Fall market arrives early

Victoria saw a strong week for new listings to start off the fall market. There were 35% more new resale listings in metro Victoria last week than the same week a year ago, and that drove active inventory up to 2543, up 18% over this time last year. For all listings month to date (including new inventory and non-residential listings), the increase was a bit more moderate +19%, but it’s a good sign for buyers when inventory has still been below average levels.

| September 2023 |

Sep

2022

|

||||

|---|---|---|---|---|---|

| Wk 1 | Wk 2 | Wk 3 | Wk 4 | ||

| Sales | 141 | 410 | |||

| New Listings | 414 | 1155 | |||

| Active Listings | 2543 | 2300 | |||

| Sales to New Listings | 34% | 35% | |||

| Sales YoY Change | +18% | -46% | |||

| New Lists YoY Change | +19% | +18% | |||

| Inventory YoY Change | +18% | +104% | |||

| Months of Inventory | 5.6 | ||||

With a lot of murmurs of more distressed sales in other municipalities, is this a real increase in new lists or just the normal September surge come a little early? At this point it’s too early to tell. While last week strongly outperformed the year ago (which was already up 18% from September 2021), we do typically get a new listings surge in September. This week’s new listings activity should tell us whether we’ll get a lot more selection this fall or if it will trend downward from here on out.

So far Monday is looking normal, on target for new listings around the mid thirties rather than the 65+ we saw last week.

Zooming way out to the last 30 years of data, we are starting from a pretty unremarkable rate of new listings, slightly under the 30 year average of 1050 a month. Given that we have 50,000 more dwellings than in 1991 one might think we would have more new listings, but that’s not the case.

It’s a similar story with inventory, and despite being up 18% over last year, which was already double the level of Sept 2021, we are still substantially below the long run average.

Back in 2018 when inventory was also low I estimated it would take 2-4 years to build inventory back to average levels. That’s what we were on track for, but pandemic low rates drained away that inventory again to even lower levels. Now rates have put us on an increasing trend again, but it’s worth remembering that inventory moves slowly. So if inventory keeps growing (after stripping out the seasonal variations), and if it grows at the speed it has typically grown in the past, it’s going to be 2025 to 2027 before we get back to even our long run average. Remember that though we have 2543 properties on the market right now, that will dwindle after about October.

On the sales side, the rate of over ask sales is down to 5%, about the same as last year at this time.

September sales should handily outpace last September as well, given that last year we were near the 20 year low for activity. We’ll likely hit between 500 and 550 sales compared to the 10 year September average of 650.

Meanwhile there’s some updated data on the central bank’s Indicators of Financial Vulnerabilities page. Mostly nothing too surprising, but it’s interesting to see that the market remains very well synchronized nationwide (primarily due to rate moves), with conditions across Canada as a whole deteriorating after a bump this spring.

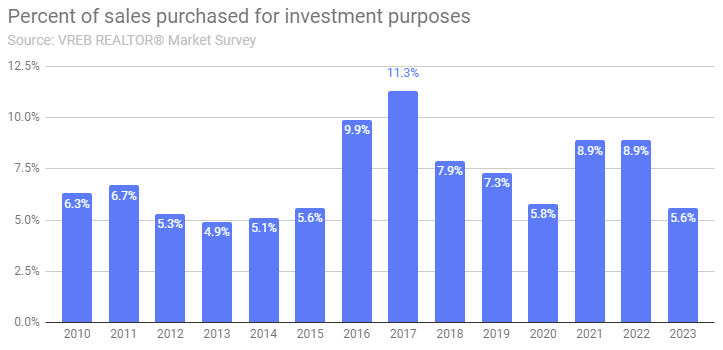

Nationwide investor purchases continued to increase as a proportion of transactions, counter to the decrease we seem to be seeing in Victoria. I’d love to have these data by city or at least province because our survey data is likely quite a bit less reliable, but seemingly it only exists on a national level.

{kind=link}

Interestingly enough, the share of homes being flipped (aka sold twice within 12 months) also increased in the second quarter. Somewhat surprising perhaps, given flipping activity usually increases during speculative markets. It’s possible that some of what are being called “flips” are actually distressed sales instead.

Tough to make sense of this data on a municipal level (why is Toronto so low compared to other cities?) but most have seen a rising trend in these rapid resales.

Tough to make sense of this data on a municipal level (why is Toronto so low compared to other cities?) but most have seen a rising trend in these rapid resales.

This will be worth a closer look for Victoria and beyond just the 12 months available from the Bank of Canada. New lists as a whole but also listings that were bought during the low rate post-pandemic period will be an early indicator if there is any owner distress in Victoria. So far we’re safely within normal ranges, but the increased selection is good news for buyers on the hunt this fall.

New article: https://househuntvictoria.ca/2023/09/18/feds-panic-on-housing-will-it-help/

Leo’s pay…

https://youtu.be/u6i9BsYwspo?feature=shared

Thank you Leo for a vary straight answer.

