Aug 14 Market Update

Weekly numbers courtesy of the VREB.

| Aug 2017 |

Aug

2016

|

||||

|---|---|---|---|---|---|

| Wk 1 | Wk 2 | Wk 3 | Wk 4 | ||

| Unconditional Sales | 157 | 322 |

883

|

||

| New Listings | 222 | 431 |

1120

|

||

| Active Listings | 1932 | 1915 |

2094

|

||

| Sales to New Listings | 71% | 75% |

79%

|

||

| Sales Projection | — | 777 | |||

| Months of Inventory | 2.4 | ||||

Detached homes are still being outpaced by condos, with 29% of detached homes in August going for over ask compared to 39% of condos. At 21 days, it takes almost twice as long to sell the average house as the average condo right now. To keep some perspective that is still relatively low given that two years ago it took 35 days and the year before it took 54. However we can already see price cuts are necessary to shift houses, with the average sell price to original list dropping to 98.6% for detached while it remains over 100% for condos (this measure varies from 95% in declining markets to 103% in hot markets).

Inventory continues it’s long slide that will almost certainly accelerate going into the fall. If you think the selection stinks now, it’s not going to get better until next spring unless there’s massive shock to the market to disrupt the normal seasonal trend.

Actually Hawk, the gravel road was more interesting than your ten minute delay on the Hat…

Bamfield was, btw – beautiful comparable to Tofino yet without the crowds!

haha! If oops’ scenario comes into effect I can see the headlines now:

‘Justin Trudeau seizes entire neighbourhoods of Toronto’

‘Liberals bankrupt the middle class’

The passage of those rules aren’t that far fetched. But such an overt declaration of war on their own voter base is political suicide. No way those rules are going into effect. If they did then expect the conservatives to reorg away the entire OFSI with their soon to be majority government.

New post: So much for the retirees coming here. https://househuntvictoria.ca/2017/08/17/population-change-in-victoria/

Totoro: “Foreclosure is expensive and if there is equity to support the foreclosure costs and payments being made no need to foreclose.”

They seemed to have that figured out totoro.

“Undue reliance on collateral can pose challenges, as the process to obtain title to the underlying property security can be difficult for the borrower and costly to the lender.”

I think that you are confusing the bank’s desire to make money with OSFI’s desire to ensure the integrity of the banking system.

Perhaps their risk management assessments have concluded that the biggest problems are Toronto/Vancouver and all of the other markets just end up as collateral damage.

Again, this is another situation where everyone is painted with the same brush because a minority created a substantive issue for a supervisory body.

You know, similar to a minority of people taking advantage of incorporation to avoid taxes so the Government brings in wide sweeping legislation to ensure that everyone pays their fair share. lol.

I think the doctors and the dentists were saying it wouldn’t make sense to go after them. Canada needs more physicians and this would just encourage them to move. Why would they target doctors, dentists and lawyers?

@torontoro

It’s all good, no? We all wait & then buy? @ Hawk don’t move quite yet

This is a consultation document oops – not a set of rules. It is in draft. Highly unlikely be applied upon renewal where payments have been made imo – makes no financial sense for a bank to foreclose unless there is insolvency and breach of contract via non payment of debt. Foreclosure is expensive and if there is equity to support the foreclosure costs and payments being made no need to foreclose. Where there is no equity and payments being made the lender will go negative on foreclosure.

Helocs will be impacted if values fall – as they are currently.

totoro: “From what I read we are talking about draft guidelines – not “rules”.”

<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

Guidelines – not rules except when there is non-compliance. Totoro, OSFI is creating these rules to deal with circumvention of their previous legislation.

“A FRFI should not arrange (or appear to arrange) with another lender, a mortgage or combination of a mortgage and other lending products (secured by the same property), in any form that circumvents the maximum LTV ratio or other limits it establishes in its RMUP, or any requirements established by law, i.e., no co-lending.”

Non-compliance with the Guideline

“Where a FRFI fails to adequately account and control for the risks of underwriting or acquisition of residential mortgages, on a case-by-case basis, OSFI can take, or require the FRFI to take, corrective measures. OSFI actions can include heightened supervisory activity and/or the discretionary authority to adjust the FRFI’s capital requirements or authorized leverage ratio, commensurate with the risks being undertaken by the FRFI.”

“It is in no-one’s interest, to apply initial borrowing criteria to renewals where someone is in good standing and has made their payments, not to mention that the equity position upon refinance will be quite different for most borrowers.”

They will ensure that the banks retain their loan to value ratios whether it is a new mortgage, renewal or refinance. They are outlining this directly in your quote. The FRFI should update the borrower and property periodically …. don’t wait until renewal.

“FRFIs should update the borrower and property analysis periodically (not necessarily at renewal) in order to effectively evaluate credit risk.”

…and what do you think they will do with HELOCs when they are out of whack because of declining house prices.

“OSFI expects FRFIs to limit the non-amortizing HELOC component of a residential mortgage to a maximum authorized LTV ratio of less than or equal to 65 percent.Footnote 11 OSFI expects the average LTV ratio for all HELOCs to be less than the FRFI’s stated maximums, as articulated in its RMUP, and reflect a reasonable distribution across the portfolio.”

….. and when things start to fall apart….

“Realistic, substantiated and supportable valuations should be conducted to reflect the current price level and the property’s function as collateral over the term of the mortgage. Consistent with Principle 2 above, comprehensive documentation in this regard should be maintained.

FRFIs should ensure that the claim on collateral is legally enforceable and can be realized in a reasonable period of time or, absent that verification, ensure that title insurance from a third party is in place.”

“There is zero advantage to forcing a sale at that point for anyone. I highly doubt this will be what is applied and it is certainly not what current practice is.”

I highly doubt, I really hope, they wouldn’t really ….. how could they do this. I don’t know about you totoro but “consequential amendments” doesn’t give me a warm and fuzzy. They are going to make sure the banks survive even if you don’t. The loose lending created this bubble and they will not let the banks “pop” as well.

http://www.osfi-bsif.gc.ca/Eng/fi-if/rg-ro/gdn-ort/gl-ld/Pages/b20_dft_let.aspx

“Once the changes to Guideline B-20 are finalized, OSFI intends to make consequential amendments to Guideline B-21 – Residential Mortgage Insurance Underwriting Practices and Procedures.”

Where do you get that from. From what I read we are talking about draft guidelines – not “rules”. Even in the draft guidelines re qualification at renewal is not a “rule”.

http://www.osfi-bsif.gc.ca/Eng/fi-if/rg-ro/gdn-ort/gl-ld/Pages/b20_dft.aspx

It is in no-one’s interest, to apply initial borrowing criteria to renewals where someone is in good standing and has made their payments, not to mention that the equity position upon refinance will be quite different for most borrowers. There is zero advantage to forcing a sale at that point for anyone. I highly doubt this will be what is applied and it is certainly not what current practice is. Mortgage renewals generally happen automatically unless you are changing lenders or have a poor history of paying.

Barrister

August 17, 2017 at 5:10 pm

I suspect that the banks will be given some discretion when it comes to mortgage renewals that are in good standing and for a principle residence.

<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

Nope, OSFI isn’t going to give that kind of discretion to the banks, Barrister because the banks were at least in some part complicit in circumventing the previous legislation.

These are rules, not guidelines.

I suspect that the banks will be given some discretion when it comes to mortgage renewals that are in good standing and for a principle residence. Anything else they will apply the new rules.It will have some impact on the market but it will smooth out over a few years.

3Richard Haysom: “In other words, the Government in trying to avoid a housing crisis, is going to cause one…

Leave it to Government to screw everthing up, look no further than Ontario.”

<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

I’m with you on the whole Government screwing everything up, Richard, but the blame for this legislation falls squarely on those bright lights that circumvented the previous legislation.

OSFI only became concerned when the banks started to take on “unexpected” risk. CMHC was shouldering all of the risk beforehand and OSFI was a happy camper.

It’s not within their purview to moderate the housing market. They are simply negating the risk factor to the banking system.

Any real estate agent, mortgage broker, lender, etc. that pointed naive buyers around the previous qualification rules should be sued by those same buyers. The buyers will ultimately be the ones to pay for their professional’s obfuscation.

“assessed as to your new terms, not the old ones under which you were qualified. For rich kids, if your parents co-signed with you and they are now in a pension income, you better watch out as well…just to make those around us a bit wiser; oh and all HELOCS will also be reassessed…

Going to be an interesting time…”

In other words, the Government in trying to avoid a housing crisis, is going to cause one…

Leave it to Government to screw everthing up, look no further than Ontario.

