Mid Month Madness

Stats update courtesy of the VREB via Marko Juras. Visualizing the current market conditions compared to last year really drives home how drastically the market has changed in a single year. Months of inventory has dropped in half from this time last February, and the Sales/New Listings ratio is up 41%. March and April 2015 is when the market really took off, so one would hope this is the end of these dramatic year over year increases. That said, the spring market is just gearing up, and we have seen hotter markets in Victoria.

Or in text form if you prefer.

| February 2016 |

Feb

2015

|

||||

| Wk 1 | Wk 2 | Wk 3 | Wk 4 | ||

| Unconditional Sales | 165 | 317 |

542

|

||

| New Listings | 307 | 579 |

1108

|

||

| Active Listings | 2472 | 2550 |

3480

|

||

| Sales to New Listings |

54%

|

55% |

49%

|

||

| Sales Projection | 660 | 760* | |||

| Months of Inventory |

6.4 |

||||

*The sales projection is calculated by taking the current sales pace, comparing it to the same date from last year, and adding the percentage increase to the total from February 2015. The number is nuts and if hit, would be the highest ever. Let’s see what happens.

@Marko – don’t forget to mention that 3466 Plymouth Rd just sold previously in May 2015 for $675K. This is truly shocking and depressing, since that is one of the areas I had wanted to buy in. Henderson, Estevan and Gordon Head have gone particularly crazy. I have now decided to look at other areas and maybe one day prices will come back down to earth relative to working family incomes.

I have been hoping for the past few years that interest rates would go up because overall price is more important to me than monthly payments (I wish more people saw it that way), but with talk of negative interest rates (discussed in the Globe and Mail yesterday), that doesn’t seem imminent at all.

CuriousCat: I went to that same open house on at 322 Gorge Road. I had the same general observations as you. The ad says something about it being renovated upstairs. More like fresh paint and that was it. I’d expect at $425k that the wiring was all redone. Pretty obvious that it wasn’t done. They’re putting lipstick on a pig in this case. 🙂 There’s a lot of places like that in Victoria. Overpriced junk.

3466 Plymouth Rd listed at $795k, sold for 868k unconditionally today.

I went to the open house today of 322 Gorge Rd. Lots of people there. The house was listed on Friday, and the agent told me it already had an accepted offer in place, but they would be willing to accept backup offers in case the conditions weren’t removed. Cute house, but it has some issues – only one bedroom upstairs, small, next door to a parking lot, near a busy intersection, knob and tube wiring and I heard the realtor tell another guy there were TWO buried oil tanks, in addition to the oil tank that was still servicing the 1940 boiler in the basement. I’ll be curious to see what the sale price was! (Listed at 425k)

Funny how perceptions are blinded… with that scenario, you are chasing more leveraged debt to upscale…whereas in a declining market, you can upgrade more effectively…(and you likely; a: paid down your mortgage to some degree, b: saved yourself the financing costs of the higher mortgage on targeted property in the interim, c: probably improved your employment status, d: put away some extra savings/investments.

The above strategy doesn’t require you to overextend (which is why bear markets are a blessing to those seeking the opportunity to upscale) – (and FLAT markets amount to the same thing as points a-d also apply)

The average person has very little financial common sense and people just don’t care to think about these types of strategies. Researching the next vacation is probably a little more important to most people.

You have to recognize that very few people as part of the overall population visit websites like HHV, redflagdeals, etc.

Inflation or stagflation (like the 70s) would be great for owners.

Victoria prices climbed 450% between ’71-’81.

Better is to try to time it. Not easy, but if we keep following this ~10/4 pattern…

71-81 up, 81-85 correction

85-95 up, 95-99 correction

99-09 up, late09-13 correction

13-23 up

…then of course sell 2023 and wait to upgrade ~2027 to the 5M house to save the most.

Funny how perceptions are blinded… with that scenario, you are chasing more leveraged debt to upscale…whereas in a declining market, you can upgrade more effectively…(and you likely; a: paid down your mortgage to some degree, b: saved yourself the financing costs of the higher mortgage on targeted property in the interim, c: probably improved your employment status, d: put away some extra savings/investments.

The above strategy doesn’t require you to overextend (which is why bear markets are a blessing to those seeking the opportunity to upscale) – (and FLAT markets amount to the same thing as points a-d also apply)

However… buying a $1,000,000 house and having it drop 20% into a downturn allows you to upscale into a $2,000,000 house dropping 20% 7 years later…and pocketing $200,000 in the process..

The problem is psychology behind it all…..if the market dropped 20% most individuals wouldn’t take the opportunity to upgrade. If the $1 million house went to $2 million at that point for whatever reason people would probably be more comfortable upgrading to $4 million.

” not something people think about” or “not something everyone thinks about” (edit backfired on me there… added an s where I thought I wrote everyone…had it right the first time)…

However… buying a $1,000,000 house and having it drop 20% into a downturn allows you to upscale into a $2,000,000 house dropping 20% 7 years later…and pocketing $200,000 in the process.. not something people thinks about…(the wife says she would rather have our quality of life over lending it to others for an abysmal after-tax rate of return) (ps..not everyone has a mortgage ..oh and this works for those that do and are upwardly mobile)

Db you’re reading the frequency table right.

The differences between now and 2001 were the direction in interest rates, massive economic road and sewer expansion into the Western Communities, and that the median price was rising significantly back then.

As for burying your cash in your home mortgage. It is rarely a bad idea to pay down debt and reduce your exposure to a downturn in prices by selling off any surplus properties you may have.

But remember that the bank isn’t going to foreclose on your property because your home has declined in value. Converting mortgage debt into equity only works well if your equity isn’t falling along with prices. Otherwise your equity may not be changing.

Market Value – Mortgage Amount = Equity

“The report by Economics and Strategy put it this way: “It was not a Merry Christmas for Canadian retailers. December’s volume slump was the worst in seven years.”

CS,

There’s that 7 year thing again. But they blame the weather, loonie, drought, etc. Inflation is rising and hitting pocket books is the bottom line. No wonder gold is popping lately.

One thing all theses gloomy gusses are overlooking is that in a world of Negative Interest rates, bank bail-ins and cashless societies being promulgated…the old adage of burying your cash under your mattress makes more sense by burying it into your principal residence under Canadian tax rules…(thus when higher priced house sales volume increases, it may actually be money seeking alternatives to bank deposits, equities and cash on hand… nada mas…)

I predicted the peak would come after the election. It looks as though we are about there. Last year we had a predictably engineered, pre-election housing boom. Now we’re experiencing the consequences of falling hourly wage rates, declining job quality, rising import prices due to the sharply devalued loonie, leading inevitably to:

Worst Plunge in Retail Sales since 2008. Inflation Whacks Consumers:

http://wolfstreet.com/2016/02/19/stagflation-visits-canada/

Oh, and did I mention the stock market?

Right now RE inventory in Victoria is low. Lots of people holding out for higher prices before downsizing, or migrating to Palm Springs. Meantime, those moving up the ladder intend to buy first and then sell into the rising market.

But once the market falters, as it will, watch out!

And here’s a interesting comparable to that mouldering shack on a 33 foot Vancouver lot that went for more than $2.5 million:

Big Bang Star Puts Bungalow on Market

http://www.pressreader.com/canada/times-colonist/20160220/282411283383662/TextView

View lot, one-third of an acre, pool, modern kitchen glass walls, and located in Los Angeles, a city of 20 million.