Well I work part time at UVic so they pay me a salary.

I do some programming contracts for various clients, who pay me for that work.

But no one pays me a salary for any housing advocacy related work, and I have no interest in pursuing one.

Homes For Living is entirely volunteers, none of whom have any development industry connections. You can find the list of core volunteers here: https://www.homesforliving.ca/about-us

Partially why past calls for more housing have failed is because they were all coming from industry folks who obviously have a conflict of interest. It’s working now because calls for more housing are coming from normal people who are struggling to find housing, or understand that other people are struggling. That’s not even remotely my doing of course, there is a long history of YIMBYism in California but it’s really exploded in the last 5 years all around the world. I just happened to wake up to it and help drive it along locally.

Not sad at all. Wouldn’t be hard to monetize the work but I would enjoy it a lot less if it was a job.

I do post data. Such as average income to buy a home across Canada. It seems noteworthy that average incomes can afford average homes in much of Canada. I assume you’re aware of that, but for some reason don’t want to comment on how that can be true if the housing system is broken everywhere in Canada.

Leo works at UVic in an unrelated field. He clearly is an expert in housing and should be getting a salary for it but, sadly, appears to be paid in pithy blog comments.

LeoS, since you are gaining prominence as an expert exactly who is it that you work for and if it is an organization that lobbies exactly where is the funding coming for your employer. I am just wondering if you are what the Americans would call a lobbyist?

I am assuming someone is paying you a salary and if that is not correct it would be useful to know.

I don’t think you’re aware of what’s going on in most of Canada.

Right, but your concise punch line is “how broken our housing system is”.

And does that also apply to Canadian cities where average incomes can buy average homes?

Victoria is the “Malibu” of Canada, expensive Victoria homes doesn’t mean Canada’s housing system is broken.

You may have misunderstood I should keep my answers shorter not add more caveats and tangents

But speaking of affordability, it’s pretty incredible how Edmonton condos are cheaper today than they were 15 years ago, on a nominal basis

That’s despite Edmonton growing at a rate substantially faster than the Canadian average

Thanks Leo. So it went for list. They did a lot of work the past month. Seems extensive for a busy street.

Since you were speaking to a nationwide audience, did you qualify that “rant’ as applying to two provinces (BC and Ontario) ?

Because much of the rest of Canada can afford and quality via stress test to buy homes with close to average incomes (e.g. Alberta, Saskatchewan, Manitoba, Quebec, 4 Maritime Provinces)

https://www.ratehub.ca/blog/home-affordability-improved-in-may-despite-rising-national-average-price/

$1.6M

Marko acreage any decline in prices lately. How is that end holding up. Thanks

4527 Emily cart went quickly. Can I get selling price. Thanks

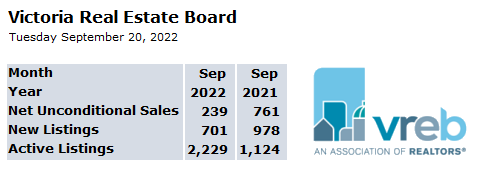

247 sales reported Sept 1-18 2022 vs 239 reported by the board in their weekly update. Could be due to collapsed sales but no way to verify that.

Matches up for me.

Either way we should be hitting 460-480 sales for the month.

Some journalist called me today from Ontario to comment on GST reform based on my Twitter

The conversations usually go like this.

J: So what do you think about this one specific housing policy

Me: 10 minute rant about how broken our housing system is

J: …. Ok

That was for the MLS HPI. Shouldn’t affect sales counts. Then again it’s all a black box so who knows

From memory, I believe that the board was using the wrong sales dates around that time in their analysis. They were using the closing date instead of the pending date.

Just heard Leo on CBC Radio’s All Points West.

Dude is getting famous!

Should, but wasn’t. Can’t recall why they released it on a Tuesday that week. Perhaps they released it Tuesday but the numbers are actually from the day before. Still doesn’t match up, but closer.

Sept 19th, 2022 was a Monday. Shouldn’t it be Sep 1st-18th?

Not a big factor this time. If I manually check number of sales reported, I get an exact match with the report of 260 for month to date, but last year Sept 1-19 I get 255 instead of the 239 reported by the board. Only thing I can think of is that they had a set of collapsed sales from earlier months that were backed out of the numbers last year. It’s a black box with those reported sales numbers, so I find it easier to look at the pending sales.

Thanks James and it was an interesting read.

Here you go Barrister

https://archive.ph/Rhch3

Pre con units closing?

Month to date activity:

Sales: 260 (up 22%)

New lists: 743 (up 18%)

Inventory: 2618 (up 17%)

A bit puzzled at the reported sales numbers being 22% higher than last year, but residential resales (by pending date) are basically at the same level. Not sure where the discrepancy is coming from. In any case, tracking resales more accurately reflects market activity.