@cadbarosaurus

Also to note, if your partner goes on mat leave, or one of you changes your job status e.g., from a full time government position to contract or consulting you would be assessed as to your new terms, not the old ones under which you were qualified. For rich kids, if your parents co-signed with you and they are now in a pension income, you better watch out as well…just to make those around us a bit wiser; oh and all HELOCS will also be reassessed…

Going to be an interesting time…

This worries me as well.

As to gridlock, I hope that increased cycling infrastructure, increased downtown density, expanding westshore commercial centers, and an increase in telecommuting help there.

“Victoria population could easily double with more condos approved over the next 15 years.”

You wouldn’t want to live anywhere near here with double but odds are it will never happen, just like your oil to $80 call, and house prices going up 20 to 30% more.

Then you attempt to go to a credit union or other alt lender and hope they loan you the money. Or sell. If they don’t, or you can’t (ie you owe more than it’s worth) , then you either pull some kind of Frank Abagnale or get ready to foreclose.

Cities do have a size were there is maximum efficiency. Growth past a certain point has some serious negative impacts. generally the optimum population size is somewhere around 250,000 depending on other variables. There are threshold to every aspect of the infrastructure which people dont appreciate. The simplest example is the number of vehicles that can operate on the road network before you hit gridlock. At a certain point a 10% increase can cause far more than a 10% slowdown. We actually have a real limit to water available to us and if this type of dry summer is more the norm than the idea of doubling the population is very questionable.

The rate stress test coming in the fall: what happens if you own a mortgaged home and then you do not pass this stress test upon renewal?

Introvert:

You sound so much like my dad; there must be a drop of Scottish blood in you somewhere. I have yet to buy a brand new car and the closet I have come to it is to buy last years model.

Victoria population could easily double with more condos approved over the next 15 years.

Introvert do you feel like Victoria is at its max already?

We’re much the of the same bent when it comes to spending. Minimal university debt due to jobs and a bit of family help, buying used everything, only recently bought a used car with cash, go camping and small road trips for vacations, not buying into consumerism as much as possible, etc.

@Introvert

Wow, pretty close to my story I bet!

My house isn’t a million (but I love your optimism!). It’s 7 or 800-something, and when we bought in 2009 it was 500-something.

Some info by way of answer:

• My partner and I had no university debt thanks to jobs and parents/grandparents’ generous help.

• We always rented very modest places ($500/month for our place in Calgary and then in Victoria). The one in Victoria was a basement suite that had a hot plate instead of a stove and a bathroom that wasn’t much bigger than one you’d find in a large motorhome. Privation like this allowed us to squirrel away enough for an 18% down payment.

• My partner makes much more than me, but our household income (rental included) is not astronomical. No one is a doctor, lawyer, or the head of ICBC.

• Lastly, we don’t shoot ourselves in the foot. We don’t buy new cars, or lease them (we’ve never owned a car that was less than 10 years old). And we don’t sink our money into a lot of consumer goods or go on fancy vacations.

Does that sort of answer your question?

Shitty weather.

No. Cities, like anything, can’t grow infinitely.

Thank you.

Another weak Golden Head slash of $20K at 1554 San Juan Ave. Going to need more than that with all that competition. One more South Oak Bay slash of $70K at 745 St. Patrick St.

Several “hot” 2 bed 2 bath condos in the core slashed but anyone looking knows which they are.

Is there PST on real estate commissions in BC? Or is it just GST? THANKS.

Just for fun…

Realtors warn that if Toronto housing market continues to collapse everyone could one day afford house

After a nearly 30% decline in value, realtors across Toronto are concerned that if the market continues to falter someday in the near future everyone could afford a house.

“I don’t want to alarm anybody, but this is happening as we speak,” said Parkdale realtor Carol Mert. “If we can’t pull out of this tailspin three, even four million people could suddenly find themselves with a roof over their heads.”

Recommendations ranged from rescinding the foreign buyers tax to burning down 20% of the homes in the GTA, but if something isn’t done soon Toronto will be looking at a city full of homeowners.

https://www.thebeaverton.com/2017/08/realtors-warn-toronto-housing-market-continues-collapse-everyone-one-day-afford-house/

House sold 3 days @ ask.

That’s fine, I’m in it for the long haul and can absorb a couple points of interest rate hikes along the way 🙂

Sellers getting a little antsy

“Because everyone could use more vacation time, the sellers of this beautiful waterfront property would like to add a $25,000 travel voucher (or CASH) Bonus to the buyer agent whose clients purchase this property”

Not as long as it will take you to recover from the crash. 😉

http://realinvestmentadvice.com/wp-content/uploads/2017/04/Margin-Debt-Net-Credit-040317-4.png

Bitterbear yup, household income plays the largest factor in determining affordability. Rough rules of thumb say that your housing costs should be no more than 30% of your income. Some people disagree with that amount, but it’s something to aim for.

Yup, agreed that affordability isn’t the only piece of the puzzle here. If rates rise 2%, we will likely see a lot of current owners who were already stretching affordability get nailed.

And yup, just a year now. How long have you been calling Victoria RE a bubble?

“One of the main measures of affordability is the monthly carrying cost. A $300k 25yr mortgage at 10% is the same monthly carrying cost as a $600k 25yr at 2.5%. Lower rates helped drive prices up, but the affordability might have stayed roughly the same.”

The US market tanked on a couple of points rise and a debt bomb way smaller than Canada’s. You don’t get that you may not qualify when the 2 point stress test comes in so that may be the kicker that pushes this over the cliff. It’s about qualifying for the mortgage as rules tighten severely all the way down in a crash, and not about affordability alone.

“I don’t have the historical context on this site, but how long have you been calling the Victoria housing market a bubble, Hawk?”

How long have you been a homeowner Garden ? A year ?

In the calculation of affordability, isn’t household income considered? I would have thought that affordability would have been something like rate(mortgage/term)/income.

One of the main measures of affordability is the monthly carrying cost. A $300k 25yr mortgage at 10% is the same monthly carrying cost as a $600k 25yr at 2.5%. Lower rates helped drive prices up, but the affordability might have stayed roughly the same.

I love how they characterise increasing rates as compromising affordability. Affordability has been compromised because of FALLING rates.

Hmmmm it’s uncanny how this blog seems to mirror HHV. Heck, we could probably even give them similar names like John Dollar, Hawk, Leo, Gwac etc.

http://www.mortgagenewsdaily.com/5172005_Housing_Bubble_2005.asp

Robert

on

I dont expect to see the kind of appreciation we have been experiencing in so. ca (+20%/yr), but I do expect to see an appreciation of +3-6% a year for years to come. Barring a monumental catastrophy, I dont forsee any great loss of housing price (a drop of more than 10%?).

Report This Comment

Robert

on

I have been reading about the so called housing bubble for about four years now. We sold our house in 2000 (big mistake). I kept reading and listening to others speak about the looming bubble in So. Ca., so we waited to purchase a house. I expected the prices to fall in 2001, 2002, 2003 and finally after seeing that was not to be the case, we purchased a four bedroom house in Simi Valley in 2004 (for 385K). The house across the street from us just sold for 515k.

SRB

on

Anybody — can you advise what the average residential real estate value trend in % increase has been in Texas and Arizona, over the past 5-10 years? Thanks, SRB

Jonas

on

I was born and raised in Cali. I feel really sorry for anyone who has purchased a house within the last 2 years. Within the next 5 to 7 years the prices WILL go down to normal. Anyone who thinks Cali home prices have just risin to a justified 8:1 ratio to incomes, is more stupid than someone who has taken the $100K out of their house to buy a new car. To answer a previous post….NO, now is not a good time to buy a house in Cali!!!

I don’t have the historical context on this site, but how long have you been calling the Victoria housing market a bubble, Hawk?

“Calling it over in 2 xxxxxxx months in David Lereah BS land.”

OK Hawk, going to hold it to ya!

Meanwhile, TD bank speaks reality that will kill prices everywhere. Toss in US rate hikes on top of Canadian hikes and you could expect 5 or more.

“TD Bank economist Diana Petramala expects the Bank of Canada to hike rates three times in the next 18 months, so mortgage rates should continue to trend higher.

“As such, housing affordability is likely to deteriorate broadly across Canada,”

“Let’s drop the pretence,” Douglas Porter wrote in a commentary. “The Toronto market — and the many cities surrounding it — are in a housing bubble.” – Feb/2017

“My biggest concern here is that speculation will now take full command and the market will absolutely run out of control, eventually leading to a serious correction,” Porter added. – March 2017

“Little doubt foreign buyers are pumping up Victoria’s housing market, says BMO chief economist”; April 2017

“This housing market needs a bucket of water thrown on it and soon,” Doug Porter, ” – April 2017

“Nothing to see here folks” – August 2017

Like all bankers they are the worst hypocritical liars and will be til the bitter end. Dougie won’t know what hit him between the legs and he either missed out on 1981 or was still in diapers.

