get a break on the property transfer tax, but the purchase price limit of...

The median condo went for $540,500 in January, which is down from a very short-lived peak of around $600k in the spring of 2022. Outside of that market mania, prices haven’t really moved since late...

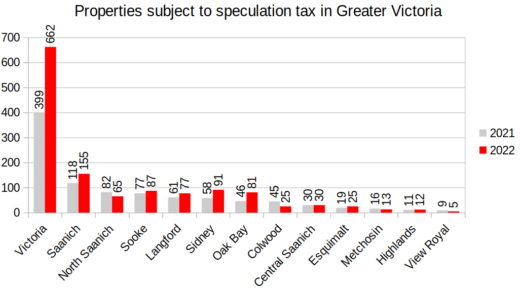

The province recently released new data on the Speculation and Vacancy Tax, and it showed that 1328 people in the CRD paid it last year (for the 2022 tax year), up from 971 the year...

Recent Comments