Stick to what you know frank, which is pretty much nothing…..

BMO is more concerned with credit card debt. Car loans are secured by the vehicle and losses are limited. Credit card debt has zero collateral.

Given the auto industry strikes recently, these repo vehicles could sell at a premium. Certain vehicles have long waiting lists.

The official statement after the rumor…

From: https://www.ctvnews.ca/business/bmo-to-shutter-retail-auto-finance-business-as-bad-debt-mounts-1.6565467

Wow, I guess folks stop making the payments on those $70k cars before they stop making them on the mortgages.

Vic RE analyst, as to why we sold this fall instead of earlier. We listed after the tenant of 13 years vacated the upstairs … we had to do an update first of course tho :s

Of the 362 pre-owned condominiums in the Victoria core 25 percent are vacant and about 10 percent are subject to tenancy.

Some condominium investors are selling, but not in large numbers. From those that I have spoken with their decision on when to sell hinged on the tenant giving notice to leave. When the tenant gives notice, they are choosing to sell rather than re-rent the condo.

Re-sales of single family housing in the core is a little bit different with 14 percent of the houses available immediately and about 7 percent subject to tenancy.

Strata re-sale properties in the Western communities are about 17 and 7 percent respectively.

In my opinion, it will take a lot more investors deciding to sell before market prices for condos in the core begin to fall significantly

What I’m not to sure of is how this will effect the rental market. If the condo is vacant then it will either be used for home occupancy or possibly a future rental. If it has a tenant then that tenant will have to vacant and likely that would add more pressure on an already tight rental market.

All we need is another 3.5 million investors to sell.

The rental market was so tight this spring for large newer detached house with useable backyards. Westshore has reasonable prices for 3,000 square foot houses less than five years old in beautiful spots. call it BS tho it’s all good

It would be a fascinating read if it did not have a paywall.

Thats what I thought, I am renting my 3 bed upstairs for 3400, its 10 min walk from uvic and that allows me to be picky. Everyone I know renting in the 3700 and up range for a 3 bedroom suite has turnover headache.

Seems obvious

What can you rent for $4,000 a month today in Westshore?

There are more choices for people to rent in the Westshore now than there was a year ago. To obtain $4,000 for the main floor of a house in Langford is at the extreme end for the Westshore.

There is a main floor of a new home on Rowils available for $3,800 and its been listed for six days. Or a 1,794 square feet townhouse on Strandlund for $3,575 a month. and that’s been listed for a month.

Increasing next year’s rent by 3.5% to $4,140 may just cause your tenant to move as there are now less expensive alternatives and the price difference is significant.

You might get 50 calls but I bet that some of them are current renters looking for cheaper housing.

Fascinating read.

“ you must have put more than 20% down. I haven’t seen any with numbers that worked yet, but 4k for a 3bedroom upstairs is pretty aggressive.”

the min 20% but with 4.79% fixed, got lucky as mortgage rates kept moving higher afterwards. Now it’d be impossible to break even with a 20% down, i agree.

and “aggressive” rent but i had like 50 applicants so could have charged more believe it or not. it was an insane process

https://www.cbc.ca/news/canada/british-columbia/a-substantial-revenue-source-but-b-c-s-property-transfer-tax-barely-mentioned-in-campaign-1.4080752

https://www.theglobeandmail.com/business/commentary/article-interest-rates-will-stay-high-cause-the-stone-cold-bond-market-said-so/

Note the columnist said rates are “higher” (than recently), not “high” (which they’re not from a historical perspective).

The provincial budget is available online.

PTT goes back to the former Social Credit government and as far as I know it always went into general revenue. You might be confusing it with the NDP’s spec tax which is earmarked for affordable housing.

Well give us a reference.

https://www.cbc.ca/news/canada/british-columbia/multiplex-housing-vancouver-1.6967977

you must have put more than 20% down. I haven’t seen any with numbers that worked yet, but 4k for a 3bedroom upstairs is pretty aggressive.

I think that may have been a self pep talk

Where do you see doom and gloom? Listings rising?

So much doom and gloom on this site lately.

Quick reversal in sentiment.

Housing market is hard to time, i’ll hold on to my investment property i bought this year; rent is high enough for fully cover my mortgage, property taxes and insurance. West shore home 4k for the 3 bedroom and 1900 for the one bed suite is quite decent imo. The transaction costs are so expensive to sell then re-buy, with a long-term view it should be more than fine. Maybe i’ll regret it but it’s not costing me anything so far. Figure it’s a good way to help out kids in the future with a house if/when the market takes off again out of reach, or at least can help with chunky down payment when they need it in 15/20 years.

Car financing can be a risky game if one thinks we are heading into a recession.

Why didn’t you get out in the spring? So interesting how everyone gets out at the same time.