Bubbles take a year or two to play out and the fall out from deals crashing is going to be a disaster. Calling it over in 2 fucking months is David Lereah BS land.

Do you think the US housing bubble will burst?

David Lereah, chief economist for the National Association of Realtors, March 2007.

Honestly just keep doing it. Think about how long it took to learn even a little english. It takes kids over a year from their first word to speaking in sentences. 20 minutes a day and you’ll get there over time, the important part is doing it.

“There’s no canary in the coal mine here and this is not the same orbit as the U.S. in 2006-07 when it was truly a national bubble,” the economist added”

Well, there’s confidence! Have at him Hawk! Can’t wait to read your response!

Sorry Hawk, we’ve both now missed out according to BMO’s chief economist.

Economists say the Canadian housing bubble — long feared to be vulnerable to a dangerous pop — is now officially dead

“It has ceased. It has expired and gone to meet its maker,” said Douglas Porter, chief economist at BMO Capital Markets, parroting a famous Monty Python quote. “This is a late bubble. Bereft of life, it rests in peace.”

http://business.financialpost.com/investing/trading-desk/canadian-housing-market-bubble-has-ceased-without-a-crash-landing/wcm/f1e899d9-1f98-4513-94ab-f7a5fce42b82

Being stuck here while trying to recouver, I just spent some time looking at real estate in Lugano. Bear in mind this is a small town of only about 65,000. Thank god that we already own a house because the prices make both Victoria and Vancouver look dirt cheap. Emailed a RE agent there to ask what the rough price range of our place is there and waiting for a response. Not being to able to get out of the house is a serious pain.

Neighbour was nice enough to set me up with Rosetta stone but I am finding it a real struggle to learn Italian. I am thinking that if I just mumble then I can just learn the hand gestures.

“It is better to be irrational in an irrational market. Follow the herd and the herd will protect you.”

The US herd of debt is surpassing 2007 and credit card delinquencies are on a 2009 level. Never mind, just follow the herd down the road to ruin and you’ll do just awesome in bankruptcy court. Seen friends go through it before, and it’s one sad and ugly place.

“Flows of credit card balances into both early and serious delinquencies climbed for the third straight quarter—a trend not seen since 2009.

Source: New York Fed

The NY Fed noted that early and serious delinquencies for credit cards are rising. This is not a new development either… it’s been happening for NINE straight months: a trend not seen since the depth of the great crisis in 2009.

So US households are more in debt than they were in late 2007… and the credit cycle is turning with delinquencies rising just as they did in the Great Crisis of 2008.

Meanwhile, stocks are at all-time highs. So what happens when the markets wake up to the fact that yet another massive debt bubble is beginning to burst?”

http://www.zerohedge.com/news/2017-08-16/did-fed-just-warn-debt-bubble-beginning-burst

“Yep, every mortgage is an adjustable rate mortgage in Canada. Aren’t we lucky.”

I would like to see the Federal Government endorse 7yr mortgages with competitive rates to the 5yr rate. I think that would add a lot more certainty and stability to the market. Also I would like to see a maximum/cap of 6 months mortgage interest payout for all mortgages as the maximum interest differential penalty, that’s plenty enough blood for the banks to feed off of.

It is my understanding that the lender will do that now, no?

The lender should always do it…..but my guess is it gets missed so as the home owner I would follow up and make sure it is removed.

Ya. I think there’s a lot of people embodying that mentality, though. That’s the very genesis of FOMO. Starting to get tired of that acronym, actually. “FOMO”. I hate acronyms, most especially this morning. Drafting a 20+ page contract, which has about 30 billion of them. Jittery from excessive coffee, too.

Never mind. Vic RE. Carry on.

Local she was being sarcastic I think. About the Herd.

…and not tax deductible. Ugh.

Yep, every mortgage is an adjustable rate mortgage in Canada. Aren’t we lucky.

Oh, god. Totally true, until it isn’t true at all. Good for the people who can do that – I just couldn’t be irrational with the largest purchase of my entire life. Perhaps that will cost me dearly, who knows. In a way, I’m happy with that if it gives me piece of mind.

Richard and Leo’s “buy if you can afford”, in my view, is really the best advice presuming a non-investment motivation. RE markets do move in cycles, which does tend to smooth out the implications of buying high or low, given enough time.

The equation for me though, is more difficult as unlike the USA, you’ll have to keep renewing the mortgage rate into a likely rising IR environment. So I guess the only thing you can do is stress test your own mortgage, presume nominal rates of 5-6%, and absorb the risk that interest rates could go higher than that over the course of the amortization.

There is definitely a line between prudent analysis, and too much. So even if house prices go to where I am comfortable, I suspect I will go into it with some trepidation – what if, what if, what if. I know, you only live once. Take a risk! Nothing ventured, nothing gained.

I just like being able to do that – live. I like my freedom, yet I also would like my own place. But a debt prison is just an awful prospect, and that’s what this market represents to me at the moment.

Maybe I should stop whining, and just move to Tahsis. Great deals over in those parts. Prices are so good, I don’t even think I’d need a job to live there. Retire a few decades early, and never have to look at a Starbucks again. Yay!

It is my understanding that the lender will do that now, no?

As at March 1, 2017, legal professionals and financial institutions are required to electronically submit mortgage releases to the Land Title and Survey Authority of BC. Registered property owners will no longer be permitted to submit a Form C – Release, either in person or by mail to a land title office.

https://ltsa.ca/property-information/remove-paid-mortgage

“Anyone know why CIBC and President’s Choice just divorced?”

“We are excited about the future and our ability to create new products to serve Canadians,” PC Financial spokesperson Lana Gogas said in a statement. “Today marks the start of an exciting new chapter for PC Financial, including continued strength in payments and loyalty through our PC Financial Mastercard products.”

PC probably going into the subprime business at 12% plus rates and credit card gouging for the coming crash. Don’t make money with no fees forever.

@Bitterbear

https://www.theglobeandmail.com/report-on-business/cibc-to-cut-ties-with-presidents-choice-unveils-branchless-banking-brand/article35997321/

@Bitterbear @Leo

My waiting plan is to a point of February 2018 (i.e., after two potential rounds of interest rate hikes, and affects of new B-21 rules can be felt). I may “miss the boat”, but I am ok with that. I moved from YVR to have a better quality of life in Vic. But, grew up in a small town on the mainland where places like Kamloops (not currently – but typically), Nelson, and even Penticton can benefit from my 30s youthful energy, “generally” high-income earnings, and interest in community building and volunteering. Love Vic, but life must go on (esp. where a $760,00 budget buys you a mansion and a half on water with a view).

Anyone know why CIBC and President’s Choice just divorced?

Trump just started a race war and divided the US more than ever. His policies will not go through as the GOP jump ship like the rats they are.

Toss in 100 hate groups in Canada and on the rise and you have a future with a shaky foundation. Everything changed yesterday with that brainless clown and his big racist mouth.

I’d be looking for a major market correction as the large US institutions are again starting to pump trash to their clients disguised as gold like in 2008.

“As a quick aside, I got an email today from a colleague, a self-admitted “very small fish,” who told me he was now getting cold calls from Goldman Sachs brokers offering “very interesting structured products.” I told him the last time I heard stories like that was in the spring of 2008. One of my best friends was getting ready to jump ship from Lehman before it collapsed – he was in the private wealth management group. He told me he heard stories about Merrill Lynch high net worth brokers selling high yielding structured products to clients. He said they were slicing up the structured garbage that Merrill was stuck with – mortgage crap – that institutions and hedge funds wouldn’t take and packaging them into smaller parcels to dump into high net worth accounts. Something to think about there…”

Marko, I think you are dead right. I read books, articles, look at data, charts, listen to experts and it has got me nothing but left behind. My husband has said for years “if everyone else is doing it, it must be the right thing”. It became the right thing only because everyone else was doing it. Now, I’m too old to be diving into half a mill in debt.

It is better to be irrational in an irrational market. Follow the herd and the herd will protect you.

Leo, can you set me up on MLS for listings on Vulcan?

It’s interesting to see the conversation here “normalizing” the past decade in real estate and the mocking of the bear perspective (though Hawk does nothing to help…). With the GFC the global financial system almost collapsed, resulting in prolonged, near zero rates, a huge increase in personal debt and years of flat wages. In addition to the rate stimulus Canadian real estate has benefited from immigration, foreign investment, tax evasion, rampant speculation, a blind eye to money laundering and unenforced regulations in real estate and related areas such as AirBnB. The previous provincial govt. not only ignored these problems, at times they encouraged them.