But this opinion comes with no warranty!

@ Just Jack your sales comparison is a bit confusing… is it a comparison of sales (both jan+feb) for 2015 vs 2016 in different price ranges? (ergo in the $600 – 700 50 55 => meaning 50 sales in 2015 and 55 in 2016 for Jan/Feb combined?) If so, what this schedule seems to indicate is that 2016 sales in the higher ranges are well ahead of 2015 and like in 2000-2001 higher priced sales tended to lead the bull market …

Or am I reading this wrong ???… (as I can’t understand the 2 lowest number ranges of 1 AND is this for SFH, freehold or all types?)

A hundred showings is pretty crazy depending on the time period.

I guess the question is in such a competitive market whether offers are actually over market or whether this is market value? I’m not sure how you’d distinguish. I would be willing to pay $50k over list if the place suited my needs, the market was rising, inventory was low and I knew multiple offers were likely. That would be, in my opinion, a rational decision if I believed the rising market would continue and I needed to move.

I thought the median in the core was 7% up yoy? The VREB benchmark for the core shows an increase of 10.15% in the core yoy. For example, Oak Bay is up to $857,300 from a $739,700 benchmark last year same time – more than 10%. http://www.vreb.org/pdf/VREBNewsReleaseFull.pdf

That seems like a fairly big change and enough to explain why some houses got bumped into a higher price segment this year. Also, there were just way more sales this than last year – 53.6 per cent more in January alone.

I don’t know Mike, it’s only up 22K from 5 years ago. Speculating that hot Arizona money is flooding into Sidney when sales are at the norm level is just not allowed on this blog. Maybe they’re building a Red Barn and the word’s leaked out. 😉

Have no fear, 60 Minutes is here,wait til they come to BC. Australia crash in the works. Can’t happen here though, we’re only at historical 174% personal debt levels.

“An explosive 60 Minutes investigation, which airs on Channel 9 on Sunday, has discovered banks are irresponsibly loaning large amounts of money to people who just can’t pay it back due to a collapse in the property market.”

“Renowned investment expert Jonathan Tepper, who has predicted mortgage bubble bursts in both Ireland and the United States, told Mr Coulthart Australia would be next.

Mr Tepper believes property values will plummet by 30 to 50 per cent, leaving investors with incredibly high loans to pay back and a lack of return from their investments.”

http://www.news.com.au/finance/business/banking/banks-are-loaning-too-much-to-people-who-cant-pay-it-back/news-story/57af9a6edf85528f5fa38beddd7bb2e3

Here’s the thing about high house prices and low rates though. Affordability might be fine, but in the end you still have to pay off the whole house.

In the past when rates were high and prices were low, it was similar on a monthly basis. A young family would stretch to afford their house, and then live close to the edge for a few years. But then income would increase, and many people started putting a bit extra on the mortgage. On a 200,000 house, that little bit extra soon made a big dent, and many places were paid off quite a bit early. But when the place is $600,000, that bit extra is essentially nothing, and the return on the extra payments is very low. All those misallocated resources will put a drag on our economic growth for decades.

I was completely surprised that sleepy Sidney is up as much as the core at 11.9%… $485,100 from $433,500 (with the majority of the gain in the past 6 months).

Makes me wonder if it’s another signal that retiring boomers are finally making their move… (following the windfall proceeds from their US digs).

In reality the opposite is true VictoriaVv.

The property I was consulted on last week was under listed at $525,000. One of the several suggestions I made was for my client to present a Bully Bid at $575,000.

The marketplace consists only of those that have their homes listed for sale and prospective purchasers actively bidding on properties. That represents generally between 3 to 5 per cent of the total housing inventory. Currently for Saanich East that’s around 100 owners that have their houses up for sale. What is more difficult to determine is how many prospective purchasers there are for a home.

The property on Filmer had a hundred showings that resulted in 6 presented offers. And that is considered to be very strong demand. Similar properties to that of Filmer were exhibiting under 1 month of inventory, with one new listing for every home that sold coming to market and the market exposure around a fortnight. When the market for properties like Filmer is so heavily weighted to the seller there is a possibility for irrational offers over market value.

As more listings come to market and/or housing sales slow, the months of inventory will begin to rise and that will cool appreciation. The important thing to watch is how the median price is changing or if it is changing at all. And that’s what is strange about housing in the core. Despite a very strong sellers market, the median has not changed very much. This most likely has to do with affordability as half of the prospective purchasers are unable to finance at significantly higher prices.

Month Sale Price Median for Houses in the Core Districts

Sep 2015 $640,000

Oct 2015 $677,250

Nov 2015 $620,550

Dec 2015 $672,500

Jan 2016 $656,000

Feb 2016 $672,000

The median price is also being slightly skewed by an increase in high end sales. That shows up when you compare the number of sales occurring in the different price ranges. Again an effect of decreasing affordability in the marketplace.

Sales, Number of for January and February

Sold Price 2015 2016

$0 – 200 1

$200 – 300 1

$300 – 400 26 11

$400 – 500 44 28

$500 – 600 64 54

$600 – 700 50 55

$700 – 800 26 30

$800 – 900 18 28

$900 – 1,000 7 15

$1,000 – 1,250 8 16

$1,250 – 1,500 4 11

$1,500+ 6 11

Decreasing affordability is a leading indicator for a correction in prices.

The hypothesis that affordability of just the mortgage payment isn’t the whole story is perfectly reasonable. If other parts of the household budget are heavier than they used to be, then the same percentage of income going to a mortgage can become an issue where previously it was not. The decrease in savings rates is a clue that this might be happening on a national scale.

Personally I don’t think that even with other costs, the average household in Victoria is nearly has stretched on a monthly basis right now as they have been in the past.

There is a difference between not having stats and proving a hypothesis wrong. A hypothesis exists where there are no stats yet ie. in the case of making a guess about what will happen in the future or the research does not exist currently. Part of the point of this blog really is to hypothesize on the market and gather research to have a more accurate set of facts from which to form a hypothesis.

Your hypothesis is that prices will crash and the market is massively overvalued in Victoria. You won’t know if your hypothesis is true or not until time passes. In the meantime your hypothesis remains a hypothesis.

Your hypothesis also appears to be that the Jubilee-Fairfield/Gonzales area is not experiencing gentrification. That is fine provided you have some reasonable basis for the development of the hypothesis other than that I’m wrong. In the end I don’t really care if you agree or not, I only care about whether the basis of your hypothesis might have validity and that requires more information than you have provided.

What I stated was the stat on what the average family contributes via taxes to health costs. I have no idea whether our family pays more taxes than you or not and I don’t really care. Completely irrelevant to the point.

@VictoriaVv. Keep it civil please.

@Justjack. I feel sorry for whomever you are getting paid real money for advice. They will put low offers in on a couple places if lucky and get massively outbid. You will basically tell them everything is “above fair market price”

Do they know you post here?

Houses in Fairfield not long ago were 180k… Is that fair market?

It’s not a Starbucks it’s a very small grocery store with two major competitors within 5 minutes of each other. Since you can’t show stats that the other Red Barns have increased house prices in those areas then you are speculating as your hypothesis has already been proven wrong.

So your family contributes more than a couple towards MSP so I should be grateful for your support ? I should research medical funding structures now ? LOL You’re getting ridiculous.