Apparently car dealerships today started receiving letters from BMO stating that BMO will no longer be providing auto financing.

Victoria has a few of those mega-mansions, that seem to change hands frequently. Presumably serve as playthings for the idle rich.

Distressed sale.

According to Zillow, that King George Terrace property was built and sold in 2002 for $2,275,000 in December 2002

Interesting, TH owners sitting tight. Perhaps because they are the likely end users

First 9 business days of September, Core, Peninsula, Westshore, resales only

https://www.theglobeandmail.com/real-estate/vancouver/article-vancouver-island-mansion-finds-a-buyer-after-14-years-on-the-market/

Regarding porting a mortgage, you usually have within 90-120 days of closing to close on the next home in order to be able to port. Other requirements like the loan amount must be at least equal to or more than the amount ported also exist.

We recently sold an investment property and a key driver was the ability to take the 1.93 rate until 2026 with us. If we don’t find our forever house in the next 90 days we will port the mortgage to our current principle residence and pay the penalty on our 4.94% rate. We can still port the 1.93% mortgage again as long as we buy and sell again within 120 days of each other. Sound complicated?

No longer millennial homeownerx2

That would start a new process, namely the criminal justice system.

Any chance u can break out condos, TH and SFH?

There’s a lot of truth to this (that said, I was in SF recently, and would argue that downtown Victoria is in a lot worse position in terms of homeless folks/drugs/aggressive behaviour and safety than downtown SF, at least the touristy parts – I think we are already there).

It’s a wonder people aren’t more up in arms generally – I don’t think this is “business as usual”; the systems we’ve set up are failing too many people, unless you are lucky enough to have money. Our society seems to be failing on three main fronts at once now – the environment, a basic ability to access reasonable housing, and a basic right to half-decent medical care. It’s amazing to me that politicians aren’t being held more to account than they already have been. Yes of course the environment is an overarching problem, but focusing on that almost to the exclusion of substantive action on housing (only platitudes until recently – I’m talking about the feds now) and the breaking medical system seems totally insufficient to me.

The only thing that seems (depressingly) about the same is politics. We get the Liberals with Trudeau as standard-bearer for years and years until people finally can’t stand his sanctimonious ineffectiveness, and then, voila, the conservative protest vote with a guy like Poilievre who, sorry, seems like he has a mean streak a mile wide. And a middle-of-the-road guy like say Peter MacKay was never gonna fly. And so rinse & repeat. Meanwhile, we can’t even have an honest national conversation about, say, whether the insistence on universal health care should be at least reconsidered when it’s clearly falling apart around us, or whether we should look at medical or housing models adopted in other countries & see if we can learn something.

So what do you do? Batten down the hatches. Help your kids if you have the means. Help others where you can. Stop reading the news, or get involved…

From: https://www.cbc.ca/news/canada/toronto/landlord-tenant-dispute-resolution-delays-1.6963498

Nothing quite like 2 years rent and hydro bill free and then having to start with the eviction process all over again. I wonder how fast the process happens if the landlord moves all the belongings to the curb and changes the locks?

All those missing spring listings are coming on now.

Spent on what?

Where is the accountability?

Why shouldn’t it be use on projects that what it originally collects for, and wasn’t Eby was the one that demanded the PTT to be use for affordable housing not long ago?

Last but not least, what happen to balancing the budget, and eliminate redtape/useless department and positions?

Yes the old “why not use the XXX tax to fund YYY” fallacy. Short answer is it’s already being spent. It’s not sitting in a pot waiting to be put to use.

New expenditures require new taxes, new borrowing, or cutbacks in other expenditures.

So when will Eby use the property transfer tax for affordable housing purposes?

https://en.wikipedia.org/wiki/False_dilemma

Not surprising you don’t under stand this.

New lists looking decent still!

You don’t need to wonder who’s going to build them, the people building them are telling you they will with this change .

https://x.com/khzny/status/1702361080155218249?s=20

Definitely. And it’s going to take at least a decade to fix

“Population movements”, that’s a nice way of putting it.

Great column by Andrew Coyne, unfortunately subscribers only. His main point is that the current crisis is decades in the making and the result of faulty policies at all levels of government:

https://www.theglobeandmail.com/opinion/article-many-of-the-so-called-solutions-to-canadas-housing-mess-are-merely/

Couldn’t agree more, however, Canada can’t house the world. The alternative to capitalism is communism, and we all know how well that works.

@Frank. I am equally curious about the logic behind the view that more rental housing is NOT needed. Is the idea that some people deserve to be homeless? Even the children of the poor who are currently forced to live in vans or without electricity? If there is some right to housing (even very minimally) then do we think that the right is to own a home? To me it seems clear that there is a right to some form of shelter – is such a view really that contentious? And so, if there is no right to OWN housing then certainly there must be a right to otherwise get housing (i.e. via renting it). So maybe REITs don’t work, maybe the last 40 years of capitalism gone wild has caused our housing crisis because there is no solution in the private market.

