The new federal housing plan

Ever since polling numbers collapsed last summer, the federal government has been on a speedrun to reverse the (arguably well justified) perception that they have done a disastrous job on housing. Though I would argue...

Ever since polling numbers collapsed last summer, the federal government has been on a speedrun to reverse the (arguably well justified) perception that they have done a disastrous job on housing. Though I would argue...

A while back Gregor Craigie (local CBC radio host and author) reached out to discuss my take on some of the root causes of the housing crisis. We’d discussed some aspects before on his show...

September is a wrap, and it’s clear that rising rates are putting a damper on the market, at least in terms of activity. Though the headline numbers look ok (reported sales at 493 are up...

I’ve spilled a lot of virtual ink on affordability on this blog and why I believe it matters. In short, there are generally two affordability stories: For condos, affordability has oscillated between bad and good...

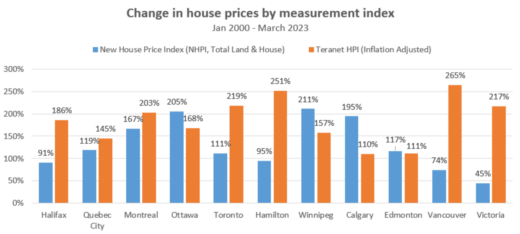

It’s nothing but puzzles on the blog lately, and here’s the latest one: The New House Price Index (NHPI) is an economic indicator developed and maintained by Statistics Canada that measures the changes in the...

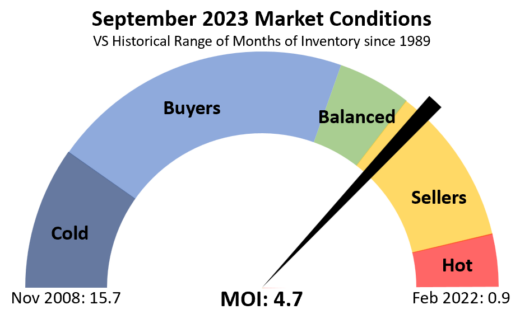

March is a wrap, and the situation remained substantially the same as in February. Sales are still historically slow for this time of year, but sellers are uninterested in playing ball with new listings trailing...

There’s no doubt that we have a severe housing shortage in Canada and BC is especially bad. We can see that in long term rental vacancy rates which are lowest in BC cities (Victoria being...

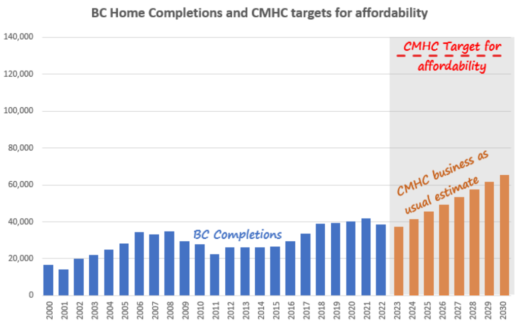

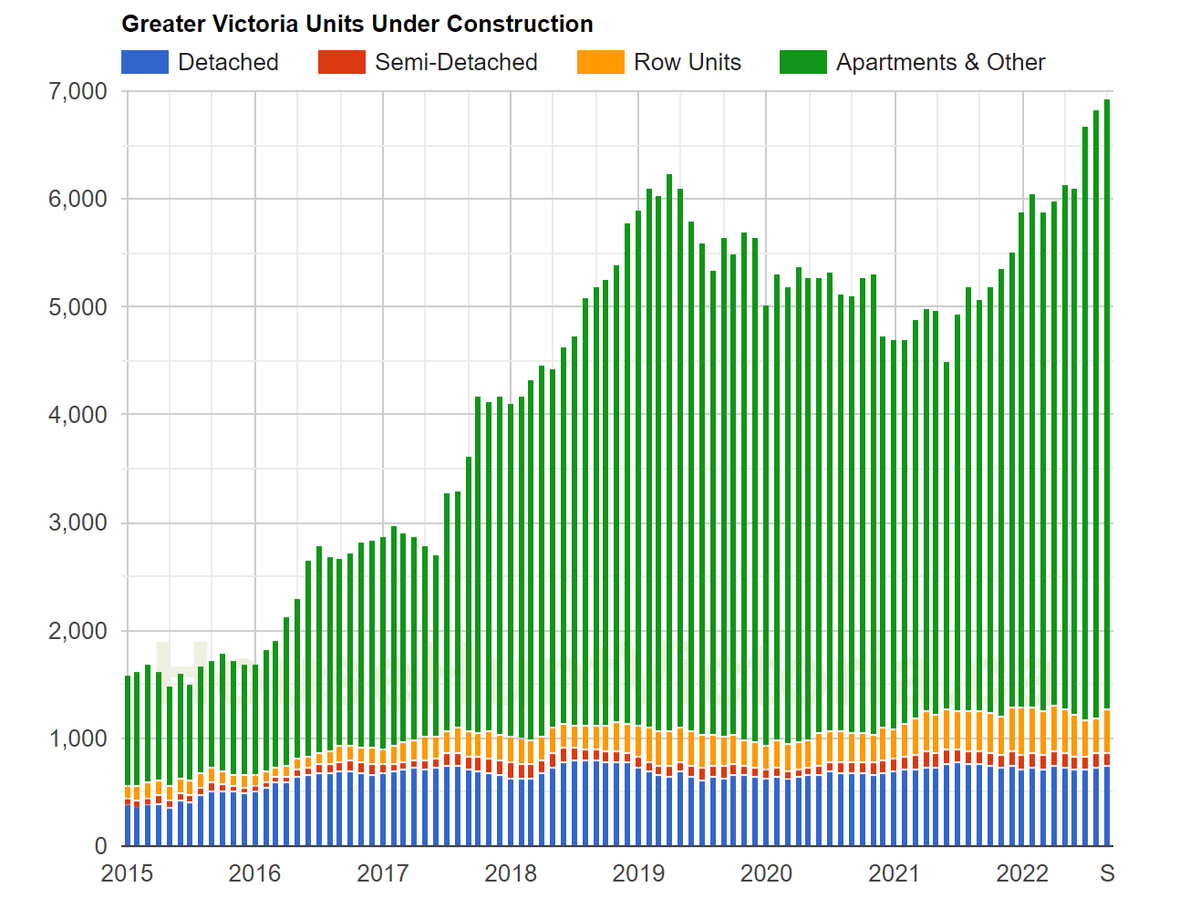

Despite gathering dark clouds for the economy, the number of units under construction has been hitting an all time high in recent months. That’s not just for the past few years, it’s the highest level...

This post is 2 years old. The data and my views may have since evolved.A few weeks ago David Eby released his housing platform which contained a long list of actions both on the supply...

This post is 2 years old. The data and my views may have since evolved.If you hate politics, please skip ahead to below the break for an update on weekly numbers. Early voting is underway...