Yes, you don’t see any stats because it is a hypothesis. One I am making. As I have stated this is not a fact.

The difference between hypothesizing that Red Barn is a sign or effect of gentrification vs. stating that affordability is decreasing due to an 18% increases in “food” prices is that affordability is currently measurable. CPI exists. You can’t just cherry pick cauliflower as a measure of affordability because the basket of goods has been identified to measure CPI and people don’t purchase just cauliflower or computers. Gentrification is a trend that is measurable after it occurs. Before it occurs it is a hypothesis.

As far as sensationalism goes, I don’t see how a gentrification hypothesis fits this definition but, hey, if you want to call it high drama go for it. Oak Bay probably has a lot more going on than you’d think.

You need to research the medical system and how it is funded if you think your $20/month is covering medical costs for your child. The average Canadian family contributed $11,735 in taxes for public health insurance in 2015.

Good post Just Jack. A lot of people are confused and think that market value is always whatever price something sells at.

An auction is a good example. If everyone only ever paid market value, they wouldn’t have to talk so quickly…

In reply to your post VictoriaVv without resorting to the need to insult or cast disparaging remarks.

What someone pays for a property is known as the Contract/Purchase Price. That price may or may not be at Market Value. If the contract/purchase price lays within the range of what similar properties are currently selling at, then that contract/purchase price is a market price.

Market Value is made up of market prices most often illustrated by at least three comparable sales which never includes the individual property that sold.

For example if the market value range for properties with similar physical characteristics as the subject is $550,000 to $600,000, then a purchase price at $650,000 is not a market price and is not at Market Value.

“Market Value is the most probable price which a property should bring in a competitive and open market as of the specified date under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus.”

Source: The Appraisal Institute of Canada

-You can pay any price for a property that you want to – but that doesn’t mean you paid market value. I can offer $850,000 for a home that is listed at $775,000 because I want that specific home for some reason. I chose to overpay to guarantee getting that property for my own personal reasons. That $75,000 is lost money, I will never recoup that over payment.

Anyone that has been to an auction at Kilshaws or Lunds understands how people can get caught up in the emotion of bidding. The bidding sometimes ends with two buyers fighting it out over a cracked flower pot. And sometimes two buyers can push the price up to level where you could buy that same item new in a store for less. Something that a knowledgeable buyer would not do.

I am currently working with a few clients that are actively trying to buy a home. I provide the analysis to show the market value range of the home that they want to bid on. What is the low, high and most probable price for the property. Sometimes they want a formal appraisal report and other times just a synopsis of the market for a specific property. Since this is a new consulting service that isn’t offered anywhere that I know of – I leave the fee they want to pay me up to them. If it is a foreclosure, I’ll sit and advise them through the court proceeding.

Prospective purchasers are willing to pay market value – they are not willing to be taken advantage of.

I don’t see any stats on Google saying Red Barn just increased house prices in Oak Bay Ave. area. Gentrification is the hypothetical process of tossing out the poor and small businesses for the rich. That takes years to show true or false so is nothing but sensational speculation.

Education is one thing, but I paid for my kids MSP already thanks. If you make average income of 85K you should be able to pay $20 for your own. This isn’t about seniors. Another strawman bait job.

I suppose if an unconditional offer comes in that clause is enforceable but if there’s a condition such as a home inspection well there’s no reason a seller can’t just refuse entry and then the buyer would have to decide if it’s worth continuing. Anyway it’s a pretty dick move to back out of selling unless there’s a really good reason.

@Marko you have such bad news every day for a prospective purchaser with examples of houses going for more than they would have even a few months ago. The truth hurts.

I will say it is extremely frustrating to see a house listed in my price range, put the time and emotion into considering it, then have it going for $100K more than list price. However, I am getting better now at predicting sale prices, and I see several houses in Gordon Head now priced over $800K to not get anyone’s hopes up.

I think the frenzy buyers are thrown into is one reason why we are seeing a sharp price increase in a short period of time. People are panicked and don’t want to miss out, so they overshoot their offer. Yes, the market price is what someone is willing to pay, but there are a lot of psychological factors that go into that decision. The price of produce may have gone up, but at least there aren’t 50 people fighting me for broccoli when I’m at the store, unlike when I go to look at an open house.

I love Victoria.

Do you feel the same way about funding public education?

Most people here aren’t lawyers, so I don’t think hiring one to negotiate a change to a standard listing contract will have a positive ROI. 🙂

That is a difference in opinion, I do think I should contribute to pay for your children and for medical care for the elderly and homeless and that medical care is a basic human right that we should happily pay for with tax dollars. When you are older you’ll probably be just fine but if not happy to have my tax dollars support your long term care.

I think it is fine to have an opinion if you have done the research to support it. It is also fine not to know. And okay be wrong if you have done the research and you missed something or couldn’t predict something. Presenting biased or hyperbolic arguments as fact is more difficult.

FWIW gentrification has been studied pretty extensively and whether Red Barn is a chicken or an egg my opinion is that it is a sign of a changing neighbourhood. Oaklands is evolving as well imo. Starbucks has a similar cause or effect or precondition for the sites it selects/is in. There is a statistical link and homes located near Starbucks appreciate faster than in other areas.

And if I’m wrong I’m wrong about that time will tell. I’ve already identified that this is my opinion and not a fact. Internet opinions are what they are. You decide.

And yes, I’m a really fast typist and reader. My only superpowers unfortunately.

Just noticed totoro banged out 4 healthy posts in 11 minutes. Is that an HHV record ? Now that’s what I call “pent up demand”. 😉

So it’s OK for you totoro to speculate with sensational hyperbole that your property is going to go up because Red Barn moved in down the street ? That’s being a total hypocrite, but whatever suits your case.

Whose cherry picking ? Last time I looked “some” fruit and vegetables are a mainstay of most people’s healthy diets. If you want to get into beef prices they have gone up huge the past year or so. $7 ground beef packs used to $5. Etc etc.

Denying inflation isn’t effecting people’s wallets and eventually eats into housing affordability is bullshit. Comparing computers and Hondas is not remotely the same as the month to month survival costs.

Another strawman bait job like US medical insurance to MSP. I don’t think I should pay for your kids either but it’s only $20 so I should feel better about it. 😉

Yes, that is a problem if the contract states the buyer’s realtor must be paid even if the listing realtor cannot collect. Not sure what it says in that respect.

Mostly this issue seems to be a problem of the realtor’s association drawing up contracts with no representation from consumers

I would personally never go after my client for a commission in such a scenario; however, the problem is the buyer’s REALTOR® could sue my brokerage for the cooperating commission.

Yes, I can understand how it would be frustrating for a realtor who has put the time in to have a seller back out but I would negotiate to remove this clause:

(iii) an offer to purchase is obtained from a prospective buyer during the term of this Contract who is ready, willing and able to pay the Listing Price and agrees to the other terms of this Contract, even if the Seller refuses to sign the offer to purchase;

Found a case in TO on it, the contracts stated, “due and payable upon delivery of any “valid offer” on the terms set out in the listing agreement, or any other terms acceptable to the seller.” This is payable if the non-completion of the transaction was owing to the seller’s “default or neglect.”

http://www.thestar.com/life/homes/2014/01/09/court_finds_agent_must_be_paid_for_doing_the_job.html

I personally would not sign a real estate commission contract that states this. I don’t want to be put into a situation where I have to accept a full price offer if something unforeseen happens and selling is not a good option any more ie. cancer diagnosis, job loss or other change of circumstances.