Also, not sure if people have been following news about San Fransisco. It used to be a tourism hot spot but now many people are too afraid (or whatever) to visit there. There was even a video of some tourists getting their car broken into during broad daylight at a wholefoods that went viral all over Signapore. THAT is where we are headed if we don’t prioritizing getting and keeping 99.9% of people housed. I listened to a podcast with Michelle Obama – she is a brilliant woman. She talked about homeless and said – people have to have a stake in the game. If a large group doesn’t feel that there is any hope for them and that there’s nothing for them – it is bad for everyone.

Who is going to build these apartments? REITS? I can’t see the advantage of building an apartment tower/complex vs a condo tower/complex. Your return on investment is realized shortly after completion and the fact that a certain percentage of units are pre sold prior to and during construction is reassuring. People can wait for a condo, renters need a place today. And who knows what the rental market will be in several years? I don’t see what the motivation would be to build apartments over condos even with the elimination of the GST, especially in this higher interest rate environment. I also can’t see enough units being built to appreciably lower rental rates. If that started to occur, builders would simply stop building.

That was a heck of a hard pivot on housing by the Liberals as soon as their poll numbers dipped.

First deals on the housing accelerator fund, now apparently the standard for approval is for cities to fix exclusionary zoning in some ways. Lots of these deals to come, and they are incentivizing the reforms we need (whether cities manage to not screw up the implementation is doubtful though)

Eliminate GST on purpose built rentals (big move, will revive a lot of rentals that have been shelved by high rates)

Trudeau: “House pricing cannot continue to go up. We’re facing a shortage of housing right now and that’s why prices of homes have become far too high.”

Probably too late to save their political bacon, but pretty clear they are feeling the heat.

Can’t buy a Honda Fit, can’t buy a Toyota Yaris

I’d sell you mine, but I can’t find a car, new or used that I’d even consider trading out for less than $55k. Then there’s the income tax on that money.

I don’t know about you, but I’m not looking to retire at 70. And cars won’t be “appreciating assets” for much longer.

It might be my imagination but there seems to be a lot of inventory in the 2mil to 4mil category and I am not seeing that many sales. But I dont have the stats so it might be a misimpression on my part.

It’s Livable Floor Area as shown in the Strata Plan or renderings provided by those that provide floor plans.

It is also a median. The effect of the few properties with larger than typical limited common property (non livable area) such as patios or decks would be minimized.

According to the board’s statistics the sale to list ratio for a condo was 98.7 percent, in August, when the property is competitively listed for sale. 836/962 is 87% which would indicate that sellers’ price expectations are high.

Is this indoor space only? There is a premium for condos with large patios/outdoor space, especially new condos.

After looking at some more pics in the portal, that is a 700k house in 2019 at most, so still decent froth left after accounting for inflation.

The market for “fixer uppers” such as San Juan has weakened as first time house owners face far less competition from investors desiring a house to clean up and rent.

A problem with homes with non permitted basement suites is that the income from an illegal suite may not always be used by most lenders to bump the buyers income to qualify. There are exceptions but most do not apply to homes being sold vacant.

I would like to see the members of the real estate board indicate in their listings if the suite is or is not on permit. It’s very important information to obtain financing. Just as an agent should be reporting any special assessments on a condo.

“A B.C. realtor who failed to disclose to a buyer that a condo building needed $2 million worth of maintenance has been fined $35,000”

-source Surrey Now-Leader

• The long-expected ‘mild’ economic slowdown may have already begun in Canada as headwinds from higher interest rates build and the global backdrop softens

• GDP per-person has already declined for four consecutive quarters

• The 0.5 percentage point increase in the Canadian unemployment rate over the last four months is the largest outside of the pandemic since the 2008/09 recession

Massive forest fires and labour strikes at 30 ports are among the unexpected events that rocked British Columbia’s economy this year. We believe their impact will leave a negative mark on overall growth, which we have downgraded slightly to 0.5% from the 0.6% noted in our previous forecast. The revision will leave B.C. real GDP growth trailing most other provinces in 2023 (and on par with Quebec). Still, we ascribe the bulk of the slowing from last year not to these unfortunate events, but to a dimmer outlook for household spending and capital investment. Higher interest rates are hitting British Columbians especially hard given their elevated debt levels. This pressure is likely to persist well into 2024—keeping growth on a slow track.

-source RBC Economics

I see the “diamond in the rough” property at 1743 San Juan Ave in Gordon Head just sold for $950K

Lot size 6397, 4bds, 3 baths with suite.

There does seem to be more condos that were completed and sold during the pandemic now being listed again. Of the 418 condominiums listed in the Victoria Core about 11% are condos that were completed and sold during the pandemic.