So… the expectation is for much the same returns going forward? I have my doubts apart from support from immigration and 10-year visas, both of which are dependent on other countries economic health. Price to income, debt levels, stagnant incomes, flat or rising rates, a real estate dependent economy and a new govt. which claims it will address many of the issues, doesn’t seem particularly bullish. There also seems to be a perception if there is a downturn people just remain calm, solvent and mostly unaffected. There hasn’t been a prolonged recession for a generation but with the economy so dependent on ever increasing home prices and not productivity and/or innovation it hardly seems sustainable. Maintaining a cash flow negative “investment” on a depreciating asset while working in a tenuous job market can do a lot to change perceptions…

Yeah

Sorry I was referring to the discharge document. If you pay off your mortgage while stile in a term that you locked into then there is early fee. Your bank will provide those. If you are at the end of the term and still have money left to pay on the mortgage. You can pay that off without fee instead of renewing.

Whatever you do you will probably be charge $75 for the discharge document.

OK, We are about to pay off the mortgage this year. I’m a little in the dark as to how to go about it.

Mike Grace can probably chime in but if there are fees you probably first do you max yearly lump-sum payment and then after that pay off your mortgage.

To remove or not to remove the mortgage from the land title???

Probably best to do right away in my opinion….I see them come up all the time on titles 15 years later (after payout) and then the lawyer has to deal with it.

These are smart people that didn’t think there was a bull case to be made 15 years ago.

I remember when I was doing my masters at UBC in 2010 we had a Phd in Econ prof tell us how he thought his three siblings were idiots for buying homes in Vancouver 2003-2007 time range and it turned out he was wrong…..hope he bought something eventually as the run up since 2010 has been massive as well.

Problem is when you are super smart you tend to overanalyze and residential real esatte markets don’t appear to be rational. You also compete against primarily irrational competition who buy homes not because they need it or it makes sense but they want it and it doesn’t really make sense.

I keep coming back to condo pre-sales…..almost double what they were a few years ago but people are piling in like sheep when a few years it was a struggle to move them. Obviously not sophisticated investors.

@YeahRight

We sold a home a few years ago after being told verbally our mortgage was fully transferable. We finished up with a $9,000 penalty by the bank. They insisted no one had said we could transfer the mortgage even though there were two other people in the office when we asked. We were told we must have misunderstood. So the answer I have to your question is there can be fees to closing out your mortgage. Make sure you have all the facts first, it may be in your advantage to just wait out the term you are currently locked into.

$75 I was told by RBC

It should be in your mortgage document

The law in BC requires for the mortgage company to provide you with a discharge document when the mortgage is fully repaid and after you request the discharge. You must pay the mortgage company to prepare this document, called a Release, but the maximum a credit grantor can charge under the law is $75.Feb 23, 2015

OK, We are about to pay off the mortgage this year. I’m a little in the dark as to how to go about it.

Does anyone have advice about closing fees or what not or a (Canadian, B.C.) link to this information, that we should know about before we settle? Or should I just talk to our mortgage provider about this and I’m asking a dumb question right now (Just like to be prepared before we go in).

Should we pay off early? should we ride it out? Is there penalties to worry about? To remove or not to remove the mortgage from the land title???.

Any info. would be greatly appreciated.

A little chewing gum for those interested. Some of you may recall in an interview on BNN in April this year, Central Bank Governor Stephen Poloz said his bank’s monetary policy had little to do with the state of the Canadian housing market.

“Speculation grows, and it’s fueled by actual money, not by credit — so [speculative homebuying has] got very little to do with the cost of credit,” he said at that time.

However several months earlier while speaking to the Standing Senate Committee on Banking, Trade and Commerce, he appeared to say almost the opposite. 45 second clip:

https://www.youtube.com/watch?v=mlm80x9KPFg

@Leo

Very rational response, and actually is truly appreciated- thank you.!

@Leo, you’d be surprised the # of Americans in Canada

https://en.wikipedia.org/wiki/American_Canadians

According to the Canada 2006 Census, 316,350 Canadians reported American as being their ethnicity, at least partially.[2] There are also between 900,000 and 2 million Americans living in Canada, either as full-time or part-time residents

and registered US voters

http://dailyhive.com/vancouver/vancouver-us-expat-population

Global distribution of voting-age Americans

1.Canada: 660,935

2.United Kingdom: 306,600

3.France: 156,899

All those people need a place to live and you can extrapolate that a % own homes in Canada. Those numbers are nothing to snicker at.

Agreed. Fundamental issue of personal risk tolerance.

Well said Leo.

If you had not listened to bears 10 years ago you’d have a tiny mortgage and you could come here and laugh at them. That’s the bull case. Bears are wrong and have been always.

I would much rather have a smaller mortgage at a higher rate than a large one at a lower rate.

You’re missing the uncertainty in the market. In 2008 we started looking for a house. I was convinced the market was wildly overpriced. But due to a drastic drop in rates it didn’t decline all that much and we bought 5 years later at probably roughly the same price as it was back then. Worked out fine, but if I were living in Vancouver I would have come to the exact same conclusion and been catastrophically wrong.

I’m not bullish on this market. I think it is extremely expensive and I suspect the next correction will be a little different than what we are used to here in Victoria. But I wouldn’t bet on it. And I know people that have been looking since 2003 and thought it was wildly expensive back then and decided to wait it out. These are smart people that didn’t think there was a bull case to be made 15 years ago. I also recall when my sister bought her place in Gordon Head for $380,000 I thought that was a crazy amount. So I have gathered a heck of a lot of humility about my predictions over the years.

Does that mean it won’t crash? Does it mean the bear case is fundamentally not correct? Nope, certainly not. A year and a half ago I said it was a good time to buy. Now I would personally hold off a bit to see what happens. On the way down there will be many smart people that will be proven wrong as well. We can see a glimpse of that in Toronto where there were plenty of smart arguments about why it will keep going up until suddenly it didn’t.

So the argument of “do what’s right for you” is in fact wishy washy. But it’s the truth. How would you feel if you bought and the market dropped $100k? How would you feel if you didn’t buy and it increased $100k? How do you feel about your rental? How do you feel about your job and do you want to stay here? What is your risk tolerance? What is your comfort level with debt? All those things and many more factor in, and the best decision is not necessarily the one that leaves you with the most money at the end of it.

On the other hand,

“over a 5-year window run ups in mortgage lending and run ups in house prices raise the likelihood of a subsequent financial crises. Mortgage and house price booms are predictive of future financial crises, and this effect has also become much more dramatic since WW2.”

https://ftalphaville.ft.com/2015/01/09/2082512/easy-money-housing-bubbles-and-financial-crises/

Damn, not sure I like the sound of this:

Residential real estate, not equity, has been the best long-run investment over the course of modern history.

–“The Rate of Return on Everything, 1870–2015” by Jorda, Knoll, Kuvshinov, Schularick, and Taylor

That’s one of several surprising findings in a new paper from the crew that’s been studying historical economic data on everything from the growth of mortgage lending to the relationship between loose monetary policy and financial excess.

https://ftalphaville.ft.com/2017/08/15/2191433/housing-for-the-long-run/%3Futm_source=Daily+AR&utm_campaign=53e5ed388e-RSS_EMAIL_CAMPAIGN&utm_medium=email&utm_term=0_c08a59015d-53e5ed388e-140320821

585 Falkland Rd in Oak Bay slashed $50K. The greater fool pool is drying up fast.

“I called the Toronto Crash and will call this one when I see the variable change.”

You and everyone else with a brain. FFS gwac, next time lay it out months before not after it’s started.

A 2% interest rate hike will knock prices down more than 10%. Try 25 to 40% with massive debt loads crumbling as refinancers can’t get approved and forced to sell. 2% in this market is the same effect as 5% increase had in 1981.

@Bitterbear

“AFFORD” is what you can afford, not what the bank says you can afford.

Remember Bitterbear, the most likely scenario for house prices coming down is interest rates going up. So you need to focus on the “cost” of ownership and not the purchase price. It may well be that houses drop 10% in value but a 2% interest rate increase could actually make your monthly mortgage payments greater than they would be today. I say “managing your mortgage” is the most important part of home ownership as you can save tens of thousands of dollars if not even into the hundreds of thousands over the lifespan of a mortgage.

Crunch out your numbers, as you know your price range and available funds for downpayment etc. You decide on accelerated mortgage payments if you can afford it etc.

Bitterbear

If you can’t get comfortable than the best thing is to wait and hopefully the market will move closer to your comfort in the future. Home ownership has to be a positive, I can sleep at night situation.

Maybe it’s important to define what is meant by “afford”. “Afford” isn’t what the bank will give you today. It’s what you can comfortably pay (in the context of interest rates, divorce, disability, retirement) as a function of how many years you can comfortably pay it. right now that ratio scares the sh*t out of me.

As long as you figure interest rate increases in your measure of affordability. Those can move a lot in 25 years.

LF, I have the same notion of market dynamics as you do. But it was the right time for us to buy for other reasons in our lives, even during the gong-show of the SFH market last Jan-July.

