Past performance is not indicative of future results… but we’ll try anyway

Back to our regularly scheduled programming…

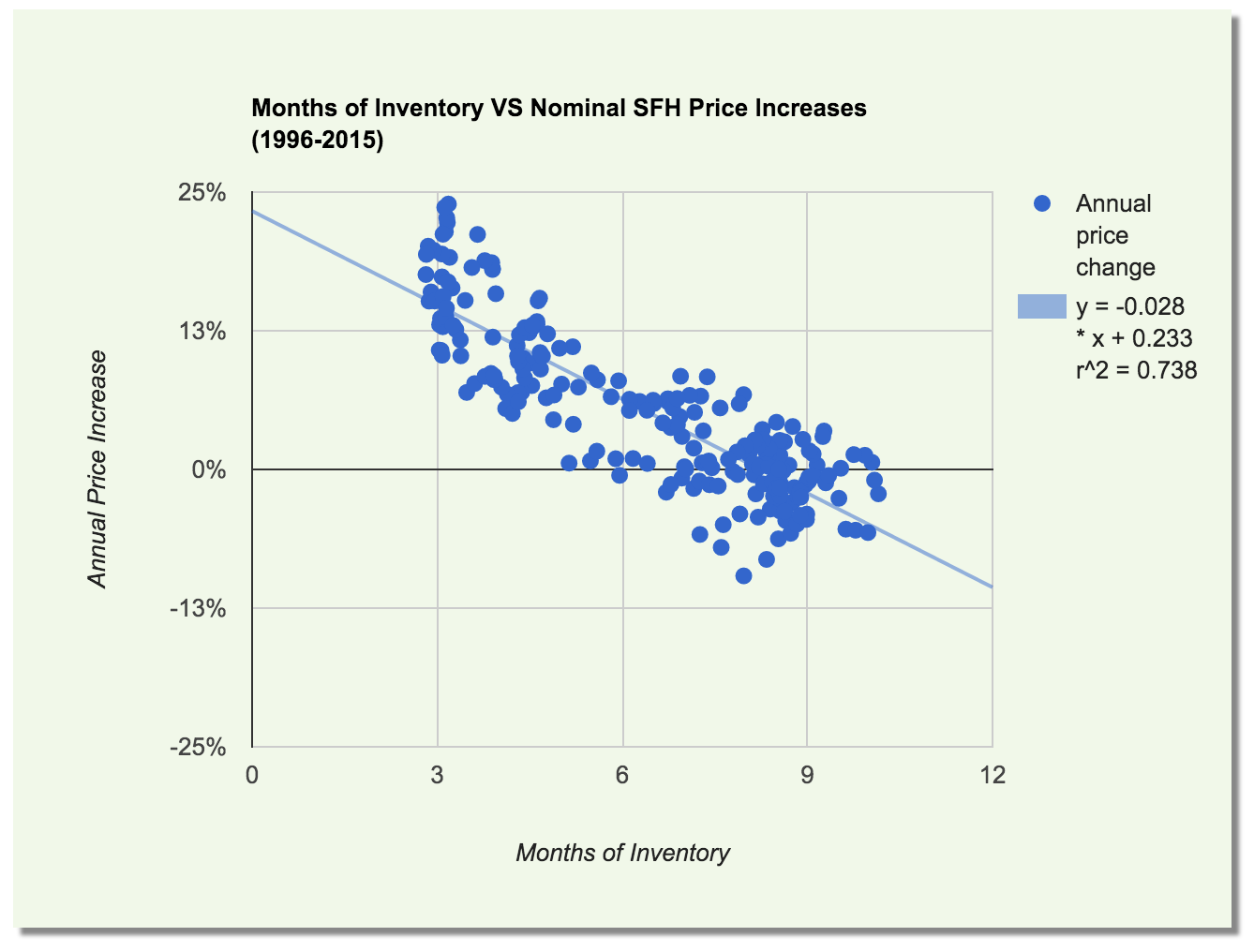

Now that we have data in a scriptable form, we can look at how the market has behaved when various market conditions are in place. Two of the most commonly cited metrics for determination of whether a market is tilted towards sellers or buyers are the sales/list ratio and months of inventory. The theory being that if the ratio of sales to new listings is high, or if the months of inventory is low, then demand is outstripping supply and prices should be rising. For now we’ll use the months of inventory, my theory being that it is a more accurate reflection of current demand than the Sales/List which might be more of a leading indicator (Sales/List could be very high but if there’s enough inventory that doesn’t mean there is a pressure on prices). However this deserves another look in the future.

