The non-permanent residents

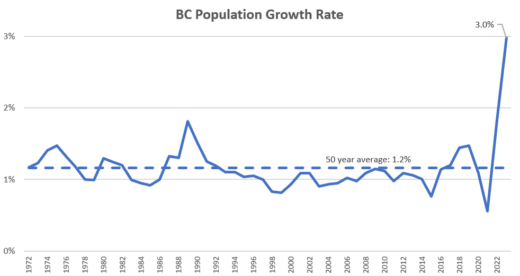

Much has been written about the surge in population growth in recent years, and indeed year over year growth in B.C. has spiked to levels that we have not seen in many decades. Many have...

Much has been written about the surge in population growth in recent years, and indeed year over year growth in B.C. has spiked to levels that we have not seen in many decades. Many have...

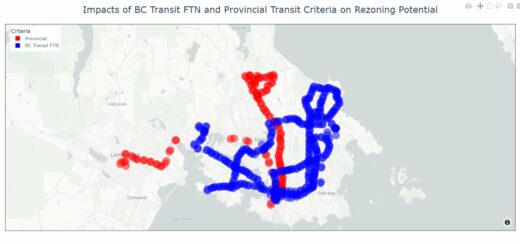

2023 has been a momentous year in housing policy at the provincial level. More has changed this year on the housing front than did in the past 40, and it’s getting quite confusing to keep...

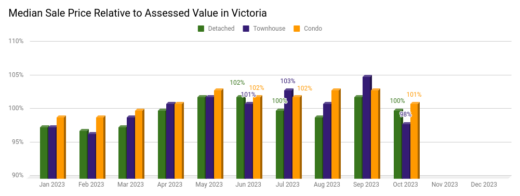

It’s been an eventful month for the housing market both in Victoria and the broader regulatory landscape in the province. In Victoria rates have continued to suppress activity, while the province dropped two bombshells, one...

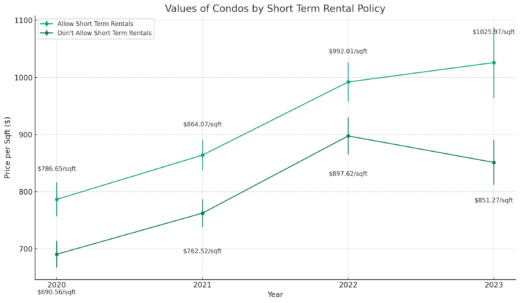

Last week the provincial government brought in broad new restrictions on short term rentals, defining minimum standards on what’s legal, unveiling new strategies for enforcement, and most surprisingly, ending the practice of grandfathering for short...

March is a wrap, and the situation remained substantially the same as in February. Sales are still historically slow for this time of year, but sellers are uninterested in playing ball with new listings trailing...

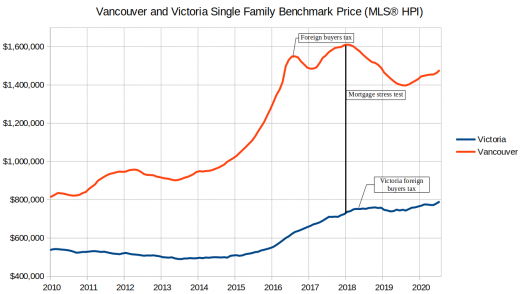

This weekend I read an article by Dr. Joshua Gordon in the Globe and Mail arguing that the focus on housing supply is a red herring, and demand stoked by foreign buyers, cheap credit, and...

This post is 4 years old. The data and my views may have since evolved.Since it’s all Coronavirus all the time on the blog these days, here’s a closer look at how the situation may...

This post is 4 years old. The data and my views may have since evolved.BC Assessment has released their previews of assessments for the year, and the media has jumped on them to make breathless...

This post is 5 years old. The data and my views may have since evolved.Another month another rent report from the folks at Padmapper and of course the requisite spinoff articles in the media about...

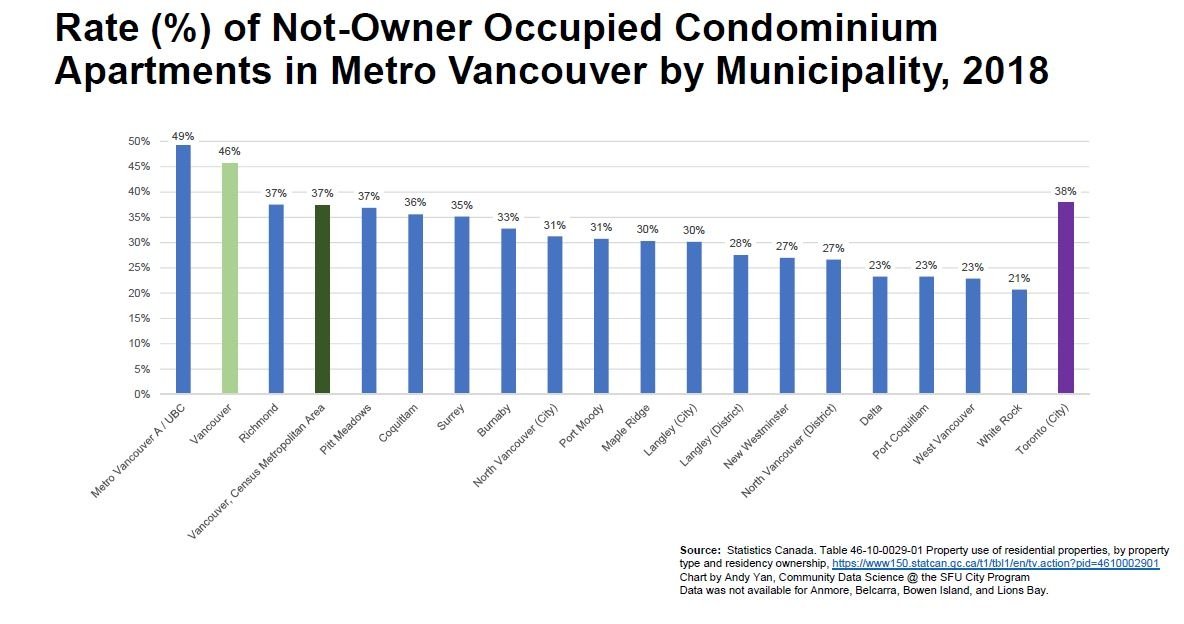

This post is 5 years old. The data and my views may have since evolved.There’s a study out by SFU’s City Program that has been getting some media coverage lately. In it, Andy Yan examined...