That percentage of listings increases to 18 percent when you consider non new condos built in the last five years. That’s a big change from the past when there were very few re-lists of newer condos. However sales of pre-owned newer condos is down with only 13 condos with accepted offers or that sold in August. The median ask price is $962 per square foot while the median sold price is $836 per square foot.

That leads me to the opinion that more investors and home occupiers of near new condos are less confident in the future condo market and are choosing to list their homes. And that owners of these newer condos will likely have to lower their expectations to effect a sale.

The increase in listings for near new condos also makes marketing a new condo project more challenging as prospective purchasers have more choices today when looking for a new (er) condo, as builders have to compete against these condos completed in the last five years.

This may be why builders are reluctant to start a new project or are now considering to put a project on hold.

Savings rate is an aggregate of course. There are actually people who are better off from the higher interest rates, as well as those worse off.

But the goalposts have been moved. If the day of reckoning coincides with a recession down the road, there will be consequences.

Oh Frank…. there is a cap on lease payments too.

I have some contacts too and they tell me some of the independent dealers in town are in real trouble, could be going under in the next 3 to 6 months.

Also, this is great: https://www.bnnbloomberg.ca/federal-government-will-remove-gst-on-new-rental-builds-senior-source-says-1.1971481

Trudeau is trying to up his approval rating, but if the outcome is more rental housing, cool

@Sidekick – I’m pretty closely tied to the used car market. There is a glut of “toy” cars coming onto/on the market. Corvettes, Camaros, Mustangs, 370z , convertibles, etc., as well as massive inventory on EVs that I couldn’t source during the pandemic at all – Model 3’s, Chevy Bolt and the like, and prices are dropping quickly as well.

There’s always a slight increase in September of “toys” for sale like RVs and motorbikes, sports cars, but it will be interesting to see if this trend continues into October and there are more price drops. I can tell you that the market is in a weird place and prices are all over the place. One ad will have the same car, year, and mileage for $5-8K less. I think there is a lot of dealers (and private sellers) trying to get that last gasp of crazy high prices, while some are starting to adjust and are actually moving cars.

We will see.

The statement “People are struggling” is always true. It always applies to low-income and to varying degrees to middle and upper incomes in Canada. I assume the implication in the current discussion is that people are struggling “more than usual”. But if you look at long term Canada savings rate, which is 5.0% as of June 2023, it doesn’t appear that in the aggregate that Canadians are struggling more than average. And that’s saving after paying rent/mortgages and buying $70k new cars.

Of course that leaves a lot of low-income people struggling, and I’m not referring to that group here. But if we are talking about middle/upper income HHVers buying Victoria homes and buying $70k cars, they aren’t struggling more than usual. At least not as measured by savings rate.

The point being, the relevant cohort for a househounting forum – homeowner or “house hunting” mid/high income Canadians – don’t appear to be “struggling”, and this helps to explain the robustness of house prices, and almost zero mortgage delinquency rate in Canada. And the nice new cars in driveways.

Not if it’s leased, you’re thinking of a private purchase. And only used for business.

50 hrs for low 100ks, no thanks

Pretty sure there is a $ cap on vehicles price for business use for tax deduction purposes.

Skip must pay well, plus the lease is a 100% tax deduction.

People are odd. I have a workplace acquaintance that earns over a 100k partnered with a spouse that earns the same. They live in the western communities in one of those areas you describe in a recent purchase and went the variable route (not fixed payment). So, they are eating the rate increases as they come. A job opportunity came up that would initially be a 5-10k pay cut, (but with better lifestyle and work) and in 2-3 years would more than out pace their current earnings. The person said no to it because of their current financial strain. At the same time, they went and leased one of those 70k cars. Which they are driving skip the dishes for outside their 40-50 hours a week regularly job to keep afloat.

na

This is a tough one to figure out for sure. On one hand $2-$3k/month seems like an insane amount, on the other hand you drive through areas that I would think would be the highly leveraged (Kettle Creek, Happy Valley, new subdivisions in Sooke) and it isn’t unusual to see 100-140k worth of cars on the driveway. The houses I show on a regular basis in these areas are also packed with shit inside.

I find this impossible to believe but apparently the average price of a new car in BC was nearly 70k -> https://www.theglobeandmail.com/drive/mobility/article-average-price-of-a-new-car-tops-66000-as-drivers-wrestle-with-a-very/

An excellent car, imo, is a Mazda3 Sport @ $24,950. Another excellent car you can’t even buy in Canada due to lack of demand is a Mazda2 which would be around $18,000 if there was demand for it and Mazda sold it. Can’t buy a Honda Fit, can’t buy a Toyota Yaris (in the rest of the world Toyota also has smaller cars in the line-up than the Yaris such as Aygo.)

Seems odd people are struggling but are buying $70k new cars on average.

Hey @dad, thanks for the quick response as my worry set in pretty quick. They are the red ones and no sign of tubes anywhere.