Local

Its a house not a stock. Trying to market time a stock vs a house is different. You can always buy another stock. Here the asset just gets more expensive. History has shown prices go in one direction over time. You are a very smart guy which means you are trying to rationalize prices to incomes and other things. This is not a rational time and the problem is it may not be for a long time.

I think Richard advice is the best. If you want a house and can afford one buy it and live with the potential up or down consequences.

“Again, Bulls, please, one rational reason why buying is better than waiting.”

1.) If you can AFFORD to buy now…..the worst that can happen to you is, in a maximum of 25 years you will have paid off your house and have the option of never having to pay another mortgage payment for the rest of your life! Good enough reason for me!

The problem with the go-with-the-flow, is that it runs counter to my notion of market dynamics. If everyone and their dog is panicking to get into an asset class, whether it’s houses, bullion, purple widgets, or tulips, that causes me to back off. I’m smart enough to know I’m not “smart money”, and by the time the general public is going ecstatic, that money is quietly pulling out.

I’ll never be able to time the housing market. But I see red flags all over the place: low wages, little wage growth, housing valuations at 8-12 multiples of income, tightening credit, tightening credit standards, unprecedented personal debt levels, unprecedented personal debt acceleration, freakishly low delinquency rates, local market prices making global headlines – just…no way José.

Bitterbear the only good reason IMO is because renting isn’t doing it for you anymore and you want the benefits and accept the drawbacks of buying. We bought last summer because landlords sold places out from under us, and we wanted a stable place for decades to come.

I don’t think timing the market is ever a good idea, whether housing or equities. If you’re happy renting now, then keep renting.

Prices may keep rising and your priced out…

Learner: oh, it could very easily do so. It could also stay flat, or keep going up. I wouldn’t bet on this market either way. We own, but that’s because we wanted the long-term stability of a house here and plan to live in the one we bought for decades. It’s not a short-term investment for us; we’re not specs or flippers.

I do think in the mid term it won’t be that bad for simple supply/demand economics. People seem to want to move here and there’s only so much land available. Prices have gone through an sharp uptick in the last 24 mos, so we could be overvalued now. People could stop wanting to live here. Who knows.

Housing prices being untethered to incomes is problematic, but you have NYC with lower ownership and higher rental rates. Remote work, taking advantage of market arbitrage (live here, work for an SFO tech company) and people starting more tech businesses here could continue to move that needle.

Local and Learner, I have asked for the bull rationale twice. First, I got nothing but conspicuous silence. Then I got, “because it is the right time for you” and a squishy e-hug. Now, I hear because it is better to “go with the flow” (straight down the toilet).

Again, Bulls, please, one rational reason why buying is better than waiting. Is there a set of invisible data that only Bulls can see? A secret handshake? Wink, wink, nudge, nudge? What am I missing here?

Learner

“Please answer how each of these aspects will not affect our current market in Victoria?” Wow I feel like I am writing my exams again.

Dude you are picking 3 variable that may or may not happen in a multivariable market. If you think they will send the market down than sell or do not buy.

With everything that I know about the Victoria economy/ population growth/ interest rates, I am happy to stick to my plus/minus 10% over the next 4 years.

I called the Toronto Crash and will call this one when I see the variable change.

I think people will remember my pig comment about Toronto that a lot took offence to.

That is still horrifying. I wouldn’t borrow that much money for 4 walls if it was the last set on earth.

Gwac, I’ve been picking on you because you’ve been brave enough to give out numbers. I don’t agree with your 10%+- prediction, but I appreciate that you don’t argue underhandedly while thinking you’re clever in doing it.

It’s fine to say that you don’t have anything but intuition to back you up, if that’s the case. In the end it’s all anyone has. If I had to make my own short-term bullish argument for Victoria, it’d probably be “the market can stay irrational longer than you can stay solvent”. I made that saying up myself, just now.

@Gwac:

“With potential mortgage interest increases (BoC Oct 2017 and January 2018…), new B-21 rules (this fall), and China’s clamp down on money transfers (current), you still do not believe Victoria will even experience a small correction from 2017 – 2018…?

Please answer how each of these aspects will not affect our current market in Victoria?

gwac

August 15, 2017 at 10:40 am

OMG ten years of the same doomsday predictions for Victoria yet prices are way up. The boat has left without you. Time to shit or get off the pot…<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

The biggest problem with the little boy that cried wolf was that the wolf finally showed up!!!!

When OSFI legislation comes through in the Fall, every mortgage (insured and uninsured) as well as every renewal will be stress tested. These aren’t guidelines for the banks to hem and haw over, they are rules they will have to follow.

The same people that got around the previous legislation by getting a 20% down payment through their parents or another lender to avoid being stress tested at a rate almost 3% higher will be stress tested at the higher rate upon renewal.

Says the mortgage Nazi: “no mortgage for you”

Somebody that would qualify for a $965,000 mortgage at a 2% rate will now be looking at a mortgage of around $750,000 or less.

That wind you feel in Victoria just might be the wolf this time, Gwac

oops

I will look at my Starbucks barometer. As good as any.

I will watch Home Depot sales and Starbuck sales to judge where we are.

Barrister hope recovery is quick.

Both Leo

People are not rational with their decisions. Their wants and needs are totally different. The pyramid scheme keeps going until rates go up and/or the economy/jobs goes south. Right now rates are falling again and the economy is being propped up by Government spending from Ottawa and soon to be BC.

Gwac: “Funny all those max out people are driving nice cars, eating out for lunch, having their 5 dollar Starbucks fancy drinks.”

<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

Hey Gwac, that could be a bad barometer for this market.

Vancouver Homeowners Tapping Into Equity at Alarming Rates

http://vancitycondoguide.com/vancouver-homeowner-refinancing-surges-27-year-year/

Or they are very indebted. I’ll withhold judgement on it one way or the other until the tide goes out.

I am just recovering from some serious surgery but the plans for moving are underway. The main drawback is my lack of either Italian or German. It is the little things like not being able to read the local paper. Luke, since when has 29 Floors become a mid rise. Which developer did you say that you work for by the way?

Enjoy your trip up island, you might actually notice that there is some vacant land here there . Perhaps a 29 floor mid rise in Mill Bay would improve things as well.

What is the basic question?

@Gwac, answer the basic questions.

Funny all those max out people are driving nice cars, eating out for lunch, having their 5 dollar Starbucks fancy drinks. When I see Starbucks with no lineup than I will call that everyone is over extended.

Like I said trying to put everything on a spreadsheet and figure it all out does not work all the time.

People are very resourceful.

Increasing the number of people at a particular salary level won’t drive the market when that salary level is already tapped out and financing pressures are increasing. Most of those folks are already living in houses that are smaller and in worse condition than they’d like with suites in the basement. Their finances are maxed out and their willingness to compromise is probably pretty close as well. In my opinion, with Vancouver doing what it’s doing, local salaries need to go up or debt carrying costs need to go down for prices to go up. Absent external demand or increases to internal demand, things will probably go own this year.

By the by, there is nothing comfortable about carrying 950k mortgage on a 100k salary. That sounds like a death sentence for me. A literal mortgage. No one should ever do that even if a bank lets them.

Local

Sometimes it’s better to go with flow than to over analyze everything. Sometimes things are not meant to be understood on a spreedsheet.

As long as the population is growing and employment and interest rates are stable than people will find away to afford just like people in Toronto and Vancouver do on the same income but double the prices.