I didn’t think of the realtor contract. It states commission is due when a full price offer comes in? Does it have to be unconditional?

LISTING BROKERAGE’S REMUNERATION: The Seller agrees:

A. To pay to the Listing Brokerage a gross commission of ________________________________________________________

of the sale price of the Property, plus applicable Goods and Services Tax and any other applicable tax in respect of the commission

(commission + tax = remuneration) if:

(i) a legally enforceable contract of sale between the Seller and a Buyer is entered into during the term of this Contract; or

(ii) a legally enforceable contract of sale between the Seller and a Buyer who is introduced to the Property or to the Seller, by

the Listing Brokerage, the Designated Agent (as hereinafter defined) a Cooperating Brokerage or any other person

including the Seller during the term of this Contract is entered into:

(a) within sixty (60) days after the expiration of the term of this Contract; or

(b) any time after the period described in (a) where the efforts of the Listing Brokerage, the Designated Agent (as hereinafter

defined) or the Cooperating Brokerage were an effective cause;

provided, however, that no such commission is payable if the Property is listed with another licensed brokerage after the

expiration of the term of this Contract and sold during the term of that listing contract; or

(iii) an offer to purchase is obtained from a prospective buyer during the term of this Contract who is ready, willing and able to

pay the Listing Price and agrees to the other terms of this Contract, even if the Seller refuses to sign the offer to purchase;

B. The remuneration due to the Listing Brokerage shall be payable on the earlier of the date the sale is completed, or the completion

date, or where no contract of sale has been entered into seven (7) days after written demand by the Listing Brokerage; and

C. That to assist in obtaining a buyer for the Property, the Listing Brokerage will offer to Cooperating Brokerages a portion of the

Listing Brokerage’s commission in the amount of

of the sale price of the Property, plus applicable Goods and Services Tax and other applicable tax in respect of that portion of

the commission.

D. The Listing Brokerage and Designated Agent will advise the Seller of any remuneration, other than that described in Clause 5A,

to be received by the Listing Brokerage in respect of the Property

I could quote the dramatic decline in prices in computers to support how things are more affordable even when they may not be

Or cars….a new Civic/Corolla these days is a bargain compared to 20-25 years ago especially when you adjust for the fact that most base models now have power windows, mirrors, back-up cameras, etc.

I didn’t think of the realtor contract. It states commission is due when a full price offer comes in? Does it have to be unconditional? Sometimes deals still fall through and the seller doesn’t sue for specific performance. Do they still have to pay the realtor?

If you are going to claim cost of living has increased eroding affordability you need stats on cpi. Quoting food as being up by 18 percent when you really mean some vegetables is misleading. You also need overall wage increases to determine this. Cherry picking stats may suit someone’s feeling that they are being victimized by the system but it doesn’t promote accuracy. I could quote the dramatic decline in prices in computers to support how things are more affordable even when they may not be. And the stats may show that over time the cpi has risen faster than wages – or not – but the topic was mortgage affordability compared over time with the stats are clear on that.

As for feeling it is personal, it isn’t. It is just about checking out your assumptions before posting. Google makes that a pretty easy thing to do. When you post information as if you are the harbinger of truth and the info is inaccurate or misleading or based on a theory you have not researched it doesn’t do anything to advance a clear picture or support credibility.

Where it becomes unethical is if the seller has no intention to sell at the list price. Say he lists the place at $525,000 hoping to incite a bidding war, but only gets one unconditional bid at $525,000. Can the seller still refuse to sell for full ask?

I’ve been having long discussions about this on listings I’ve taken in the last 6 months…..the REALTOR®(s) could sue the seller for the commission as all the requirements of the listing contract have been fulfilled. That wouldn’t be fun for the seller.

I always make sure my client is 100% okay with accepting a full price offer at asking price. If not, we raise the price until such threshold is met.

Yes you can refuse a full price offer. Sellers sometimes change their minds. I’m not even sure if it is a question of ethics because in re you don’t have a deal until the seller accepts in writing.

I wonder how prospective purchasers feel about being baited with intentionally under listed properties in order to illicit multiple bids?

For the most part I don’t think it is intentional. For example, in September my client purchased a property on Granada (Mount Doug) for $561,000. The house next door (literally next door) almost identical when the various small variables cancel each other goes up for $600,000 (sellers increased their expectations) and it sells for $628,000.

I wouldn’t blame the owner or REALTOR® for intentionally under listing…the market is just nuts. They took the closest comparable, jacked up the price $40,000 and it still went over asking.

I don’t think so. It’s just a different market. An auction not a fixed price market.

Where it becomes unethical is if the seller has no intention to sell at the list price. Say he lists the place at $525,000 hoping to incite a bidding war, but only gets one unconditional bid at $525,000. Can the seller still refuse to sell for full ask?

@JustJack. I don’t get how you don’t understand that “fair market value” is what people are willing to pay for something!!!

It’s called free market! Seriously, you are an appraiser and don’t “get” that its not some outside force “forcing” prices “above” the unspoken market value… Who determines house price??? BUYERS!

Prices are never “low” or “high” they are priced at what the market wants them to be at!!! It’s insane you “value” houses (obviously undervaluing them from your bias).

Too funny Jack !

Hawk, FYI on how to deal with negative comments.

https://youtu.be/5WeSKgW8pQ0

I wonder how prospective purchasers feel about being baited with intentionally under listed properties in order to illicit multiple bids?

How would you feel if you went to buy a TV and at the register they increased the price? Obviously that is against the law for merchandise. If the merchandise is advertised at a price that constitutes an offer that the consumer can accept or not. It is against the law to bait and switch on merchandise.

But not with BC’s real estate law. The asking price is not an offer by the seller. If it were then you could accept with a non subject offer and the house would be yours.

What happens is you have an agent list a home at $525,000 when a competitive asking price should be near $600,000. The agent hopes to attract multiple bids over $600,000 when the fair market value is $575,000.

Even if the property sells at fair market value, the public is left with the perception that the market is hot as properties are selling above asking price.

This is not considered to be illegal within BC’s real estate law. But maybe it should be?

I was accurate. A 5.5% ICBC increase is what it is, not the amount. If everything goes up 5% it adds up is the bottom line. Go tell CBC they are wrong on what they reported, those are facts. Blame the loonie or whatever you want to make excuses for, but it’s reality. Inflation is kicking in bigtime.

I don’t feel slighted I just prefer accuracy to sensational hyperbole or speculation with no research. Makes for more reliable conclusions.

I’m not sure about the different icon. I travel a lot and use different devices so might be related?

“You posted previously that you are saving thousands and not feeling pinched as a renter and now you are complaining about affordability based on amounts that combined are probably less than $20 a month? Difficult to reconcile.”

I was talking general terms for all. Stats Can does some shady stuff with the numbers as per brand swapping etc.

“Higher fruit and vegetable prices were also a factor, up 18 per cent annually in January after rising 13 per cent in December. A subsector that includes broccoli, cauliflower, celery and peppers increased by more than 22 per cent, its highest since 2009.”

http://www.cbc.ca/news/business/inflation-january-1.3454993

Must you always feel slighted when I post something ? I see where Jack is coming from. Everything is always an exaggeration when it doesn’t suit your story line, but I’m sure you will have something else to contradict with a thesis.

