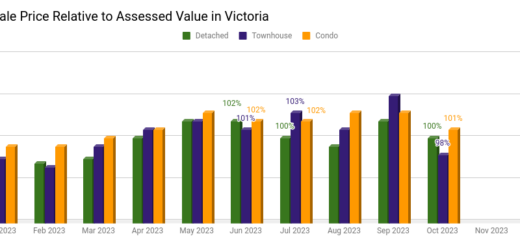

March Market Update

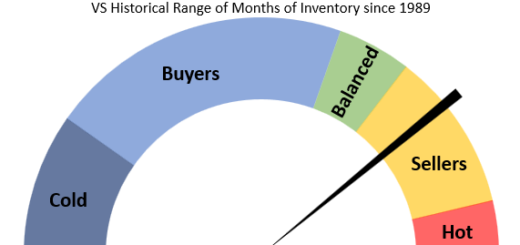

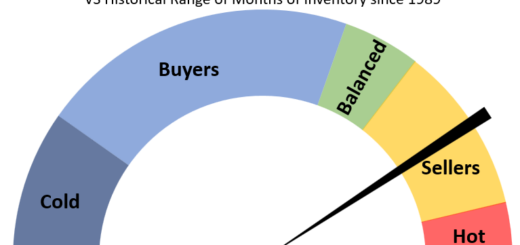

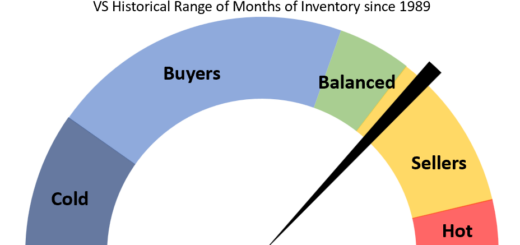

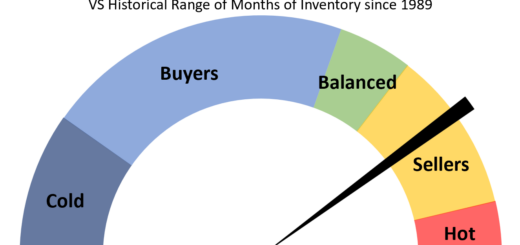

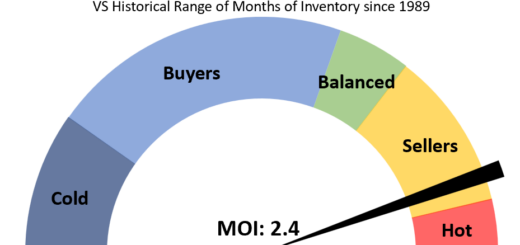

It’s the start of the spring market, and so far it’s a little lacklustre. Sales in March came in exactly where they were a year ago, which is a relative level they’ve been stuck at...

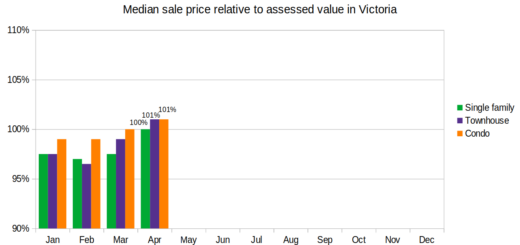

It’s the start of the spring market, and so far it’s a little lacklustre. Sales in March came in exactly where they were a year ago, which is a relative level they’ve been stuck at...

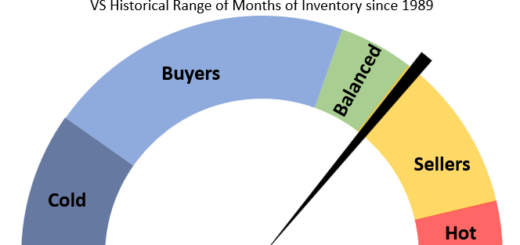

The leap year saved the market from year over year sales declines, with 29 sales reported on the 29th bringing us to 470 total for February, just 10 over the year ago figures. So...

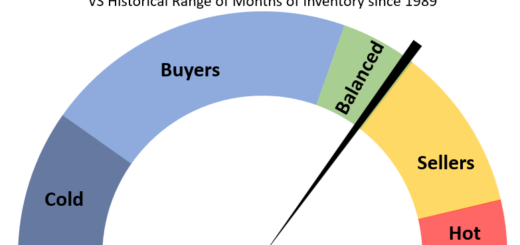

January was in some ways fairly unremarkable, with market conditions coming in essentially identical to this time a year ago. With 6.3 months of inventory (for all property types) we are in a balanced market,...

A brief update with the December month-end stats and charts. Generally, not much happens in December, and on the surface of it, the end of 2023 was no exception. Sales were up only 3% from...

It’s been an eventful month for the housing market both in Victoria and the broader regulatory landscape in the province. In Victoria rates have continued to suppress activity, while the province dropped two bombshells, one...

September is a wrap, and it’s clear that rising rates are putting a damper on the market, at least in terms of activity. Though the headline numbers look ok (reported sales at 493 are up...

August ended with 544 sales, up 14% from last year’s total, and 21% below the 10 year average. Weak sales activity no doubt, though also a remarkable display of resilience given that mortgage rates haven’t...

The Bank of Canada hit resume on their rate hiking path in June, and may well continue with another rate hike this month. At the same time the bond market is up 65 bbps in...

I’ve been banging on about the shortage of new listings for months, but in April things really got critical for the flow of supply on the market. That combined with a gradual return of demand...

March is a wrap, and the situation remained substantially the same as in February. Sales are still historically slow for this time of year, but sellers are uninterested in playing ball with new listings trailing...