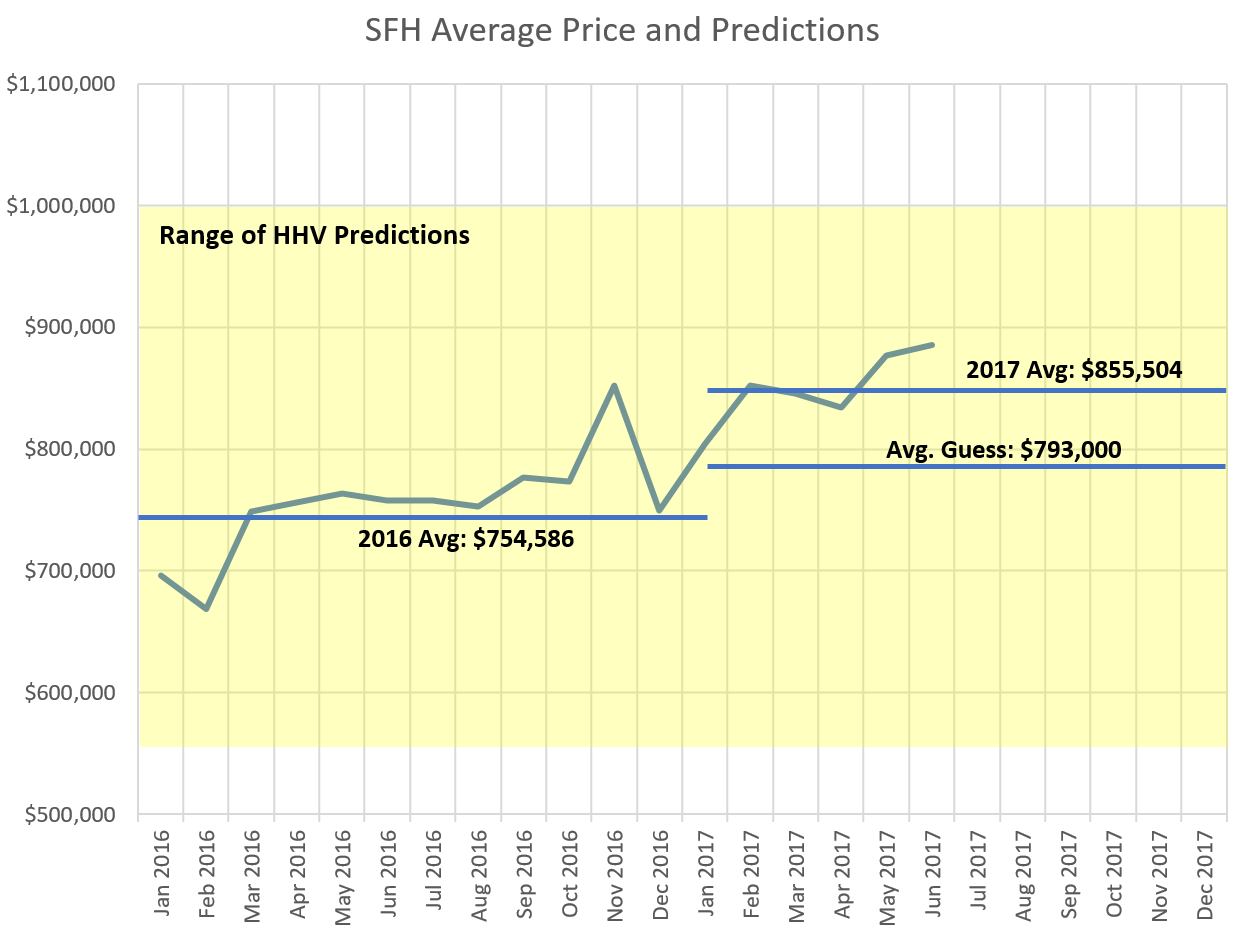

Alright, so we can work with this. SFH/All areas @ $834,850.

A civil servant will generally top out at about 80k. A Director will pull in in between 88k-115k.

So we hire more of them. As a result of this cohort expanding and entering the market, prices increase 10% from $834,850 to $918,835.

This is where it breaks down for me. Gwac, could you demonstrate how this cohort will accomplish this sustainably (equity-based markets aren’t)? Could we assume that as these are new hires, they’re new market entrants?

@john dollar

Finally caught up w/ the last thread and for the first time am going to agree with introvert.

having lived on Arbutus rd for a decade, I don’t know a single person who said that the area they lived in was called Arbutus. Everyone would have said Gordon Head.

@introvert

What is it you do w/ your arts degree that you can afford a million dollar house?

Hawk as I said before I can change with the flow of info. BTW its plus or minus 10% for the next few years. Hey if you buddies go real crazy and hire a whack more Victoria civil servant than it could go more than 10%.

Have fun on The Hat, Luke.

:large

:large

Sounds like an easy excuse gwac, just like calling for the market to keep going 20 to 30% higher just two months ago and flip flopping to a 10% decline.

@ Local fool,

You are right, I am currently selling my property in Victoria, and would like to wait to invest at a more opportune time; however, I still fear that the market will continue to rise and if I wait too long to buy I will be out of luck. BUT, looking at market fundamentals and the data reflects that I should wait and see at least until after January 2018 (2nd posted date by the BoC for interest rate increases if none are announced for October 25 & affects of the B-21 rules can be felt). Hence, a logical and informed answer to my question as I previously noted “is truly appreciated”.

Learner

1230 Victoria Ave down $60K, on it’s second slash and on the market since May 1. I thought everyone wanted to live the Oak Bay high life ?

A few weeks ago I put the screws to another poster asking them a similarly spirited question, (what market metrics will propel home prices to 1500k in a decade) and the response was attempts at redirection, extrapolation, redefinition and a bit of ad-hominem.

So Learner has just posted something similar, reiterated by oppswediditagain, and if you look right after – you’ll note the question so far, gets ignored. It’s not a trolling question. It’s not even provocative. It’s a simple one, and I join those posters in wanting to understand the answer.

If there is a bullish case to make that says market fundamentals not only support current valuations here, but also support prices doubling in 10 years, I would listen to and consider it. The truth is, I am interested in buying, but I am not because I believe trouble is coming. Am I wrong, and I am screwing myself over? Maybe. But I want to understand how so.

Again – I don’t need “proof” because no one knows. But I would like to see a logical case made, that if I poke at it, will withstand that poke reasonably well.

Hawk

The lot has not been bought because I decided I did not want to live there. Sorry If the pot analogy was too close to home.

“Time to shit or get off the pot…”

Says the guy who was pounding the table in Feb/March he was about to buy a lot any day, but still has no balls to pull the trigger.

The bulk of the Asian money is cut off that drove the west coast bubble. I know of a Golden Head family with the Asian student owning it and they are pissed they have to limit it to $50K and can’t risk their friends getting caught. They have a true fear is getting caught by their government as the punishment is nasty, and not some slap on the wrist.

Vancouver is still a bloodbath. Won’t be long til Victoria looks the same.

http://www.myrealtycheck.ca/

@Barrister

Don’t know why you’re not out in Brentwood Bay. Everything you need, none of the downtown riff raff, and the Saanich Peninsula hospital is right there if you’re having health issues. And you definitely do not need to worry about high rises.

Barrister,

Heading camping to Bamfield today – so I will be away from internet for a few days. Yet another reason to love it here – yes there’s so many incredibly beautiful spots within a few hours drive 😉

However I wanted to answer your quip about highrises – a few ‘mid rise’ towers won’t spoil Victoria – if they’re all concentrated either downtown or Vic West or perhaps James Bay. Even at 29 stories, still well below Van. The views from up top would be incredible!

When I was talking about densification in past posts I meant the old SFH developments from the 1960’s or earlier that everyone loves because of decent sized lots and mature vegetation can’t be something that everyone can afford to have. There’s just too many people on too little land. Helps calls it a “handkerchief of land” and she’s quite right. There’s nowhere to go.

I was talking about densifying along major transportation corridors that permeate out from the core – such as Quadra, Burnside, Fort, Shelbourne, etc. This would be more row housing, like you see in the UK, to give people more choice as it seems to me here, the only choice people have is overpriced SFH or strata townhouses/condos. Why don’t we have more freehold row housing here? I wasn’t just talking about high rises – or more accurately – mid rises, which do have their place but that’s not everywhere.

Anyway, hope that answers your question. Now I’m off to the wild west coast. Weren’t you going to Switzerland? I guess that says it all when it’s hard to decide between Victoria and Lugano!

OMG ten years of the same doomsday predictions for Victoria yet prices are way up. The boat has left without you. Time to shit or get off the pot…

gwac

August 15, 2017 at 10:17 am

So we are comparing a mansion in a Detroit suburb to Victoria and looking for a 50% crash in the average SFH. Good luck with that.

<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

Nope, Victoria won’t be that lucky. Sorry to sound like a doomer here, Gwac but I have lived through a number of booms and busts and suffered through the crash of the ’80’s where, yes, a lot of home prices dropped by 50% on the mainland.

What was the salvation back then. Dropping interest rates. Seriously give some consideration as to what the government can do with this upcoming crash. Too many people think that if prices drop swarms of buyers will come in to gobble up the inventory. It doesn’t work that way. If it did I wouldn’t have “suffered” through the “80’s crash.

To borrow from Learner: “So question, even with potential mortgage interest increases, new B-21 rules this fall, and China’s clamp down on money transfers, you still do not believe Victoria will even experience a small (HUGE) correction from 2017 – 2018… interesting.”

maybe this is why house prices in Detroit have been a bad long-term investment

http://www.pgm-blog.com/wp-content/uploads/2013/07/Detroit-population-chart.png

While I perceive that sarcastically, I tend to agree. Detroit is such an extreme, and specific, example. I don’t think what happened there could happen in Victoria, Vancouver, etc.

Detroit was built on, and sustained on, manufacturing – when that was at its heyday in America. And it was awesome while it lasted. Once most of that left, you had white flight and now – Detroit 2017, with ~50k houses.