So how do prices respond relative to months of inventory?

Unsurprisingly, there is some kind of relationship there, with lower months of inventory leading to higher price increases. Note that I’m using the 12 month trailing MOI to remove seasonality, and the price increase in the following quarter extrapolated to a year to calculate rate of annual appreciation. To put this into more of a usable form, we can bin the months of inventory and chart the percentiles (solid blue is 25%-75% percentile, whiskers are max/min).

So a couple takeaways:

- Victoria’s history shows lower months of inventory lead to higher price increases and vice versa.

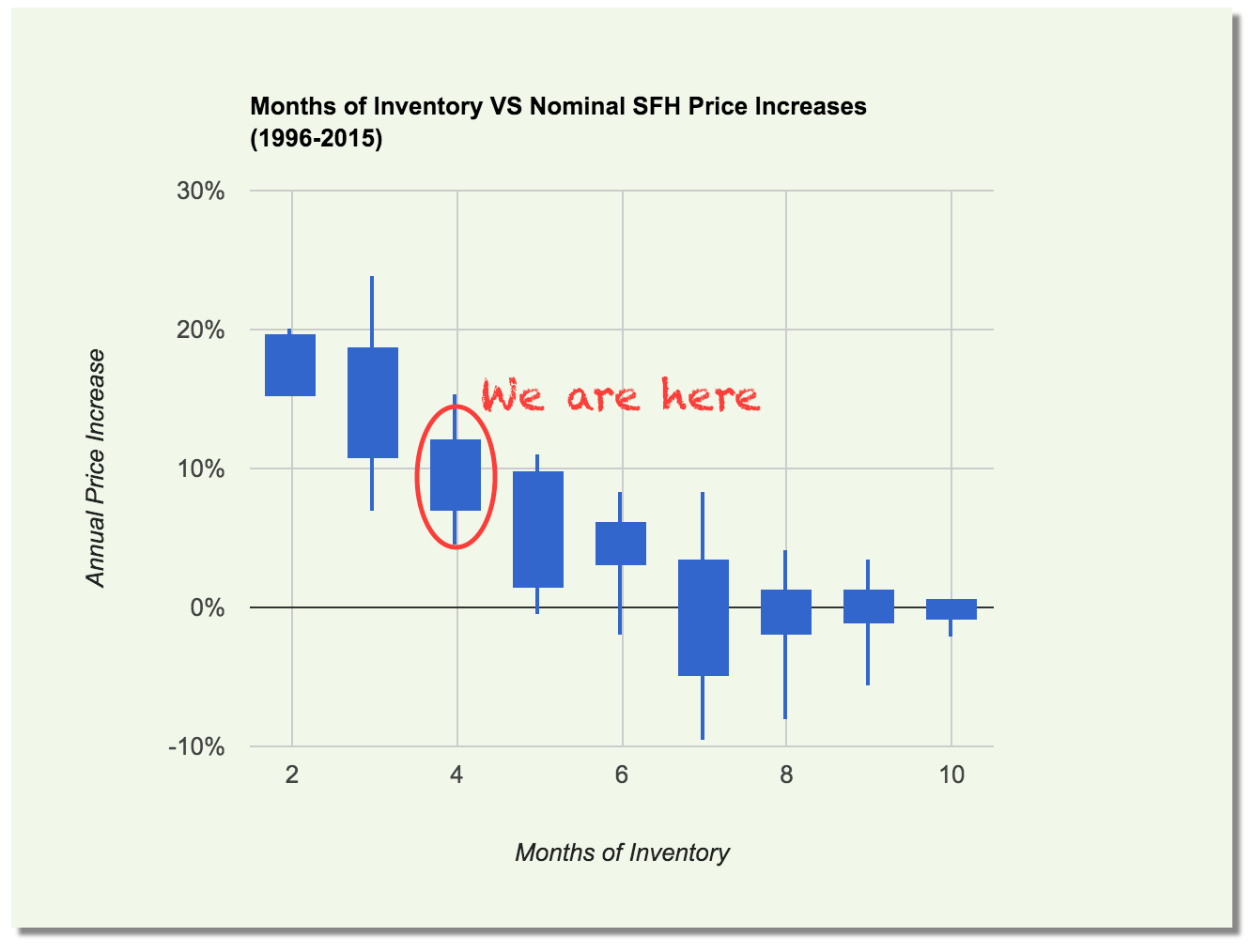

- There is still a lot of variability in price changes for a certain MOI value. For example, our trailing 12 month MOI is currently 4.13. In the 4 bin, we have seen price appreciation at a rate of anywhere from 5% to 15% annually.

- There is a definite “stickiness” about prices at higher months of inventory. It seems the linear relationship breaks down above about 7 MOI.

The price predictions on the stats page are based on a similar binned chart as above. Using the current 12 month trailing MOI, we take the median of all price movements in the past with the same MOI and use that to predict the annual movement in the future. Now of course this is subject to a lot of limitations, the most obvious being that markets are constantly changing, so the chance of market conditions staying the same are about zero. It ain’t perfect, but it’s a start at an evidence based and unbiased projection of prices.

Some areas of future investigation

- Examining the relationship between sales/list and price. With a similar method, how closely would they predict price movements?

- Using another method that doesn’t rely on 12 month trailing averages to remove seasonality. By using trailing averages we are likely being a bit too heavy handed and gathering a lot of noise with the data.

So does anyone have a theory about why prices in Victoria so sticky? Even at hugely high months of inventory that would lead to price declines in other markets, our prices barely drift lower. Do we need higher levels of unemployment to see price drops?

What market this last year or two? Single family homes in the core have only been rising for one year and my understanding is that condos have not risen the same amount. Sales of new condos might be fine but there are no bidding wars or rush to presales as far as I’m aware in general. The micro home development downtown did sell out quickly but am I misunderstanding the state of the condo market?

