Mid-June Sales up, Listings down

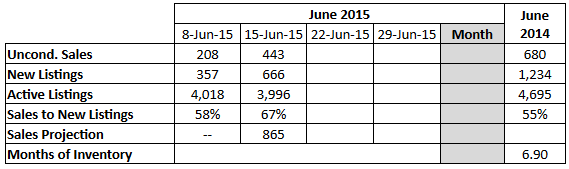

It seems that the Victoria real estate market definitely a sellers market this spring, with sales booming and active listings continuing to drop. Is it just those low interest rates that are continuing to stimulate the market? Are the current sales “pulling forward” future sales that may have occurred in the summer? Perhaps we’ll know when the monthly sales numbers are released in a couple of weeks and a few days. I’m still fine-tuning Leo’s Sales Projection formula, but the projection for June sales is about 25% more than last year.

I’m still fine-tuning Leo’s Sales Projection formula, but the projection for June sales is about 25% more than last year.

All of this talk brings back such memories for me. I just have to laugh about it now. All of the little people watching the markets as if their lives depended on it. Everybody wants to be right, prove how they’re right.

The funny thing is that if the government had not been artificially suppressing interest rates, had they never allowed amortizations to go from 25 to 40 years, had they not allowed no doc/cash backs/no money down or allowed home equity lines of credit to almost anyone, huge immigration numbers, turned a blind eye to corrupt Chinese money, none of this would be occurring. It’s so artificial, all of it.

And it could end tomorrow, and we would feel as if our world had ended. And all the people with two or three condos (hoping and dreaming for price appreciation) will be toast.

Look what the federal and provincial government (yes, I point my finger directly at them) has done to us. No one talks about much other than real estate, just like before the stock market crash of 1929.

It’s laughable really.

Your right. It hasn’t been 6 months yet.

These are the medians for detached homes in the core districts.

Month Sale Price, Median

Jan $542,500

Feb $597,500

Mar $625,000

Apr $631,200

May $620,000

Jun $635,000

I think you’re getting ahead of yourself Jack, when you say “That we have not experienced a substantial increase in prices given this strong sellers market in the last 6 months…”

We only very recently entered a sellers market. The large price increases are still on their way.

It’s not just the months of inventory. You have to know how quickly new listings are being added and how quickly inventory is being sold. Back in the early 2000’s we had the sewer and highway expansion that help create a massive amount of suitably zoned land for new home construction. A lot of that new home inventory wasn’t shown on the real estate board’s data listing service.

If prospective purchasers have the ability to increase what they can pay for a property then prices rise quickly in a sellers market. Something that any one looking to buy a home is immediately aware of when they are making an offer on a home.

That we have not experienced a substantial increase in prices given this strong sellers market in the last 6 months leads me to believe that most prospective buyers lack the financial means to increase their bids by a significant amount. We have a lot more restrictions on home equity loans today that puts a limit on prices if mom and pop are gifting some of the down payment from their home equity.

Prices could rise if Greater Victoria had the heightened level of speculation that I suspect certain parts of Vancouver and Toronto have, which is driving their prices higher and higher. These speculators are purchasing just to re-sell at a higher price where the physical composition or rental income of the property has no bearing on their offer.

Although, it’s possible we could have some speculation in some small niche markets.

What’s difficult to measure is demand. Unlike listings we can’t count how many households are actively searching for a home. However like a Black Hole in space we can see the effect on the surrounding to estimate the size of the Black Hole. That’s what the months of inventory, sales to new listings ratio and days-on-market attempt to do.

If the Western communities have a sellers market similar to the urban core they would also have similar demand. The size of the population of each area is less important to that of the size of the number of prospective buyers in each area. Depending on the economy, areas with a mature population may have less turn over of housing than neighborhoods of young people. Which could be reversed during a recession. Meaning that you may have two areas with the identical population but demand is stronger in one area.

I think a more compelling argument is the shift from starter homes in the core to condominiums. The availability of new condos provided an alternative to the older and small starter homes in these areas. The typical new 2-bedroom condo is most often similar in price to a pre 1960 2-bedroom starter house. In that way the different ratio of condos to houses in the areas may be muddling the comparison in demand between the two areas.

Maybe we should be accounting for prospective buyers that are equally willing to purchase either a strata home or a detached home? I don’t know how you would do that but it could be a reason why prices in the core are not increasing despite an obviously stronger demand than the Westshore.

Or not.