“totoro I wonder why you always get a different auto-generated icon by your name, while others that haven’t set one get the same one each time. Might be related to why you are often getting stuck in the spam filter.”

Maybe she’s a robo-poster. 😉

Variable has beat fixed 80% of the time in the last few decades. Of course that is in a period of declining rates. It will also beat fixed in a flat rates period. When it becomes a bad idea is if rates go up.

Once our 5 year is up we are going for variable as well. 5 year was a mistake, although not a wildly expensive one given how low rates were for both.

If rates ever do rise significantly there will be a huge hit on affordability, including for those with variable rates and big mortgages.

Actually everyone will get slaughtered other than those very few with a 10-year mortgage.

If rates go up at that point and time 50% of 5 year fixed mortgage holders will have less than 2.5 years left on their mortgage so in my opinion the 5 year fixed is really the 2.5 yr. fixed as one cannot predict when and if rates will go up.

Than again, I am bias, I’ve had nothing but variable mortgages. Renewing a 5-year variable later this year and it is 0.3% lower than it was 5 years ago 🙂

If you commit to going variable your entire life and there is no risk of bankruptcy/affordability problems if rates went up I think you can’t go wrong. Problem is most people aren’t discplined enough to get to the point where there is no affordability concern; therefore, the love affair and false security of the 5 year fixed.

@totoro I wonder why you always get a different auto-generated icon by your name, while others that haven’t set one get the same one each time. Might be related to why you are often getting stuck in the spam filter.

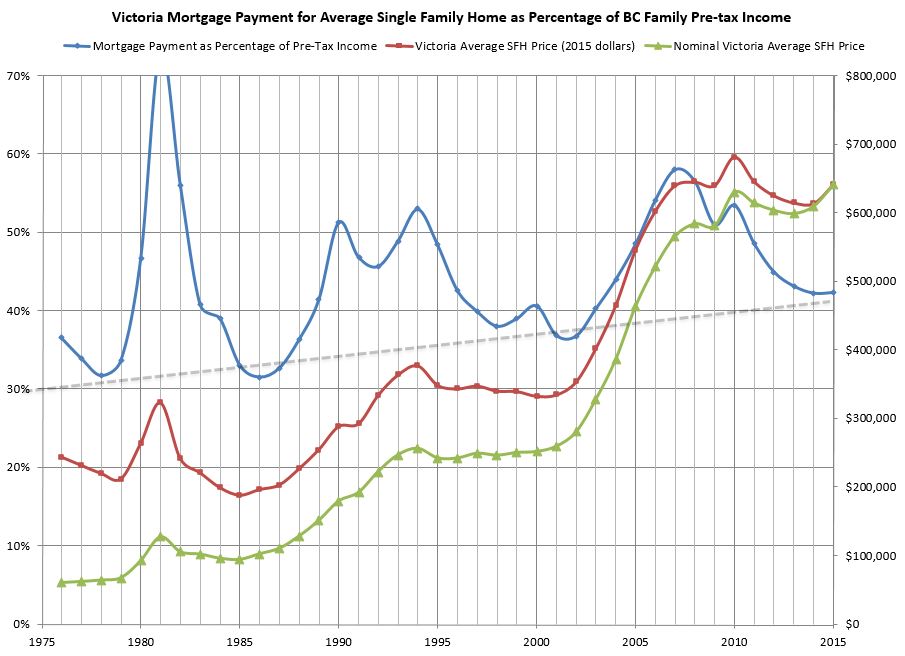

Yes, the key on those graphs is the change over time. The exact percentages are probably meaningless, because the average BC income does not represent the average Victoria buyer. However I think it is reasonable to assume that provincial income trends will be reflected locally. I have used Victoria income stats in the past, but those are based on very small samples so the data quality isn’t great.

The unfortunate reality is the average consumer only cares about the monthly amount. That’s why almost no one has an issue getting a 72month car loan because it seems like a small monthly number.

I think the indebtedness of the nation will prevent them from increasing rates all that much. When rates increase a bit the economy will take a nosedive and they will have to dial back. I can’t say I understand enough about the international factors that might drive bond yields up though.

What gouges? Look to the US before you complain about MSP. ICBC is a gouge? Are you referring to their rate increase request that will result in the average driver paying $3.70 more per month for insurance? This rate is based on a budget that takes into account personal injury settlement costs. Seems reasonable and rational to me: http://www.news1130.com/2015/10/15/icbc-reduces-insurance-rate-increase-request/

Food prices increased 18%? Exaggeration. Vegetables went up due to the California drought and the loonie, but overall food is not up 18%, but 4%. Here are the actual stats: http://www.statcan.gc.ca/tables-tableaux/sum-som/l01/cst01/cpis08a-eng.htm

You posted previously that you are saving thousands and not feeling pinched as a renter and now you are complaining about affordability based on amounts that combined are probably less than $20 a month? Difficult to reconcile.

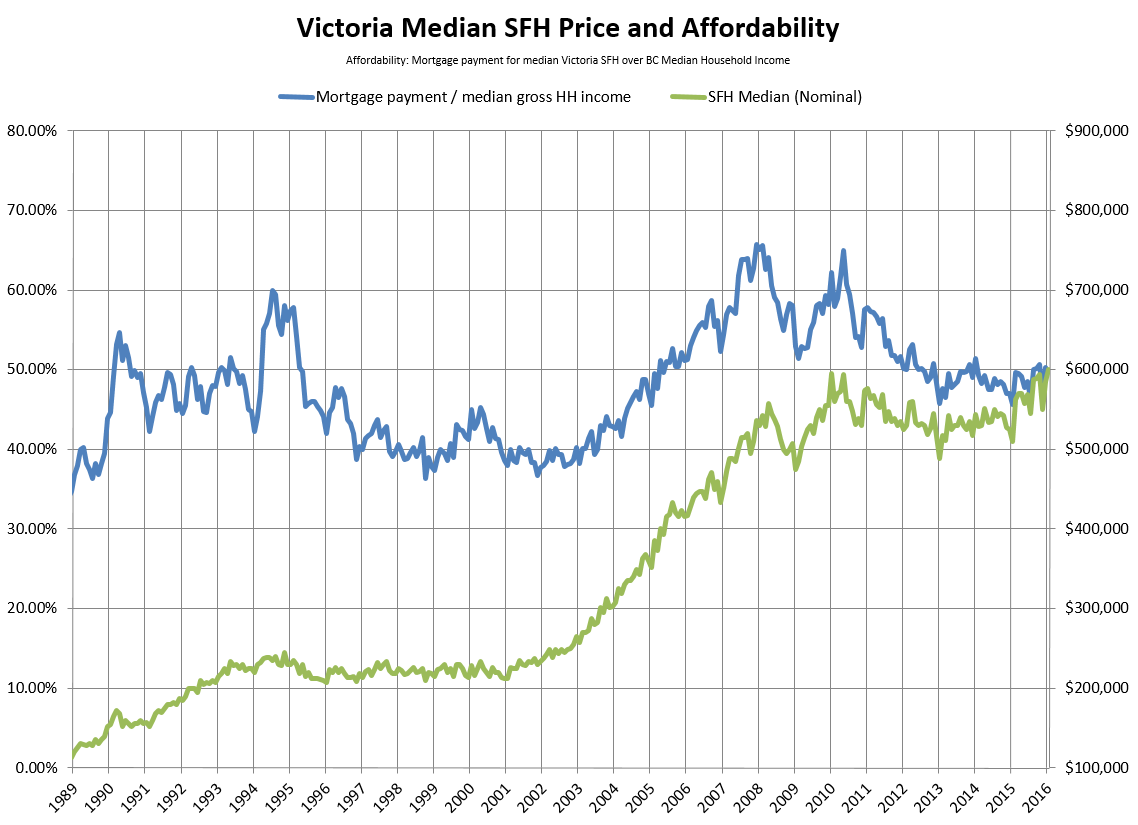

These graphs really put prices into perspective. It is easier now to afford a mortgage in a rising market like this than it has been at many points in the past when prices were much lower.