“The building only received occupancy in September or October I believe.”

A 9 unit building should be able to sell out in pre-build/building stage in this market the last year or two. Don’t think all these high end condos planned are going to sell as easily as these developers think. I see a lot of bagholder builders.

Don’t buy in Sooke, people. Unless you’re retired. Pay more to live in the core: your quality of life will be greater and your house will appreciate more.

Sooke makes sense if you work on the Westshore?

Commuting to downtown seems to be a bit of a pain these days.

The building only received occupancy in September or October I believe.

I’m so relieved Marko. Only took them 2 years to sell out a 9 unit condo. Talk about a hot market. Let me guess, HAM bought two for one deal ? 😉

Why live in Sooke when you can buy in Ladysmith and save half your money and about 10 min commute time… Plus a nicer commute, more to look at.

Where we live we are seeing zero listings. Very odd, it’s like all the people that wanted to sell did and all there is left are young families and baby boomers.

I’ll take a closer look, but if I recall correctly it bins it by 2 <= X < 3 into the 2 bin.

Oh, OK. Thanks.

Don’t buy in Sooke, people. Unless you’re retired. Pay more to live in the core: your quality of life will be greater and your house will appreciate more.

To a large extent, this advice also applies to the West Shore.

Hawk, I know you were worried about the sales pace of the development on Belcher….two units sold today.

Although lots of new homes will be over the $750k limit. I guess it applies to condos though.

And then in Oak Bay, a property that sold a year ago for $1,155,000. Re-sales today, over the asking price at $1,408,000.

This is because everyone and their dog wants to live in Oak Bay/Fairfield. This house is 500k less in Sunnymead, for example.

As for Sooke. Left my office (Fort Street) last week at 3 pm to list a property in Sooke hoping to beat the traffic. Arrived in Sooke at 4:24 pm, 24 minutes late for my appointment.

Developers are laughing….hot market plus they’ve been given a large advantage now over re-sales.

http://www2.gov.bc.ca/gov/content/taxes/property-taxes/property-transfer-tax/understand/exemptions/newly-built-home-exemption

“Do you suffer from market dysfunction? Is your West Shore/Sooke property ‘not performing’ when you need it to?”