I’m not so sure I agree with your “strong stomach” conclusion. China markets have tanked twice since 2000 (see below) with very little downward pressure on prices.

http://i.cubeupload.com/3TuVSg.png

I don’t believe it is possible for there to be a hot sellers market but no price rises. If the hot market continues prices will rise. If people were at a price ceiling due to affordability, then the market will quickly moderate again.

If you’re basing projections on Vancouver type rises, you best have a legitimate idea who is going to be pushing those prices higher. If the China financial markets tank as many experts are forecasting, you best have a strong stomach if you’re maxed out in real estate and HELOC debt.

“It smells like a bubble, it looks like a bubble, and it walks like a bubble,” Morilla-Giner said in an interview on Bloomberg Television in London. “Steer clear, that is the trade.”

http://www.bloomberg.com/news/articles/2015-06-16/china-bubble-debate-turns-to-when-not-if-stocks-will-tumble

..and the Benchmark house was up 1.2% for the month of May, and 4.4% over the entire past year, so prices are starting to move.

http://i.cubeupload.com/izXV6r.png

I’m expecting a more explosive price move (something like late ’02) to start later this year.

Even as MOI fell off cliff in early ‘01, same as it did recently, prices didn’t go ballistic ’til later ‘02.

http://2.bp.blogspot.com/-GJ97IvxxcT0/UIJUAHbjJqI/AAAAAAAAAps/B4Gx8DcduqE/s1600/moibottom.png

Are prices going up or not?

A townhouse in Vic West just re-sold at $214,900. Previously purchased March 2013 at $205,000

A prestigious townhouse in Cordova Bay sold July 2005 at $685,000 and just resold at $687,500

A waterfront home in South Oak Bay previously purchased August 2013 at 2.2 million. Just re-sold for $2,282,000

Town home along Nursery Hill. Bought April 2012 at $285,000 plus GST, Re-sold for $290,000

Goldstream Avenue condo bought April 2006 at $252,000. Re-sold at $218,000

Condo along Manchester road bought April 2013 at $166,000. Re-sold at $175,000

With the low supply and strong demand for the last 6 months prices should be going up substantially. Like they did in the early 2000’s when we had a similar shortage of listings and strong demand. ????????

The market is like a drink in a vending machine.

https://youtu.be/sXd2XLTiaW8

The population of the core areas including Vic Saanich OB and Esq was 223,993 in 2011. The pop of Langford and the Westshore was approx. 74 0000. At 1/3 the population and the same or greater number of houses available for sale you have way less competition for homes.

It’s called The Great Facade. Keep the masses borrowing so bank profits keep shareholders happy. When one third of mortgage holders say they would be up shit creek with only a 1% hike then we have major problems ahead. I wouldn’t buy the hype from the perma-bulls prancing up the yellow brick road, they must be in the real estate bizz.

“However, the survey also found that more than a third of homeowners polled would face financial hardship if their mortgage payments increased by just 10 per cent.”

http://business.financialpost.com/personal-finance/mortgages-real-estate/a-third-of-canadians-would-struggle-if-mortgage-rate-grew-by-only-1-survey-finds

@Just Jack

I would try using this site: http://pressbin.com/tools/excel_to_html_table/index.html

I tried to cut and paste out of my spread sheet. Same with some of the graphs I wanted to display. Where should I look for information on how to improve my presentation of data?

Although it takes some time, WordPress does support HTML tables in comments – so something like …

<table>

<tr><th>Year</th><th>Median Condo</th></tr>

<tr><td>2005</td><td>$207,251</td></tr>

<tr><td>2006</td><td>$249,500</td></tr>

<tr><td>2007</td><td>$253,900</td></tr>

<tr><td>2008</td><td>$299,900</td></tr>

<tr><td>2009</td><td>$280,000</td></tr>

<tr><td>2010</td><td>$295,000</td></tr>

<tr><td>2011</td><td>$295,000</td></tr>

<tr><td>2012</td><td>$265,000</td></tr>

<tr><td>2013</td><td>$295,000</td></tr>

<tr><td>2014</td><td>$272,900</td></tr>

<tr><td>2015</td><td>$285,500</td></tr>

</table>

… displays as:

I’m okay with home owners weathering an increase in interest rates. They just have to cut back on cable or phone or put a sweater on in the winter. And besides the mortgages don’t all come up for renewal at the same time. If interest rates increased by 1 percent that would be spread out over the next five years of renewals.