Unless you are sitting on a big pile of cash mortgage rates are the most critical factor in determining affordability. Unfortunately, they also carry the risk of an increase. We took a ten year fixed rate when we bought our home as a way of dealing with the potential risk. The rate is low, but not as low as now. The stats show that a variable rate has worked out better for the vast majority of people.

If rates ever do rise significantly there will be a huge hit on affordability, including for those with variable rates and big mortgages. Will the government take steps to stop this from happening? I don’t understand how that would work but it is an interesting question.

Toss in 18% food inflation plus all the other gouges like MSP, ICBC etc and affordability is much worse IMO. Not to mention those who seem to be paying $50K to 100K over asking on a regular basis.

‘White-hot’ Vancouver, Toronto housing markets could be dragged down by rest of Canada, report says

“A new report from Moody’s Analytics says Canada’s two priciest markets could eventually be dragged down by housing results in the rest of the country.”

http://business.financialpost.com/personal-finance/mortgages-real-estate/white-hot-vancouver-toronto-housing-markets-could-be-dragged-down-by-rest-of-canada-report-says

Affordability still looks pretty good. I had the annual graph updated for end of year 2015 (blue line).

As you can see back in 2007 the mortgage payment on the median SFH took 58% of the average BC family income. In 2010, although prices were higher, that was down to 53% due to dropping rates, 2015 that was down to 43%. Despite the upswing in prices rates were still dropping every year.

Note however that there is no income data for the last couple years so that is an estimate based on earnings growth. Not necessarily totally accurate past 2012 but should be close.

Or see monthly here (using all family income rather than economic family, hence the different percentages, but same pattern):

Video: U.S. investors get close-up look at Victoria’s tech sector:

https://t.co/mvBagngCkj

Hawk – In 2005 VHB (Vancouver Housing Blog) was an active blog forecasting real estate doom. It was obvious then the US market had detached from reality and the Canadian market was exhibiting the same signs. Most on that blog thought Canada would follow the same trajectory but then Harper extended amortizations and increased the CMHC ceiling. And then ever lower rates until they got to near 0. Who knows what’s next…

Sellers are making a killing off the suckers. They don’t make houses anymore ya know, lol.

Mike, those condos weren’t poor, maybe in need of an update but completely liveable. 5K over is nothing to get excited about. Rockland is a nice block but a lot of homeless probs in that hood. Southgate must have been waiting forever being over 55.

What history does show for the housing market is that prices do rise long term faster than the pace of inflation.

Makes sense for the core areas for sure. Population increases every year; yet the most desirable areas like Oak Bay stay fixed in terms of inventory.

Hey Leo, what do the affordability calculations look like right now if we go 2007 peak vs 2010 peak vs now?

The US market didn’t peak til 2006 and didn’t begin decline til 2007 Chris. If you really need to know I was awaiting permanent work status in 2005 which dragged on til 2006 but prices crept out of my affordability range. Bad timing for me. 5 year rates were still 6% to 7% then so not that cheap. Stock markets were making money with gold ,oil, and commodoties heading up. Completely different markets then.

As the previous article shows, credit levels from 40 years previous 2005 crammed into the last 10 years is extremely telling where this market is headed.

Now that the market is taking off like a rocket to the moon the bears will become more and more crazed as their dreams of a crash vanish faster than a McDonalds hamburger in front of a fat kid’s face.

Looks like core condos could be getting jumpy…

Inventory pinch even in condos right now.

The bidding wars continue to roll in this afternoon…ask/sold

816 Falkland Rd – $949,000/$975,000

1071 Willow St – $539,900/$581,000

860 Victoria Ave – $695,000/$763,300

1330 Haultain St – $749,999/$801,000

4079 Dawnview – $798,000/$820,000

Hawk, of course you were bullish back then… Rates were lower than they had ever been, debt levels were high, building was rampant, big price rises were happening consistently and the US was just starting to go over the edge. Glad you could see through all that.

.

Looks like core condos could be getting jumpy…

I noticed 2 older & in poor condition units went over list price today.

311-1149 Rockland, 1976, 1177 ft, sold 380k

410-1063 Southgate, 1992, 1178ft, age 55+, sold 336.5k

Someone was also mentioning those new Belcher units (awful street) finally sold out full price 540k.

Easy credit is a bad disease and doesn’t matter whose fault it is why it happened, it happened, and will hit like a tsunami next time around. If you don’t recall the panic buying and peak prices/sales in 2007 I’m not sure what planet you’re on/or from totorro.

Looks like someone finally has it figured it out. Keep your head in the sand though,it’s the easiest way to stay in denial.

Canada’s Credit Cycle Has Never Been This Desynchronized From the United States

A rapid private debt binge is nearly over, Macquarie says.

“Canada has entered the very late innings of its super-charged private sector credit cycle, one that has completely decoupled from that of its largest trading partner, according to Macquarie Analyst David Doyle.

“Canada’s private sector nonfinancial debt to GDP ratio (includes household debt and non-financial business debt) has skyrocketed since 2005, rising by over 60 percentage points,” he wrote. “This is a greater magnitude of increase than occurred for the forty years prior (1965 to 2005).”

As a result of this prolonged binge, Canada’s private sector non-financial debt-to-GDP exceeds the comparable U.S. ratio by its highest level on record”

http://www.bloomberg.com/news/articles/2016-02-19/canada-s-credit-cycle-has-never-been-this-desynchronized-from-the-united-states

“I know a couple of young couples with kids who went bankrupt in 2010 because of easy credit/mortgages chasing the market herd in 2007.”

What market herd in 2007? Where were they exactly?

If young couples in Canada are going bankrupt mortgages are not to blame. Mortgages have good qualification processes. Presuming they did not divorce or separate or fall ill the blame cannot be placed on “easy credit” but rather personal spending choices.

So annoying when personal responsibility is completely sidestepped in attributing bankruptcy to mortgage lenders as some part of some big conspiracy theory that removes all power from individuals.

VictoriaVV, you’re wrong on all counts about me. Goldman called oil right but gold could still move up here. Usually it’s do the opposite of Goldman as their track record so far this year is abysmal.

http://www.zerohedge.com/news/2016-02-09/goldman-capitulates-closes-out-five-its-six-top-trades-2016-loss

The world is awash in debt and gold is a safe haven for some. I don’t own any yet at $1700 Cdn., just own a gold junior stock.