I don’t think we’ll get anywhere close outside of a massive catastrophe – something way worse than a housing bubble pop. Are we justified in 1000k bungalows? No. But – places like Vancouver and Victoria have so much more going for them than there, and neither are towns that have historically been predicated on one thing. Although more recently, on that latter point…

So we are comparing a mansion in a Detroit suburb to Victoria and looking for a 50% crash in the average SFH. Good luck with that.

Nevermind, mis-read that. That’s total home ownership, not people who own their homes outright.

https://www.cmhc-schl.gc.ca/en/hoficlincl/homain/stda/data/data_003.cfm

3Richard Haysom: “Besides, buying RE should be for the long term not short as in stocks, so who cares if there is a short term correction or pause.”<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

Hey Richard, I guess it depends on what the long term is. The long term is for those well established buyers who aren’t leveraged up the ying yang…….sometimes.

“The house in Rochester Hills, Mich., is up for sale for US$1.99 million (C$2.53 million). Eminem paid $4.75 million for the place in 2003, according to Realtor.com.”

http://www.huffingtonpost.ca/2017/08/14/eminem-selling-detroit-area-house-for-less-than-half-what-he-pai_a_23077315/

“but, but, but that could never happen in Canada.”

Except he never said it. He (Mark Twain/Sam Clemens) actually said:

“I can understand perfectly how the report of my illness got about, I have even heard on good authority that I was dead. James Ross Clemens, a cousin of mine, was seriously ill two or three weeks ago in London, but is well now. The report of my illness grew out of his illness.

The report of my death was an exaggeration.”

He did die in the end though.

It’s 65%. Well below the national average.

Listing price changes, up or down, are generally not a good gauge of the market. In a market like ours, I would suggest that a “slash” more reflects over-zealousness and impatience on behalf of sellers.

There’s likely to be plenty of sellers out there that think that everyone wants their house, wants it yesterday, and for a very high price. There’s enough times recently this has been true to loan some credibility to this belief, to say nothing of the natural bias sellers will have.

In our market, they may think if they can’t sell it in a week, something must be wrong. So they drop the price a bit. Price slashes appear in any market, but it needs to be coupled with additional data to make it more meaningful.

When I start seeming DOM rise significantly, and price slashes regularly exceeding, say, 15%, then it may be a bit of an ah-ha. Not today.

@Garden Suitor,

So question, even with potential mortgage interest increases, new B-21 rules this fall, and China’s clamp down on money transfers, you still do not believe Victoria will even experience a small correction from 2017 – 2018… interesting. Please explain some rational basis for you assessment, it is genuinely valued.

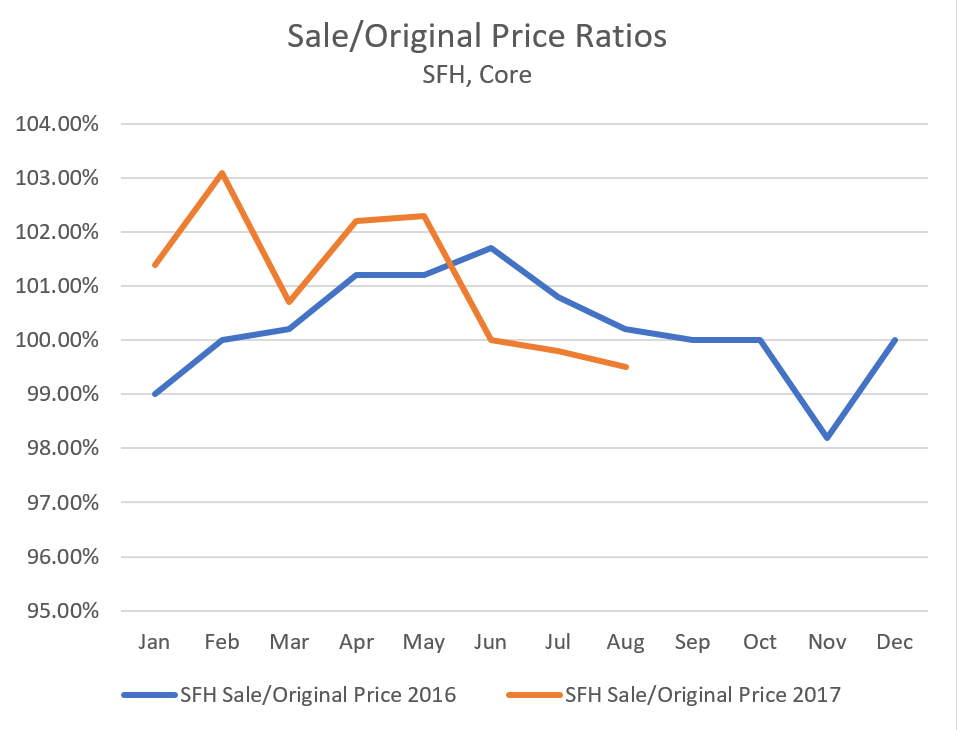

Answering my own question, based on the chart of avg SFH prices from the predictions thread, the % of sale price to original list doesn’t seem to correlate with prices.

Guess price slashes are a poor indicator of where the market will go, Hawk 😉

Thanks for that chart Leo! So around Oct/Nov we had a dip before shooting back up. Does that correlate with the movement on avg or median sale prices?

Hawk

Boom time years are not going to end soon with your socialist friends about to turn on the fire hose full of cash to all their union friends. Victoria will see its fair share since a lot of the MLA need to reward their local base.

Good thing the Ontario min wage is going up. Those realtors are going to need new jobs.

From garths page

” Looks like total monthly GTA sales will come in around the 4,000 market for August. Yikes. Compare that with 6,000 in July (which was down 40% from last year), 8,000 in June (down 37%), 10,000 in May (down 20%), 11,500 in April (down 3%) and 12,000 in March (up 18% from 2016).”

“You cannot just shut the door and tell people to move somewhere else.”

You don’t have to shut the door, they just stop coming like every other peak and bust because the jobs are low paying and don’t pay the bills, or there is a recession which is inevitable after a 8 year run on the stock markets. Business cycles don’t go on forever.

Well said Barrister. Developers will drive this town into a condo ghost town until they milk every last nickel out of the sheep and the flippers will be stuck with no renters who can’t pay their $2000 mortgage a month for a 1 bed.

ICYMI, CTV had a segment on what I was saying a few weeks ago about how downtown traffic is a complete effing gong show and to avoid it at all costs. Who would want to live down there now where bikes rule, cars can’t turn right on a red light, and idiots can’t drive to begin with.

http://vancouverisland.ctvnews.ca/video?clipId=1187528&binId=1.1180928&playlistPageNum=1#_gus&_gucid=&_gup=twitter&_gsc=GbG1H9R

Barrister I understand your concern but what do you do with the population growth. There is no land to build low density. You cannot just shut the door and tell people to move somewhere else. If you want the city to prosper long term it needs to grow and increase its tax base to pay for infrastructure.

The more people who live downtown the less we will see empty store fronts.

Leo S. “If the mandate of the OSFI is to ensure bank stability, is it in their interest to crash the market and risk that stability?”

They are far more concerned with the amount of consumers/banks/subprime lenders working around their previous legislation, Leo.

Too many fraudulent uninsured mortgages will be a lot more destabilizing to the banking system. They will risk crashing the market now to ensure that the banks don’t pay too heavy a price later.

How delightful, they are now proposing a 29 story condo for downtown. Highrises are like rabbits, you never get just one. One of the neighbours is a doctor who works out of the hospital. The bottom line is that the hospital is totally unable to handle the population growth in the GVA over the last ten years.

Strangely enough, I found myself hoping that there is an actual real estate crash since that may be the only thing that will save Victoria from the endless over development. Luke this is where you can jump in and argue how if we just built twenty or thirty more high rise towers that the city’s housing crisis will be solved. Surely all of these extra people will only be using bicycles and will be so healthy that they dont ever need hospital services. Besides a forest of highrises downtown will add to the charm and uniqueness of Victoria. The tourists will love it. Besides how else can the poor Canadian developers join the ranks of the truly mega rich with out more highrises everywhere. Increasing densification will really improve the life of the people that live in Victoria. Gridlock will make you slow down and enjoy the sights of the city. Besides think of all those additional Starbucks locations that you will be able to visit. Should be an interesting situation about ten to fifteen years from now when the baby boomers start dying at a faster rate than they are retiring. Enogh rant for now. Luke, dont disappointment me since I am looking forward to hearing how a super dense city is a wonderful thing although I am mystified why you dont move to Vancouver today where you can enjoy all the wonders of high density today rather than having to wait for it in Victoria.

Huh? Gotta immigrate if you want this stay long term. Or are you talking vacation homes?