The ones getting hit are those buying. They won’t qualify for the same jumbo sized mortgage as before. That’s a limiting factor on price appreciation and if we are at the inflection point of maximum mortgage payments, then prices have to come down or sales will drop and inventory will increase.

Market prices are determined through the actions of buyers and sellers. And only 3 to 4 percent of the total stock of housing is listed at any time. That 3 or 4% is the real estate market which sets market value. The 96 percent or so of remaining home owners are only in for the ride they have no effect on prices.

If you’re lucky to have your home up for sale in the city, you are in the driver seat. As it seems that the only thing holding back prices is the buyer’s inability to get more financing. Especially if your home is a dump. Chances are you’ll get multiple offers as opposed to when the market favors buyers and you won’t see any offer during the listing contract.

From the 2015 CAAMP report that LeoVictoria posted above, it looks like home owners are not only prepared for but are in great shape for any rate increases. Besides, 40 years of price behaviour show prices always soar as rates go up.

“The average down payment made by homebuyers in the survey: $119,000

Percentage who chose fixed-rate mortgages: 72%

On a 10-point scale of interest rate expectations, with 10 meaning they are expected to “go up drastically,” the score given by buyers for interest rates in the five years: 6.9 ”

Wow. If you can’t handle a 10% increase then the mortgage is too big to begin with!

How does this square with the constant reassurance from the banking industry about everyone being prudent with their money?

These are the May median prices for condos in the core starting in 2005 at $207,251 to May 2015 at $285,500. There hasn’t been much movement in price since May 2008 when the median was $299,900

$207,251 $249,500 $253,900 $299,900 $280,000 $295,000 $295,000 $265,000 $295,000 $272,900 $285,500

For the first few years it was good times speculating in condos. It could be a bad decision these days to speculate on condos by leaving it vacant and hope to sell at a higher price.

Although a lot of people in Victoria have chosen to buy one or two condos as rental investments. And the rents in a newer downtown condo building are very high high relative to an older downtown apartment building just a block, two or three away. I wonder if people are choosing the less expensive apartment over the newer condo? The savings could be a couple hundred to $500 a month. That’s a lot of whiskey and wild wild women.

https://youtu.be/hqk3osxS4wQ

I don’t know enough about the Toronto market.

My suspicion is that condos will drop first in a price correction. That restricts people’s ability to move up from a condo to a house or for those that own a couple of condos as investments to sell and move up to a better primary residence.

CBC News: Rate hike could leave mortgage holders stretched, survey finds

Nearly half said they couldn’t manage a 10 per cent increase in their mortgage payment. “Having your payments go up 10 per cent sounds like a lot, but if you have a $200,000 mortgage and interest rates go up one per cent, that’s a 10 per cent increase in your mortgage payments,” said Manulife Bank CEO Rick Lunny said. “So there’s not much room here for those people.”

Persons in the 45 to 54 year age range are the most likely to “move up” the property ladder. Back in 1990, they made up 9.98% of the population but in 2015, this has increased to 13.76% of the population.

The 25 to 34 year range are most likely to be first time buyers. Back in 1990, they made up 16.63% of the population, but in 2015 this has decreased to 13.71% of the population.

This change in demographics matches the property buying pattern that we are seeing.

Data Source: http://www.bcstats.gov.bc.ca/StatisticsBySubject/Demography/PopulationProjections.aspx

The number of homes for sale is about the same 585 to 550 in the two areas. It’s the demand that seems to have changed as the number of sales have increased substantially from this time last year in the urban core.

Most of the increase in core sales are homes priced in the $600,000 to $800,000 in Saanich and Victoria with a slight decrease in the volume of starter homes in areas like Esquimalt. That suggest that the increase in demand is centered in the middle to upper middle income range. Made up of people moving up the property ladder and people downsizing.

The economies of Vancouver and Victoria are quite dissimilar. I think we’re more similar to the economy of the Fraser Valley than the business hub of BC. And they are not seeing massive price increases like Vancouver either.

“Sales on the Fraser Valley Real Estate Board’s Multiple Listing Service (MLS) in May remained at strong levels – the highest since 2007 – however, they softened slightly compared to April.

There were 1,969 MLS sales processed in May, a decrease of two per cent compared to April, however an increase of 21 per cent compared to the 1,633 sales processed in May of last year.

In May, the total number of active listings on the MLS was 8,512, an increase of 1.5 per cent compared to April and a decrease of 14 per cent compared to May 2014. The volume of new listings decreased seven per cent compared to April, and was also down seven per cent compared to May of last year.