Jury is out on the US, many signs all is not right. Could go either way in the near term but many big money managers have been speaking out that US is in a recession or near one and Fed is running out of tools. We know Canada is in the tank and the “ripple” will be heading our way soon.

http://www.zerohedge.com/news/2016-02-19/sam-zell-warns-we-are-already-recession-and-markets-are-still-frothy

“Oh Hawk…. I’ve been reading proclamations with such unwavering conviction such as yours since around 2005. ”

Good on ya Chris, sounds like you should have bought in 2005, I was bullish back then but not in the right situation to buy back in, but that’s life. If you got kids and plan to stay 10 years plus and can wait out any nasty correction or crash then fill your boots, I’ve always said that.

So many now are into flipping and/or expecting instant fast cash and it’s those who will get burnt. I know a couple of young couples with kids who went bankrupt in 2010 because of easy credit/mortgages chasing the market herd in 2007. It was sad to watch.

Look how the Vancouver SFH chart separates from the rest of the condo and attached house market in 2003 to 2005 range. It only makes sense it will pullback here too and maybe faster with being a smaller market.

The market’s never been more dangerous than ever before. Paying $100K over for a dump in need of another 100K reno is insanity. Now we have the world entering another experiment with negative interest rates as the next savior after zero down, 40 year mortgages, quantitative easing, and bailing out CMHC to the tune of billions in 2009 to save the real estate and financial markets. But people will pay 100K over ? This can’t end well.

Hawk is just kicking himself for acting on his fear of a crash by selling in the low of 2009 with the hopes of re buying a much nicer place after the crash. Put all his money in gold right before Goldman warned of the big gold short.

You only read this blog if you want to buy a house in Victoria, or you own a house here and are tracking data.

Goldman just warned about gold dropping again, and with all the positive USA indicators, watch gold drop again very soon.

Timing ANY market is for fools, buy what you can easily afford after you have a large safety fund and a solid career, invest in index funds and hold for 30-40 years, and get on with your life.

Oh Hawk…. I’ve been reading proclamations with such unwavering conviction such as yours since around 2005. Back then I was reading blogs about the Vancouver market and there were all sorts of comments like yours indicating the top and how everything was going to collapse. I’ve got a 2006 chart of the Vancouver prices (Vancouver Real Estate Board) and it looks the same as it does now – pretty much straight up! At the time I thought Canada was going to follow the US but I’m still waiting. I gave up and bought in 2009 in Victoria and glad I did (but also wish I stayed in Vancouver and bought there!). My kids are growing up and wasting time trying to time the market for a primary residence is not worth it. We’ve got a nice place we’re happy in, the mortgage is rapidly going down and the value is (currently) going up.

Oh but it will, totoro. It’ll be like a wave.

Even real estate in Port Hardy will be affected, because it’s also in the path of the wave. We all know how waves work.

Except “later” is having a tough time coming.

The crash has been sure to happen in 2008, 2009, 2010, 2011, 2012, 2013, 2014, and 2015.

2016 is the year! If not, it has to be 2017!

Well, that sounds like a fine plan B to me. I personally am not okay to remain a renter forever for a number of reasons. Those that are have a big advantage as they can keep some emotional distance from the ups and downs of trying to enter the market and avoid any sense of urgency.

As far as the crash theory goes, who knows what will happen next really. My best guess is that Victoria will not have a big drop. Back five years ago I thought with the big run up we would have a small decline: instead we had flat.

Given the long flat period here vs. Vancouver’s run up I don’t think it is likely that our market would crash in tandem with Vancouver if there was a big bottom of some kind although it might cause prices to stall here. I don’t know the Vancouver market well enough to have any opinion on a crash vs. flat. Can’t go up at that pace forever.

What history does show for the housing market is that prices do rise long term faster than the pace of inflation. This means income doesn’t keep pace with housing costs and there will generally be a long-term advantage to buying sooner. Our parents really did have it easier than we do when it comes to buying a house.

Plan B? You mean I continue to rent very cheaply, save thousands, be mobile, comfortably afford life’s joys without scrimping, and have a pile of cash at my disposal ? No prob for me, my life isn’t built all upon real estate to be healthy, wealthy and wise. If it happens great, if it doesn’t, no big deal.

I may be wrong and could be 6 months or so early but it’s coming. 2008 never cleaned up it’s mess and it’s only worse now.

ICYMI, Garth had a good one on bubbles yesterday.

“Just as dot-com stock far surpassed justifiable levels based solely on sex appeal and demand, so has residential real estate become riddled with risk, ripe for revenge. Real estate’s seen as the elixir for the masses, an always-winning lottery ticket and a riskless play. Children expect better houses than their parents ever had. Renters are told they’re morons. Moms turn into banks. The herd moves as one. When numbed, brainwashed posters come here to predict single-family Van houses will average $5 million in five years because, you know, they’re going up, it’s clear where this is headed. The wall.

When prices flatline and fall – whether it’s a terrifying descent or a sickening grind lower – equity will be peeled back to reveal the largest pile of debt in Canadian history.

Later, it will seem so obvious.”

http://www.greaterfool.ca/2016/02/18/the-bubble/

What is your plan b if you are wrong?

It’s only February Fireecology. Wait til summer when the buyers are all gone and the inventories are up. Market tops disguise themselves easily to those who are stuck inside the bubble. Just look at Vancouver chart, you think that’s going to keep going straight up much longer ? Parabolic charts have the scariest end results.

Now that the message is out the HAM are being watched on how they do business in Vancouver with their shady realtors and shell companies, I expect to see a strong pullback by summer. When that happens, Victoria will be caught in the down draft as the headlines change to reality.

Regretting not buying a year ago making paper profits is a waste of energy, you would never sell if you bought so you would have nothing but a bigger ego because you were “so smart” to buy when you did. It’s like missing out on a hot stock, then look back months later and it’s come back to earth. BC’s economy is built mainly on real estate, and when this ridiculous mania finally subsides, it’s game over.

New CMHC rules for min. Downpayment took effect on Monday and I haven’t seen much comment on this. New buyers need a min. 5% down on the first 500k of purchase price and 10% down on the next 500k up to 1 million. What effect if any will this have on the SFH listings here? Was January’s craziness partly to blame on the lead up to these new rules taking hold? I’d love to know what % of buyers are first time home buyer’s with the min. Down payment who are actually affected by this change. Seems like the rule change was directed at cooling Vancouver and Toronto but Victoria will be caught up in it as well.

Hawk – I admire your optimism, but when a line is climbing at its steepest rate, that is the very opposite of a ‘top’. Well, other than a bottom, I guess.

Leo’s right. I was here five years ago. There was me and maybe two other people who were fairly bullish. It was laughably lopsided. Every second comment posted was about the “crash” that was “imminent” and “not hard to foresee.”

Today, the blog is probably as evenly balanced as I’ve ever seen it.

As sage individuals on this blog have repeated often, it’s exceedingly difficult to time the market. And not only that, but life goes on — and waiting a long time also has its nonfinancial and financial costs.

Hyper inflation would be kinda cool, because inflation would effectively decrease your mortgage principal amount. But I guess you’d need to be locked in to a five or 10-year fixed rate mortgage to really take advantage.

That kind of thing has happened before. My boomer parents tell of a friend who, in the early 80s, in Calgary, received a weekly phone call from the bank asking him if he wanted to refinance or break his mortgage, because the bank stood to lose so much money on that particular agreement.

Neat fact, by way of conclusion: the wartime debt incurred by the U.S. was never really paid off; the debt just got smaller because of inflation and rising G.D.P.