According to JJ, what’s happening in Sooke will eventually affect Oak Bay, like a wave. Or what’s happening in Oak Bay will eventually affect Sooke.

It will be like a wave, you guys.

I can’t reproduce it here with W10/Chrome, but I have noticed a few funny things with the comment box at the top (which I had to hack into the theme as it’s not an option normally).

I’ll take a closer look, but if I recall correctly it bins it by 2 <= X < 3 into the 2 bin. So you can see some values in the high twos that would have ended up in the two bin.

It would be more accurate if the bins were 1.5 <= X < 2.5, which would mean there would be no 2 bin at all.

The upper graph shows no times when MOI was much below three, yet the lower graph shows a binful at two. Is there some mistake?

Big nothing in the budget as far as impact on housing. PTT exemption of new construction less than $750,000, and tracking foreign ownership. Will be interesting how public they make that data though. http://www.theglobeandmail.com/news/british-columbia/bc-budget-2016/article28765064/

More or less yes. From a public policy standpoint, why would we aggressively pursue mortgage brokers and not banks? I think that would be unfair and not benefit the consumer. Either we should target both or acknowledge that the whole FIRE industry is ripe with unethical behaviour and commissions are likely not the worst of it.

I don’t have any data on this, but I’d hazard a guess that the average person using a mortgage broker ends up with a better product than the average bank client.

And here is the science behind the 7 year cycle.

https://youtu.be/QrdYBmbaNPs

Your way works too…‘87-94 up, ‘94-01 sideways, ‘01-08 up, ‘08-15 sideways, ’15-22 up.

Whether you use your 7up/7down(sideways) or 10up/4down, the result is still up until ‘22/23.

The reason I follow 10up/4down is it’s much better at pinpointing the optimal buying years right before liftoff… ’71, ‘85, ‘99, ‘13.

I had a client order an appraisal on a foreclosure where she wanted to make an offer. I provided three values for her. The first was a market value report that considered the limitations imposed on a property under a court order to sell. The second was a market valuation of the most probable price the property would sell for under normal marketing conditions and the third value was the highest price she should offer before overpaying for the property. All three were prospective valuations looking forward in time to how the market was changing. Since the court date was in two weeks there was little difference between the prospective and current values which look back over the last 90 days.

This resulted in three values one at $550,000; one at $575,000 and the last at $585,000. All three are market values but under different marketing conditions.

When the bank orders an appraisal the appraisal is a current market valuation under normal marketing conditions according to their banking guidelines. Those guidelines may put a hypothetical restriction on the appraisal. If you have a 12 acre farm with several out buildings. The bank regulation may state that the appraiser is only to value the principle dwelling on 10 acres and disregard the outbuildings. The bank imposes a hypothetical condition on the appraiser. Unless you ordered the appraisal with the same hypothetical conditions, the appraiser would value the property on 12 acres including the outbuildings.

Let’s consider a property that has just sold at $600,000. The second best offer may have been $590,000 and a third offer at $580,000. Which one is at market value?

They all could be at market value when the market value range is between $580,000 to $600,000. You paid the highest and won the property. Would it be fair to appraise the property at the mid point at $590,000 which would mean you would have to increase your down payment by another $10,000? And if you can’t raise $10,000 then your deal collapses. Of course it wouldn’t be fair. The amount you offered is within the market value range. The loans officer has to have one number to loan against. They are not allowed to choose a number in the value range. The appraiser estimates the fair market value of the property at $600,000 which is just confirming that what you paid is within the range of market value and you don’t have to come up with another $10,000.

In answer to your question. The value may be contingent on a host of different things some marketing and some hypothetical. When comparing two appraisals make sure they are addressing the same purpose of the valuation and the intended use of the appraisal.

When you order an appraisal, you’ll be asked the purpose of the appraisal and who will be using the report. The appraiser can then address what type of report you’ll need.

If you can get the lender to waive the appraisal fee that’s fine. But there are no free lunches in the world someone, somewhere is going to pay. That could mean higher banking fees for depositors.