Cheers

If it’s the big red guys those are dampwood termites. Wouldn’t worry about them at all. If it’s the small black guys, those are subterranean termites. They munch on wood that is in contact with the ground, or build mud tubes to access wood above ground. So look for mud tubes on foundation walls.

Both types of termites are very common in Victoria and they send up swarmers in late summer.

Hey HHV’ers, I have seen a number of flying termites around the exterior of my garage and now I’ve found a couple of dead ones inside a fluorescent light in the garage. Any suggestions on how to investigate? Should I call pest control to look into things? Thanks.

Isn’t that the point of higher interest rates?

My preferred indicator is the Boler market. I’ve noticed a lot more Bolers hanging around on marketplace, and some price cuts.

I have been seeing quite a few 10k price drops on RVs listed for sale that were purchased 2020 through 2022 that have been put up for sale in recent months. Also, has anyone looked at the second hand ebike market lately? A lot that were asking $3500 to $4500 have moved to $1500 to $2500 for ebikes with around 500 km on them. Probably don’t have to worry about liens on too many either if they were tossed on HELOCs over the pandemic. Haven’t beeing looking at at boats and motorcycles, but there was likely some pandemic HELOC splurging on those as well.

Define short-term. We’re talking ~30k/yr of income, which is pretty substantial.

Maybe I’m missing something, but if we redirect a large chunk of discretionary spending to mortgage payments, isn’t that going to seriously hurt all the local businesses reliant on discretionary spending? Restaurants, retailers, travel/accommodation etc. Is it not turtles all the way down?

And LOC/credit cards? If we get there then I feel like we’re past the tipping point.

I think early warning signs might be the fire-sale of toys – RVs, boats, motorcycles, etc. If anyone watches those spaces and notices a lot of inventory/price declines, ring the bell.

There are always multiple parties willing to buy a property at some price, for every sale everywhere. But there’s only one high bidder.

What is a distressed property? And where are those buyers currently?

If that were the case, they’d just sell and it wouldn’t end up as a distressed property sale.

I wouldn’t doubt it.

So many people over the years have royally screwed themselves by underestimating the resilience of Victoria real estate.

We’ve tried before and it didn’t work out. Every lender has their own requriements for this, and they aren’t very user friendly. The primary requirement is sale date of current home and purchase date of new home has to be on the exact same day…this is very difficult when moving cities.

I’m an elder millennial and I feel like I just squeaked through the door that was closing in every millennial’s face. I bet Leo, who’s just a hair younger than me, feels similarly.

@samonhunter -can you not port the mortgage over? We ported ours. I’m sure you thought of that – I guess I assumed it was generally available.

Interesting to see the sentiment on here become slowly more bearish. I was surprised that BOC didn’t hike the rate this month. I still think we are in for at least one – if not two – more rate hikes. I also think there’s some pain ahead. It is really sad but as others have said those with more capital will ultimately come out ahead. I guess that’s why the cycle increases the divide over long periods of time.

As a guy who does financial planning, I would disagree. Nearly everyone could afford this in the short term (it would mean living like a peasant, but it’s do-able). How? They cut all other spending, and if needed, put money onto LOC/credit cards. Furthermore, banks are allowing amortizations to grow and not forcing everyone to start sucking up this pain.

In my mind, the real question is how long does this pain last. Is it 12 – 18 months, or is 5% interest here to stay? Governments have been learning a lot about how to manage monetary policy over the last 40 years, so I really think it’s unfair for anyone to say the past is a reasonable predictor of the future. I could give great arguments that interest rates will be back to 2% in a couple of years, and also give great arguments about why 5% is here to stay.

When I look at the people in my circle who have shared their finances with me (something like 100 families), there is only 1 or 2 families who will forced to sell their home, and there is still a chance they will wiggle their way through.

Introvert: while there are always some examples of really poor decision making, I don’t think there will be enough people in the scenario you’ve pointed out here to make a significant dent in pricing. Will some properties be forced onto the market, sure. However, I believe there are just too many people waiting on the sidelines to get into the market (whether that be first time home buyers in the Vic market, or people looking to move to Victoria from elsewhere).

We’ve been watching Victoria for 3 years now (from Kelowna), and once everything lines up, we will be moving. Our mortgage right now is locked in at 1.9% until 2026 and we’re reluctant to give that up.

When these distressed properties hit the market, I believe that there will be 3 – 5+ buyers for each distressed property sale in the Victoria area. If we saw something that was a great bargain, there is a good chance we would advance our move plans to take advantage.

Additionally, recessions tend to hit people in the lower salary ranges a lot harder than those in higher salary ranges. Even if we get to 10% unemployment (which I seriously doubt), that still means 90% of folks looking for work will have it. Point being, most people that are really affected by recessions are renters (though not all). Through my work, I have helped many people financially plan their lives, and housing is the LAST thing to be cut.