By the way I’d imagine that the number of realtors would be picking up again now with the market. I believe it was declining for a number of years.

We bottomed out at 1190 last year…up to 1245 now.

Offer your next 20 desirable listings at 1% and see if they sell any slower, have fewer views/showings than the ones at 1.5%. Repeat at 0.75% and 0.5%. For science!

Although if you showed that it makes no difference you could be shooting yourself in the foot

As illustrated by my example below there is little competition in the market place. Actually, that’s wrong and let me rephrase, there is very little appetite from the consumer for alternative models. The models and competition are out there and easily accessible via simple google search but the consumer I guess is cool to split ways with 15,20,30,40k?

If 98% of consumer are choosing the option of 3+1.5% in a free marketplace that means I am already undercutting 98% of the market at 1.5%. There isn’t really a demand from the consumer to go 1% cooperating, for example.

Offer your next 20 desirable listings at 1% and see if they sell any slower, have fewer views/showings than the ones at 1.5%. Repeat at 0.75% and 0.5%. For science!

Although if you showed that it makes no difference you could be shooting yourself in the foot 🙂

By the way I’d imagine that the number of realtors would be picking up again now with the market. I believe it was declining for a number of years.

@Marko. Theoretically, I agree with you — a mere posting/alternative model appears to be a no brainer. The cooperating commission is pretty key though — my realtor was flexible on the listing side. I’ve also sold three properties with him and may well list another in a year or so, if /when the market on the peninsula picks up. If i was selling my principal residence, I might consider something different (given different tax considerations).

No fair enough. I know where you are coming from especially if the commission is a write off.

I have to get rid of my Honda Civic right now and I am going to go through a dealership versus going for the extra coins via usedvictoria….just don’t have the time or patience given the difference involved. Would take it on for 3-4k but not for <2k.

I thought you recommend offering close to full buyer’s agent commission?

I don’t believe in swinging for the fences (i.e. offering $1 cooperating commission) and yes for the past 5.5 years I’ve been mostly running 1.5% cooperating (fairly close to 3%100k+1.5%bal, ***commissions may vary) with great success but right now there is opportunity, depending on the property, to go below that in my opinion. However, with 98% of listings going with full pop I don’t think anyone is in agreement with my opinion 🙂

I was involved in a bidding war yesterday with my buyers where the cooperating commission was $3,000. I certainly didn’t ask for additional commission as I didn’t want to jeopardize my clients’ offer and it is not something I do in general. Not sure what the other REALTORS® did?

Right now if you have a house in Gordon Head, for example, you can go lower than 1.5% in my opinion.

At this point with the upward market pressure the commission to sell my house would be more than what I paid to frame it……..what da????

https://www.youtube.com/watch?v=HD3CXGwh-CE (video I made in 2014)

Marko, where is the “solid SFH inventory”? I suppose not in the Victoria/Oak Bay/Saanich areas

Do you have Saanich West, Esquimalt, Vic West, etc? If your PCS system is under a million a lot of listings in Victoria/Oak Bay/Saanich East are cut off for you.

As someone who has been looking to buy for the past few years and does not own a home, the change in the market over the past year is disgusting. Regrets…regrets…I think of houses I could have bought in 2013 and 2014 like old romances I let slip away

Highsight is easy, looking forward is the difficult part.

Marko, can you please tell me what 1829 Fairhurst Ave sold for? And DOM? Thank you. 22 days on market and $589,000.

Marko, can you please tell me what 1829 Fairhurst Ave sold for? And DOM? Thank you.

@Sweethome. I think sadly there are a lot of people in your position that could have bought but listened to the doom and crash peddlers here on HHV and others.

Who knows, maybe there will be a massive correction back to 2007 (2014-15 prices, same thing). And maybe there will be an even bigger global correction where the entire country goes bankrupt and house prices drop 50% or more. But even in that situation it would take years for prices to come down. And it would mean a huge stock market and employment crash, with possible hyper inflation from the expected monitory easing that would happen, so fingers crossed your savings are not in stocks, bonds, gold, or cash.

I thought you recommend offering close to full buyer’s agent commission?

Marko, where is the “solid SFH inventory”? I suppose not in the Victoria/Oak Bay/Saanich areas. Only a few listings showed up in my e-mail from my realtor today. One was a house in Henderson, near UVIC. It’s a small, dated 1500 sq.ft. rancher on crawl space that sold for $675K in May 2015; now listed at $795K. Now, please tell me that won’t sell for over asking?

As someone who has been looking to buy for the past few years and does not own a home, the change in the market over the past year is disgusting. Regrets…regrets…I think of houses I could have bought in 2013 and 2014 like old romances I let slip away…

@Marko. Theoretically, I agree with you — a mere posting/alternative model appears to be a no brainer. The cooperating commission is pretty key though — my realtor was flexible on the listing side. I’ve also sold three properties with him and may well list another in a year or so, if /when the market on the peninsula picks up. If i was selling my principal residence, I might consider something different (given different tax considerations).

My listing is one of those, Marko. Bring on the bidding war!

I just went through the 55 properties listed today.

53 offering 3%100k+1.5%balance cooperating commission

1 offering 1.75% (military transfer, what Brookfield pays)

1 (my listing) offering 1.5%

Little sad that after 5.5 years of pushing an alternative model no one is embracing…..it is a freaking hot market out there! Paying full pop makes zero sense.

The nice thing about hoping one way or another is that it amounts to about a hill of beans.

You should have seen the site 5 years ago, it was way more bearish! Personally I was predicting a crash up to about 2011/12, then I was thinking a slow decline, and then I was thinking flat. Currently I am pretty bullish for the next year at least.

Also neutral posts are boring 🙂

“House prices rising help way way more people then flat or crashing.”

Sorry, but that is idiotic, it only helps keep the bubble afloat. The market is up 10% from a year ago, how much greed do you need ? Sell and reap the profits.

“A ton of solid SFH inventory hitting the market today.”

Looks like a bunch of people have now seen the light and see the top is in. This is great news.

My listing is one of those, Marko. Bring on the bidding war! 😀

Why would we hope this is the end of a recovering market? Maybe we should have the posts on this site neutral rather then slanted towards comments of prices should be crashing?

A lot of readers here want their house prices to finally move up after 8 years of flat (read: decline w inflation).

House prices rising help way way more people then flat or crashing.

A ton of solid SFH inventory hitting the market today. Will be interesting to see if this continues if there will be enough buyers out there to continue the bidding wars.

Interesting court foreclosure today on a property along Filmer Road The home needed a new roof and drywall repairs and had not been updated since it was built in 1957. Cost between $25,000 to $35,000 for repairs to make the home livable. The basement was basically unfinished and had a small bathroom.

The cost to update the home and finish the basement to modern standards would likely be over $100,000. The basement was basically unfinished and had a small bathroom.

Appraised for court at $375,000 by an unknown appraisal company

BC Assessed Value at $466,000

Property listed by the agent at $409,900

Initial offer presented at $425,000

Court date set for 30 days later

Over 100 showings of the property during the 51 day listing period

And on the day of the court, the room was packed out into the hallway, there was 6 sealed offers presented.

Highest offer accepted was $538,000 or $500 per finished square foot.

The day before, Tuesday, in court. 1 person showed up to bid on a house on 11 acres on Salt Spring Island.

Listed at $445,000

Initial offer at $445,000.

Assessed value of the property $603,000

Property sold at $445,000