In May, the MLS Home Price Index benchmark price of a detached home was $603,100, an increase of 6.5 per cent compared to May 2014 when it was $595,600. (MY NOTE 1.2% not 6.5%)

The benchmark price of townhouses in May was $303,100, an increase of two per cent compared to $297,300 in May 2014. The benchmark price of apartments decreased year-over-year by 2.8 per cent, going from $198,100 in May 2014, to $192,500 last month.”

On the mobility from apt to SFH, if memory serves apt’s have been outperforming houses in Victoria for quite some time now…but I will check the stats.

Price increases always lag. IMHO I believe we’re about to see a Vancouver-like price increase. Maybe not 16% like they did last year, but likely double digits. There’s so much pressure building in Victoria on all fronts. For example our vacancy rate has now fallen to 1.2% from 2.7% last year, and is now even lower than Vancouver. Prices in Vic and Van used to be near each other, but the gap has become enormous at 0.6 to 1.4 million. I believe Victoria now starts to close that gap.

http://www.andrewcmacdonald.com/wp-content/uploads/2011/03/long-term-real-estate-formula.jpg

There is just more available in the western communities than the core. The lack of product along with low rates is contributing to the competitive market in Victoria imo. My friends just sold their place in Oak Bay. It was on the market for a short period of time and they had multiple offers and offers of backup offers once they had accepted an offer. I’m still considering selling but the whole process is such a PITA – I probably won’t get to it this year. Inertia probably keeps a large number of people with rental properties from selling even when a market shifts to a sellers market.

JJ, is this the precursor for lower prices?

The mobility from moving from an apartment to SFH is going to get HARDER IMO.

Toronto condo vacancies surge to all-time high

The Globe and Mail

Published Wednesday, Jun. 10, 2015 12:59PM EDT

There’s a glut of empty condos in Toronto. The number of vacant completed condos in the city soared to an all-time high in May, National Bank Financial said Tuesday in a note, citing data from Canada Mortgage and Housing Corp. The number of vacancies hit 2,837 in May, up from 2,038 a month earlier, as the absorption rate – the percentage of condos completed during the month either sold or rented – fell to 69.5 per cent. “It would be premature to think that the absorption rate will stay low, causing persisting accelerated increases in the number of vacant completed condos,” National Bank Financial said.

With less than 575 houses for sale and close to 300 selling in the last 30 days it isn’t possible to be a buyer and a vulture in this market. New listings are just keeping up with sales at a ratio of 340 to 300. With half the homes selling under 22 days. Being a prospective buyer in this market makes you more prey than predator.

But even with this tremendous pressure on the market place over the last 5 months, median prices have remained unchanged at $625,000. Why are median prices not rising in the double digits then?

Maybe because once you get pass the grid locked streets of the inner core and head into the Western Communities and Saanich Peninsula market activity tapers off quickly. The Western Communities have about the same number of houses for sale of around 550. But far fewer sales of around 140. With 210 new listings added in the last month. Prices have also been stable for the last several months at around $465,000.

Similarly for condos in the core, there just isn’t the panic to buy.

The hot market is concentrated in one class of property in one small geographic area.

So why such desperation to buy a house in the inner core lately but not elsewhere or condos?

Is this the last kick at the can?

CAAMP spring report http://www.canadianmortgagetrends.com/canadian_mortgage_trends/2015/06/caamps-spring-mortgage-report-2015.html

@nan

Thanks for your insightful comment in the previous post. I don’t agree with everything, but you raise some good points. I think that it is very likely that in my lifetime, money will never be cheaper to borrow that it is now.

I’m not looking to “enter” the market, but instead looking to “move up” on my own terms and time frame. My strategy is to continue to save my money, meaning that if I want to move in few years – I’ll have a lot more money to put towards a nicer house. Mind you, banks don’t make it easy to be a saver … at least the markets have been rewarding for the past five years. 😉

I wouldn’t go so far as to say I’m bullish, just not bearish. no one was really looking at the cmhc in the media as a cause of the run up last time until 2006. By then it was too late! The cmhc is relatively tight now but there are plenty of new loosenesses and new sources of demand out there now.

Maybe we’ll crash nationwide, maybe we won’t but either way, victoria is relatively cheap, money is cheap and people are buying so prices are going up. In my opinion, it’s a decent time to buy.

Well said nan! (previous thread)

Finally another bullish view… I was getting lonely 😉

Thanks for the sales projection table. I liked that on version 1.0.