SOLD — 2.48MM (80,000 above ask)

http://www.cbc.ca/news/canada/british-columbia/vancouver-teardown-real-estate-1.3449869

When a major bank says the party is over, it’s time to listen Mike but keep your head in the sand. Most cycles are 7 years, not 10, and we’re just hitting the peak. Last run didn’t start til late 2001/ early 2002. Previous run was 1987 to 1994.

Like every new 10-year cycle, it takes time to ripple out from the core to the Westshore, Sidney & Sooke.

’71 to ’81, ’85 to ’95, and ’99 to late ’09 were no different in that respect than ’13 to ’23 will be.

Just Jack – Based on this comment, the appraisal quality should be the same whether it is bank requested or directly from a client. In my experience, there can be variability in the quality and value depending on who orders the appraisal. Generally, bank appraisals come back more conservative, or, at the sales price in a contract. If a client requests an appraisal directly with the appraiser with/without a purchase contract, does this change the value an appraiser would give for the property?

If a lender farms out the appraisal and many are competing to take it on, then that appraiser may be influenced to provide a value that is more in line with the offered price vs market value before the offer.

With respect to the cost, I don’t think it would be substantially lower to the client as most lenders will waive their appraisal fee to close the business.

If we are trying to compare apples to apples as you noted, then I want to know if the apples are the same.

TD says the party is over. Paying 100K over asking for that dump on Cameo just another sign. Must have paid cash, can’t see a bank lending large on that one.

Toronto, Vancouver at risk of correction, TD warns, after January home sales and prices surge

http://business.financialpost.com/news/economy/home-resales-rebound-in-january-amid-strong-demand-in-toronto-vancouver

This market continues to be a baffling array of sub markets. What is happening in the core today is not what is happening in the outer areas or even other types of properties.

A 3,000 square foot 25 year old home on a 0.4 acre lot with amazing water and mountain views just outside of Sooke Village was bought in August 2006 at $495,000. Since then the floors have been upgraded to hardwood. After 130 days on the market, the property sells today at $440,000. $55,000 less than a decade ago.

Or waterfront property in Sooke that sold in July 2005 at $605,000. Re-sales today at $610,000 after to close to 350 days on the market.

Or a condo in Sidney, bought in September 2006 at $285,500. Re-sales today at $242,500

And then in Oak Bay, a property that sold a year ago for $1,155,000. Re-sales today, over the asking price at $1,408,000.

What we have is a shallow and dysfunctional marketplace with prices increasing in a small geographical area and type of property while property values in the remaining areas are stagnating or declining. There is a growing potential for some very large losses by the banks lending in this one sub market.

This is a transitional marketplace that does not continue for very long. A market that is seen at the beginning and at the end of a real estate cycle.

As one retired bank manager told me. One day a bank manager will look at the high price of a property in disbelief and simply say “I’m not going to approve this mortgage” and then other managers will follow. And that will be the end.

As a broker, these 2 specific marketing points by mortgage brokers and their collective professional organizations personally bother me, and seem purposefully misleading:

1) Our service is free

2) We get the banks competing for your mortgage.

Neither is true –

1) Mortgage brokers get paid well for their work – the compensation model isn’t perfect, but it does allow for some competition, and quality personal service in the marketplace. The DIY online model has it’s advantages – rates are usually cheaper, but the disadvantages are also compelling. Consumers will have minimal options, and the likelihood of being placed in a terrible mortgage product is high – especially on tight purchase timelines. The key here is to choose your broker carefully – it’s ok to ask questions like ‘how do you get paid’ and ‘how many options will I have to choose from?’

2) Brokers DO NOT get the banks competing for your mortgage, and they certainly do not shop your mortgage around. This is complete nonsense. Different lenders have different lending policies – the characteristics of the property and the borrower’s financial situation – are key determinants in where the mortgage goes. The exception to this is when a borrowers credit profile is weak – brokers will shop the mortgage around to different lenders-usually as it is declined repeatedly. Lenders will budge MINIMALLY when it comes to small exceptions from their lending policies, but in terms of negotiating rates – NO WAY, this simply doesn’t happen.

