How often do owners move?

There was an interesting article in the Globe & Mail recently trying to back the claim that Canadians move approximately every 7 years. They do some digging into where that figure came from and test...

There was an interesting article in the Globe & Mail recently trying to back the claim that Canadians move approximately every 7 years. They do some digging into where that figure came from and test...

A few months ago I looked at the potential impact of the province’s AirBnB restrictions, especially the removal of grandfathering that previously allowed owners in a couple dozen buildings downtown to legally operate short term...

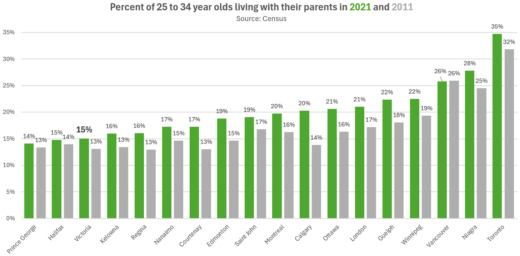

More young adults have been living with their parents in recent decades. In Canada, the number of young adults living with parents doubled in 20 years, and has continued to expand since then. Its not...

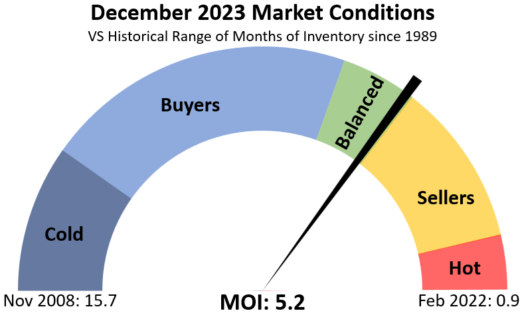

A brief update with the December month-end stats and charts. Generally, not much happens in December, and on the surface of it, the end of 2023 was no exception. Sales were up only 3% from...

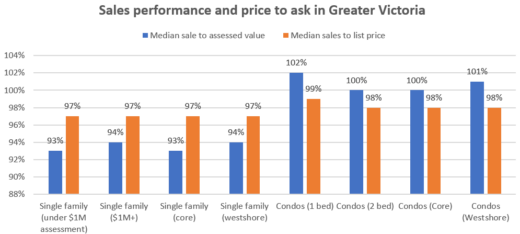

We’re finished another year, and while there were momentous changes on the policy front, the market did very little, ending not too far off from where it started in terms of prices, with about 25%...

It’s no secret that the market is very slow out there. Though relatively modest inventory levels are keeping us in balanced market territory as measured by months of inventory, the sales to new list ratio...

2023 has been a momentous year in housing policy at the provincial level. More has changed this year on the housing front than did in the past 40, and it’s getting quite confusing to keep...

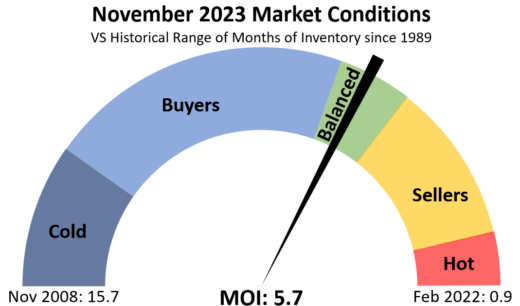

November has wrapped up and conditions in the real estate market are very similar to a year ago. Just like in 2022, high rates have brought prices down a bit from the spring, while market...

As shown in the last article, affordability continues to be extremely poor for any kind of ownership housing. In the past affordability has waxed and waned, but those are cycles measured in 10+ years, and...

Recent Comments