“Yet the number of Americans choosing to head north to retire in Canada has remained low — reaching a high of 1,675 in 2008 (for immigrants older than 49), then dipping to 1,060 in 2011, and rising again in 2013 to an estimated 1,565.”

https://mobile.nytimes.com/2014/05/15/business/retirementspecial/the-trade-offs-of-relocating-north-to-canada.html

@Leo

you don’t have to immigrate to retire in Victoria. The biggest retiree group in Victoria outside of Canadians are Americans. The don’t need to give up US citizenship. Private medical insurance is the only thing that is needed. On our little street, there are 3 families from the US. Late 50s to early 70s. Surprisingly, all from SoCal.

@LEO “All due to the weather?”

I’d say! I went to university in Halifax. Winter there can be brutal, moreso than Calgary! The last two winters they’ve had to tunnel out, let alone dig out! My daughter sent me pictures. You can’t descibe the feeling after you clear your driveway only to have a plow come down the street and barricade you in again!

I highly doubt a lot of retirees from other countries come here. Immigration rules are stacked against them for one https://www.economist.com/news/americas/21638191-canada-used-prize-immigrants-who-would-make-good-citizens-now-people-job-offers-have

My friend sent this link, outdated, but this is what the rest of the world sees:

http://www.livingabroadincanada.com/2009/07/22/top-10-places-to-retire-in-canada/

I do not. Although this may be in the stats somewhere if someone wants to dig.

Possibly, however this is mostly because we have an elderly population. Those people are net sellers and it doesn’t matter how much money they have (aside from perhaps making the argument that when they keel over their kids will use the proceeds to invest in housing).

Hmm.. Much like Halifax, except houses cost three times more here. All due to the weather?

You are right. For example, in feudal times all the land was owned by 10% of the people. It didn’t matter that the median income was two potatoes a fortnight, it mattered that the 10% could afford the land.

Same goes today. Price to income is completely meaningless unless there is a high ownership rate and one can reasonably say that the median income is also close to the income of the median home buyer.

In Victoria the home ownership rate is somewhere around 70%. In New York it is 50%. Given their income distribution that means even the poorest home owner has an income of about $50,000 and the median is likely closer to $100,000.

One wonders why the even more stable world of government employees in Ottawa only managed to bring the house price up to $415,467 (and that’s after recent increases)

It doesn’t even have to disappear. A bad year of house values and a steep drop in assessment will discourage most from trying to dip into equity to buy another house. Recency bias and loss aversion hit hard.

Wow! This preoccupation of Victoria’s impending market implosion reminds me of Mark Twain’s famous refrain “the announcement of my death has been greatly exaggerated!”

As some have referenced, Victorias market has much uniqueness to it. LEO by any chance do you know what % of Victorians own their homes outright? I’m sure it’s well above the national average. Secondly Victoria probably has the highest individual net average asset wealth in the country. Because you are the seat of Provincial Government, have a well established University and are Canada’s West coast naval port, all providing secure and well paying jobs, Victoria is very well insulated against any severe economic downturn. Much like Halifax on the East coast, it’s hard to imagine either city experiencing much of a housing correction inspite of any upcoming new OSFI regulations. For my money I’d still buy into Victoria anyday over Halifax as would most prairie dwellers. Besides, buying RE should be for the long term not short as in stocks, so who cares if there is a short term correction or pause.

If the mandate of the OSFI is to ensure bank stability, is it in their interest to crash the market and risk that stability? The new regs increase stability going forward in the long term, but in the short term could destabilize.

The charts are a big buggy so I can’t generate it for condos or the whole market, but here it is for SFH in the core:

Local Fool

August 14, 2017 at 6:40 pm

Again, they are not a regulatory body for the frickin housing market.

Never said they were. My comments about the housing market were my considerations, not a hypothesis of the discussions that OSFI is having with its stakeholders.<<<<<<<<<<<<<<<

Sorry, Local Fool, I was frustrated with a poster on Greaterfool.ca and did a copy and paste.

I enjoy reading your considerations, among others. Peace!! Lol

Never said they were. My comments about the housing market were my considerations, not a hypothesis of the discussions that OSFI is having with its stakeholders.

If they were concerned with the direction of the housing market, if anything, it may enhance the impetus for them making their contemplated changes to lower the risk to the financial system during a bust. I think they should, and I hope the provincial bodies follow suit. Next up in my perfect world…getting rid of CMHC.

Local Fool

August 14, 2017 at 4:33 pm

Well if you’re correct, that would represent a serious disruption.<<<<<<<<<<<<<<<<<

<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

http://www.osfi-bsif.gc.ca/Eng/Docs/B20_dft_let.pdf

Subject: Public Consultation – Revised Guideline B-20 Residential Mortgage Insurance

Underwriting Practices and Procedures

Hey Local Fool, unfortunately, I am right. Regardless of the “Public Consultation” they will be making CONSEQUENTIAL AMENDMENTS.

“Once the changes to Guideline B-20 are finalized, OSFI intends to make consequential amendments to Guideline B-21 – Residential Mortgage Insurance Underwriting Practices and Procedures.”

Again, they are not a regulatory body for the frickin housing market. They are in place to protect the banks interests. They want to ensure that the banks have proper systems in place to provide proper recourse when you default on your mortgage.

“The Office of the Superintendent of Financial Institutions (OSFI) is an independent agency of the Government of Canada, established in 1987 to contribute to the safety and soundness of the Canadian financial system. OSFI supervises and regulates federally registered banks and insurers, trust and loan companies, as well as private pension plans subject to federal oversight.”

Not to mention the GDP of NYC generally exceeds that of our entire country. Nothing in Canada comes close, no matter how cutely we like to think so. Toronto is more or less a mid-size regional city. Vancouver? Not even a little. Victoria? hahahaha.

Your numbers are subject to question, as well. According to the (US) National Association of Realtors, the average home price in the New York metro area is $455,500, which is still expensive relative to the national average. Certain areas will be higher, way higher in fact – but there’s good reason for it. That city has very high prices coupled with a large proportion of very high income earners and large scale economic diversification – none of the things that any region in Canada has. There’s another niggly factor you’re missing: commuting . Many people live in the surrounding region, including out of state. The subway system is really well developed and is designed to accommodate this type of thing. You could easily work in Manhattan and live in a nearby city.

This isn’t to say that NYC could not suffer a housing bubble – in fact if I recall correctly their luxury market in Manhattan has taken a beating as of late, as prices got a head of themselves. Don’t know if that was a “bubble” though. In any case as you can till, New York does not represent an area where local incomes have no relevance. Gravity prevails.

So how much more construction can we handle. Look at how China has taken construction to an extreme to prop up their middle class.

https://youtu.be/BcyYyyaPz84

Garden Suitor: “We’re not NYC by any stretch, but house prices don’t have to be pegged to income”

….. or maybe it does.

http://nypost.com/2016/03/12/new-york-city-is-the-capital-of-millionaires/

The number of our households with annual gross incomes of $200,000 or more hit nearly 247,000 in 2014, according to the Census Bureau.

New York City has the largest population of super-rich on the planet — 8,655 individuals, just over 12 percent of the nationwide total, each having at least $30 million in net assets, according to a recent Wealth-X study.

Median family income in NYC is ~$51k (2009-2012), with avg sale price $1.4mil (2013). We’re not NYC by any stretch, but house prices don’t have to be pegged to income.

https://project.wnyc.org/median-income-nabes/

http://www.nytimes.com/2013/01/20/realestate/what-is-middle-class-in-manhattan.html

Well if you’re correct, that would represent a serious disruption.

In that event, I think Victoria would have a degree of insulation to volatility that Vancouver and Toronto will not. Having said that, I don’t think a 30% + decline is off the table, but it just depends on so many things, that I have no idea.

I have more trouble with the “over the next few years, +/- 10% for Victoria”. Granted, I know it’s a guess perhaps better than mine, but I just don’t think that this mania has years worth of life left in it. Prices versus incomes here are just too out of wack.

At 10% more, if we’re entering into a cooling period, I don’t think that’s realistic. I would want to know what metrics would durably support that kind of growth. At 10% less, that would not bring prices back to nominal levels, i.e. in touch with the underlying economy at all. In other words, it might be just as well to say the market will remain ho-hum – which after what we’ve just seen…I don’t know.

Local Fool: “Regarding your opinion of upcoming OFSI regs as something that will precipitate a “crash”, what would you say about alt lenders and credit unions in that picture?”<<<<<<<<<<<

Personally, I think that OSFI is introducing horses out, barn door closed legislation but that is only in respect to homeowner mortgage lending. The application of this legislation will severely curtail lending in the major centres and have a very meaningful impact on mortgage renewals. Yes, this will exacerbate the crash in Toronto and hasten the other major markets demise.

OSFI isn’t interested in the boom or bust of the real estate market as long as the “financial system” (banks) are fine regardless of direction of that market.They are really making sure that the banks will be in a position to weather the upcoming storm.