Brokers do have the ability to save clients thousands of dollars through in depth pre-planning, providing feedback on specific properties, and then structuring mortgages strategically. In reality, most people don’t even think about financing until it’s a condition on their signed contract of purchase and sale – usually leaving the potential savings and strategy too late.

Some lenders do not pay brokers commissions or have a list of approved brokers that they only deal with.

Knowing human nature. If a brokerage firm offered a flat fee charge to buyers very few would take advantage of the service. Even though the broker would be able to shop the paper around to more lenders.

People want to feel that they are getting something for nothing. Even when they are not. If any industry can muddy the fact of who is paying for the service, then they can increase their fees with few questions asked.

I even go as far to say that after you visit your doctor or dentist you are provided with a copy of what services the doctor is charging the medical or dental plan. That you can check over to see if you actually received those services.

Because the last time I went to the dentist I was charged for 2 units of Nitrix Oxide. I refused the Nitrix Oxide during the visit. Only when I read over the invoice could I tell the receptionist to take this off the bill.

When we, as consumers, are not provided transparency then we can easily be over billed or under serviced.

Forgot to mention, if anyone’s looking for advice on mortgages, I found this active RedFlagDeals discussion useful: http://forums.redflagdeals.com/official-mortgage-rates-thread-351105/

It’s almost a decade old, but still sees daily new posts.

Technically true but I don’t think it has much real world relevance. if a mortgage broker could get you 3% and their commission was .2%, I don’t think you would have any luck going to a bank and saying lets cut out the middle man and go for 2.85%.

So what you are saying is because banks are unethical mortage brokers should be given some slack? I really think mortgage brokers should be forced to disclose two numbers; the percentage they are receiving from the mortgage amount (approximately 1% give or take) and what that amount works out to in terms of basis points.

”Our service doesn’t cost you anything,” is very misleading just like when buyers

REALTORS® advertise the exact same thing. I guess if you as the buyer ignore the fact that you bring $600,000 to the transaction, for example, which is used to pay the buyers REALTOR® $10,500 (commission may vary) then yes it doesn`t cost a thing, other than your money was used to pay for the commission.Unfortunately 99% of people buy the ”Our service doesn’t cost you anything,” so it is the punch line for a lot of industries.

Yep. Bailed 50 buckets away from our poorly drained back patio before realizing we could science and set up a siphon.

Squint. That’s a joke, right? I can’t tell!

It looks like it went 114K over asking, but maybe there’s something I’m missing. Typo?

By the way, has anyone noticed the “Post Comment” button vanishing when messages get long? I had to break this reply in two. (Chrome, Windows 10)

Or outsourced gatekeepers. Someone has to collect the papers. Can you even get access to a monoline lender without a broker?

With online rate sites, price comparisons are easy to make, so I didn’t feel our middleman was adding any cost on our side of the deal. That will probably change once robo-lenders like the new Quicken service arrive and buyers do end up with a choice between service and price.

Technically true but I don’t think it has much real world relevance. if a mortgage broker could get you 3% and their commission was .2%, I don’t think you would have any luck going to a bank and saying lets cut out the middle man and go for 2.85%.

Similar to how if you buy without a realtor you probably won’t be getting the buyers commission yourself. As much as I like to believe that happened with our house, more likely the selling realtor just pocketed most of it.

54 mm of rain today….good time to be inspecting homes!

842 Cameo – A 1980 five bedroom. Shag carpet and stained white stucco. Assessed at 518K, offered at 500K, sold for 614K. Huh.

The proximity to high-voltage power lines held it back a bit.

I actually think it’s a bit unfair to force brokers to disclose commissions while the banks don’t. How about we force the banks to disclose when they try to sell you a mortgage that they know full well isn’t the best rate you can get? Targeting brokers only isn’t the way to go.

Yea, but brokers are middle people. I think they should be forced to disclose. The CND broker commercials of late have been driving me nuts….”Our service doesn’t cost you anything,” well I guess if a portion of your mortgage payment for the next 5 years going towards the brokers commission is ignored, then yes it doesn’t cost anything.

Just like in real estate, developer (equivalent to bank I guess) doesn’t need to disclose how much he or she is paying the sales associates, but REALTORS® are forced to disclose.