That said, I think anyone selling luxury/non-essential items (vacations, jewellery, fancy clothing, etc) is going to have a bumpy few years as lots of folks will start paying 50% of their incomes towards housing.

p.s. I’ll be curious to see if any of the government incentives on housing actually do anything. If OSFI allows 40-50 year amortizations on mortgages prices could start moving up again…if there is a building boom thanks to builder incentives, things could go down…sooooo much uncertainty.

CMHC projects the discounted mortgage rate will be 5.6% in 2030

Most generations have been down this road before , nothing new here and it will sort itself out. Great buying opportunities will be coming for real estate and the stock market

@Introvert – that’s almost my situation. Not quite as bad, I’m up $1950 a month. Ouch.

I knew the rates would go up, and planned and saved accordingly, I didn’t think they would go this high, however. But, life isn’t fair and I’ve learned a lot. It does suck that I’ve been hit by two of the biggest recessions since I basically got out of high school in 2007, and am likely to hit another one this year or next, and didn’t have the money to be in the market on the bull run in the 2010s in either RE or stocks. Millenials have had all the bad luck, lol.

Luckily our new renters are paying $500 more a month. And before anyone says it, I didn’t FOMO into the market. I moved for work in early 2020 and bought in Summer 2020, before prices got crazy and because we needed a house. We bought well under what we were approved for and realized we would need a suite to rent if we were ever to get a SFH and also not be completely house-poor. It is what it is, and we saved for years for the downpayment and saw an opportunity. I couldn’t buy my house right now if I had to again – even with relatively high HHI (160k ish between partner and I), we wouldn’t qualify.

This is why I think we’re headed for trouble. This issue is being masked by the fixed-payment variables, but those will roll over just like those with fixed rate mortgages. I just don’t buy that a decent chunk of the vic/van populace can afford and extra 2-3K/month (of after tax dollars).

Atleast the principal is getting paid down

A family buys a house two years ago, in Langley, with a variable rate. $900K remaining on the mortgage. Monthly payment has increased $2700 and is now $6300.

Fuck me!

https://www.cbc.ca/listen/live-radio/1-63/clip/16007616

It is for airbnb condos in the coming months…. 🙁

Looking at the graph of the SNLR, it’s starting to appear that we might see a double dip.

I think a lot of us have come to assume that we won’t see much more home price depreciation after the first round or tightening.

However, the counter case that I have seen made quite a few times is that the rapid rise in rates has locked people into their mortgages, temporarily creating a new supply crunch that backstopped prices.

There is a possible scenario, where the feds feel forced to restrict immigration due to rising public pressure, interest rates stay high to fight ongoing inflation, and the mild recession we may already be in triggers a further hair cut in prices. I’m still not seeing more than 10% further decline in the tea leaves, and there’s no chance of affordability until interest rates fall in what 2 years (?)… but, the truth is no one can predict the future.

Hold on to your horses folks, this one’s not over.

I wonder if the buildings on the Roundhouse lands are ever going to be built. It seems a perfect location for another six or seven towers. It seems like they are talking about getting a 13 story tower from the deal for supportive housing which at least would move a lot of people off Pandora and maybe empty a couple of the motels. Might be a good trade off for giving approval for six to seven extra thirty story towers. Might block some views but that is okay.

CRA can look into whatever they feel like it as they are there to generate tax revenue (they actually have quotas believe it or not for certain audit groups). The bigger risk is that should the CRA decide to not only go after you for the current year but previous years as well, because the onus will be on you to prove that you haven’t been operating a rental and evading taxes.

No worries for the folks whom have been claiming rental income. Or you can just give your tenants $400 or more to keep quiet provided they don’t turn around and try to blackmail you afterwards.

@VicREanalyst – the $400 amount you mean? Do you think CRA will follow up on specific properties? I doubt it. FWIW I always claim my rental income.

Looks like the renter credit is out for 2023, could spell trouble for those not claiming rental income as you are at the mercy of the CRA.

Wasn’t Martel’s pitch also Victoria RE?

Hawk probably invested in Martel, because he wanted a safe return compared to Victoria real estate, LOL.

Didn’t someone on the forum “invest” with him and was all cocky about the returns?

I found the last graph from the BOC’s Indicators of financial vulnerabilities very interesting. The average of Canadians believe that housing prices will increase 4.3% over the next year, a sharp increase in expectations since 2022 Q4. Interesting how that relates to the current interest rate environment.

Victoria mortgage broker Martel guilty of contempt

https://www.timescolonist.com/local-news/victoria-mortgage-broker-martel-guilty-of-contempt-7534265

The chart of type of homebuyers (first time, repeat, investor) determined by mortgages, does not include cash purchases. I would think that would increase the percentage of repeat and investor share of sales, decreasing the share of first time buyers. I believe cash purchases represent 25% of sales, I could be wrong.