New mortgage rules kick in today. Will be interesting to watch sales in the coming weeks. http://www.cbc.ca/news/canada/toronto/toronto-new-mortgage-rules-1.3448550

I actually think it’s a bit unfair to force brokers to disclose commissions while the banks don’t. How about we force the banks to disclose when they try to sell you a mortgage that they know full well isn’t the best rate you can get? Targeting brokers only isn’t the way to go.

again, I am in the market for insurance( both home and life insurance). the guy with a bright smile and a shiny suit told me, I should consider buying a universal life insurance because it eventually gets my money back, I told him, I am speechless and had to leave…. oh well, beside educating myself how unfortunate the industry is, I just want to say, take care myself seems to be difficult in a mix of good and bad-ass brokers…….

Some brokers will be happy to disclose their fees to you, including myself, – you just have to choose one that is as open and transparent as you desire.

Any and all industries have people with questionable ethics – the key for the informed client is to find a broker who legitimately has their best interest at heart – not just some guy with a shiny suit and a bright smile.

In practise, I try to offer all my clients three different options – educate them on the differences, and then let them choose what they think will work best for them.

Admittedly, I would bet that some people get steered into restrictive mortgage products because of the broker compensation model.

More often than not however, the property, client’s income source, credit score and the closing date of the sale have a far bigger impact on what lender the mortgage is directed towards.

That would be a good thing for brokers to disclose the fee they are being paid by the lender. It would give public insight on how brokers get more commission when they get you to sign up for a longer term or they don’t shop the mortgage to all lenders.

I would go farther and say that brokers should be paid a flat fee by the home owner for their service. And that brokers can not accept referral fees by lenders.

Just last month I was sent a memo that I now have to disclose my appraisal fee in the appraisal report for one lending institution. Appraisers are moving towards a greater level of transparency with the public and the lenders. In this case the bank wants to know what they are being charged by the middle man or management company. The management company charges the bank between $100 to $150 for ordering the appraisal and handling the account receivables.

I charge my client’s for accounts receivable when they order directly from me too. But I only charge $1 for the e-transfer. You pay a $100 less and the lender gets the report sooner.

I was on a speaker phone with a broker and her client and I told them just as a described above. The broker replied that she did not know how to do an e-transfer. In the background I heard her client shout that he knew how to do one and the client sent me my fee over his smart phone, as I spoke with the broker. Report delivered that afternoon and deal closed the next day.

Every appraisal company will charge you a substantially lower fee if you order it directly from them. Because the appraisers don’t have to wait 60 days to be paid by the management company. You just have to insist on this with your lender.

Anyone that wants to buy a home in the core can.

Forgetting about manufactured homes, leaseholds or co-operatives. You can buy a bachelor suite along Hillside Avenue at $118,000.

That’s not the problem. The problem is getting what you want at the price you want to pay. Unfortunately almost all of us are looking for the same thing.

-A house with a suite or potential suite in the core. And that’s because we need the suite to make the property affordable.

So those properties that are outside of the prime rental areas or are not suitable are still “cheap”. Like a 750 square foot home on Lyall in Esquimalt asking $320,000. This home was bought back in 2009 at $300,000. Or a rancher in Tillicum asking $360,000.

But once you add a suite in a high rent hood, then the price goes over $575,000. Since it is more financially challenging to buy the rancher at a lower price than the home with the suite. And that is ironic.

This creates hyperinflation in one class of real estate. There are 246 houses up for sale in the core, but only 97 have one or more suites. And the number of homes with suites that sell each month has been increasing with 62 sold in just the last 30 days. And it even gets worse when you consider that few of us would be buying a million dollar plus home. Most buyers are topping out at $800,000. And there are only 38 homes with a suite under $800,000 in all of the core districts available for sale . And 44 of them sold in just the last 30 days.

If this were a “normal” market then there would be a consistent increase in prices of all types of real estate. This is not a normal market. This is a shallow and dysfunctional market.

Mortgage brokers don’t want to disclose their fees. Interesting, just another sign this industry needs a transparency overhaul.

Regulator says B.C. mortgage brokers should disclose commissions

“The regulator says it’s concerned that brokers might be tempted to steer clients toward lenders who pay the highest commissions and bonuses, rather than into the most suitable mortgage or the one with the lowest interest rate.

“Our concern is firstly that there is a lack of transparency in the way that brokers are compensated and that consumers don’t have any information about the potentially powerful influences on a broker’s advice to them,” the commission’s deputy superintendent Chris Carter said.”

http://www.theglobeandmail.com/report-on-business/economy/housing/the-real-estate-beat/regulator-says-bc-mortgage-brokers-should-disclose-commissions/article28756021/

842 Cameo – A 1980 five bedroom. Shag carpet and stained white stucco. Assessed at 518K, offered at 500K, sold for 614K. Huh.

For some readers the effect of months of inventory on prices might be illustrated as a rain barrel with water coming in at the top and a tap allowing water to spill out at the bottom.

On the water barrel there is a line drawn representing the months of inventory. But we also need to know how many new listings are being added which is the rain water entering into the barrel. And we also need to know how much water or sales are leaving the barrel.

You can have the months of inventory remain unchanged as long as there is enough new listings to offset the number of sales occurring. Stable prices might occur at low months of inventory or at high months of inventory depending on the flow into and out of the marketplace.

The problem is how do you relate the months of inventory, new listings and sales to price? And that depends on how much more the local economy can pay for housing. And that might relate to the size of our economy or the size of the barrel. Are our prices at or near full capacity/affordability or not?

If our market is at or nearing its capacity price appreciation will slow. The barrel/economy just isn’t big enough for our prices to go much higher. You can change the affordability by lowering interest rates or easing up on lending guidelines. That makes the barrel larger as more people can buy at higher prices. You can also make the barrel larger by stimulating the economy by building more housing units and creating high paid construction jobs.

In the short term, I think looking at how the months of inventory, new listings to sales ratio and the days on market is changing will give a reasonably reliable indication of what will happen in the next three months or less. Then you could relate the information on how prices have been changing over the preceding consecutive economic quarters to past historical spring, winter, summer or fall markets that the economy is about to enter into in the next 90 days.

Projecting farther than 90 days means you have to rely on events that may or may not occur. Such as 355 million dollars for social housing or private construction that might be moth balled depending on future economic events.

As is all projections it isn’t an art, it isn’t a science – It’s a goddamn mystery.

Realtor promoted tax evasion. This story keeps getting uglier.

Questionable tactics encourage B.C. homebuyers to avoid taxes

“Several experienced Vancouver-area agents who spoke with The Globe said they believe the risk of tax evasion is high in the sales of new, multimillion-dollar homes, based on how they see other agents promoting the properties firsthand. The Globe was referred to dozens of recent sales, where brand-new and seemingly vacant homes – some staged with furniture – were being shown to clients as “owner-occupied” – therefore tax-free – when in fact no one appears to have lived in them. ”

http://www.theglobeandmail.com/news/investigations/questionable-tactics-encourage-bc-homebuyers-to-avoid-taxes/article28758483/

Mon Feb 15, 2016 8:30am:

Feb Feb

2016 2015

Net Unconditional Sales: 317 542

New Listings: 579 1,108

Active Listings: 2,550 3,480

Please Note

Left Column: stats so far this month

Right Column: stats for the entire month from last year

The BC government is a huge employer on the island providing reliable employment for a lot of people. Perhaps that is a factor with respect to price stickiness?

I’m not sure why prices in Victoria haven’t experienced much depreciation when MOI rises significantly. It is good news for those who want to own here if it is part of a longer term trend.

My recollection looking back over this period is that the lowish interest rates have been around that long and they have only dropped over time. We also know that the core doesn’t have room for many additional SFHs, that densification is occurring, and Victoria is seen as a generally desirable place to raise kids/live. There is obviously demand in the area for SFHs or the new developments out in Langford wouldn’t be going up as fast as they are to accommodate both those who want to live in a new place and those that can’t afford to live in the core.

BTW I was out in Langford visiting a friend who had just bought a new home in one of the new developments. The house was much much nicer than anything you can get in the core for $550000. And there were lots of amenities nearby including the lake, the rec centre, schools and shopping. Not where I’d want to live but I can really see the appeal for families with young children.