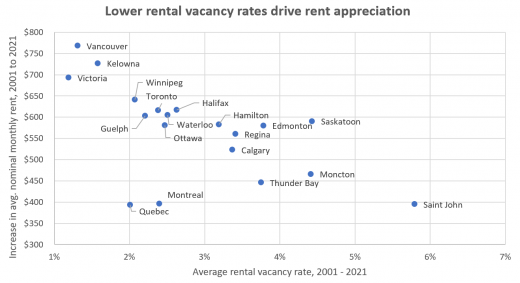

Rental reprieve over: vacancy rate returns to 1%

This post is 2 years old. The data and my views may have since evolved.Back when the pandemic first hit I wrote an article saying the rental market – which at the time had a...

This post is 2 years old. The data and my views may have since evolved.Back when the pandemic first hit I wrote an article saying the rental market – which at the time had a...

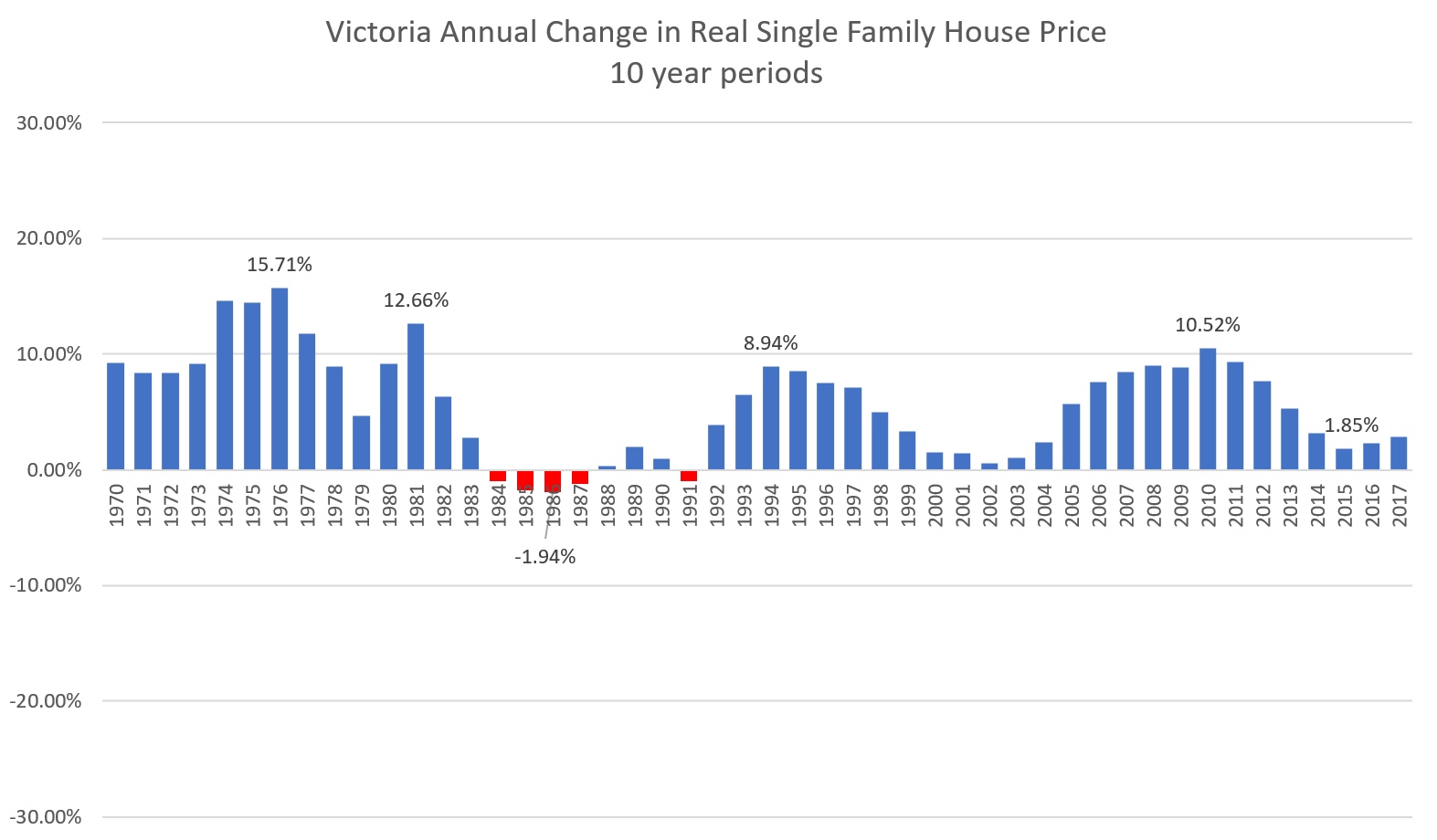

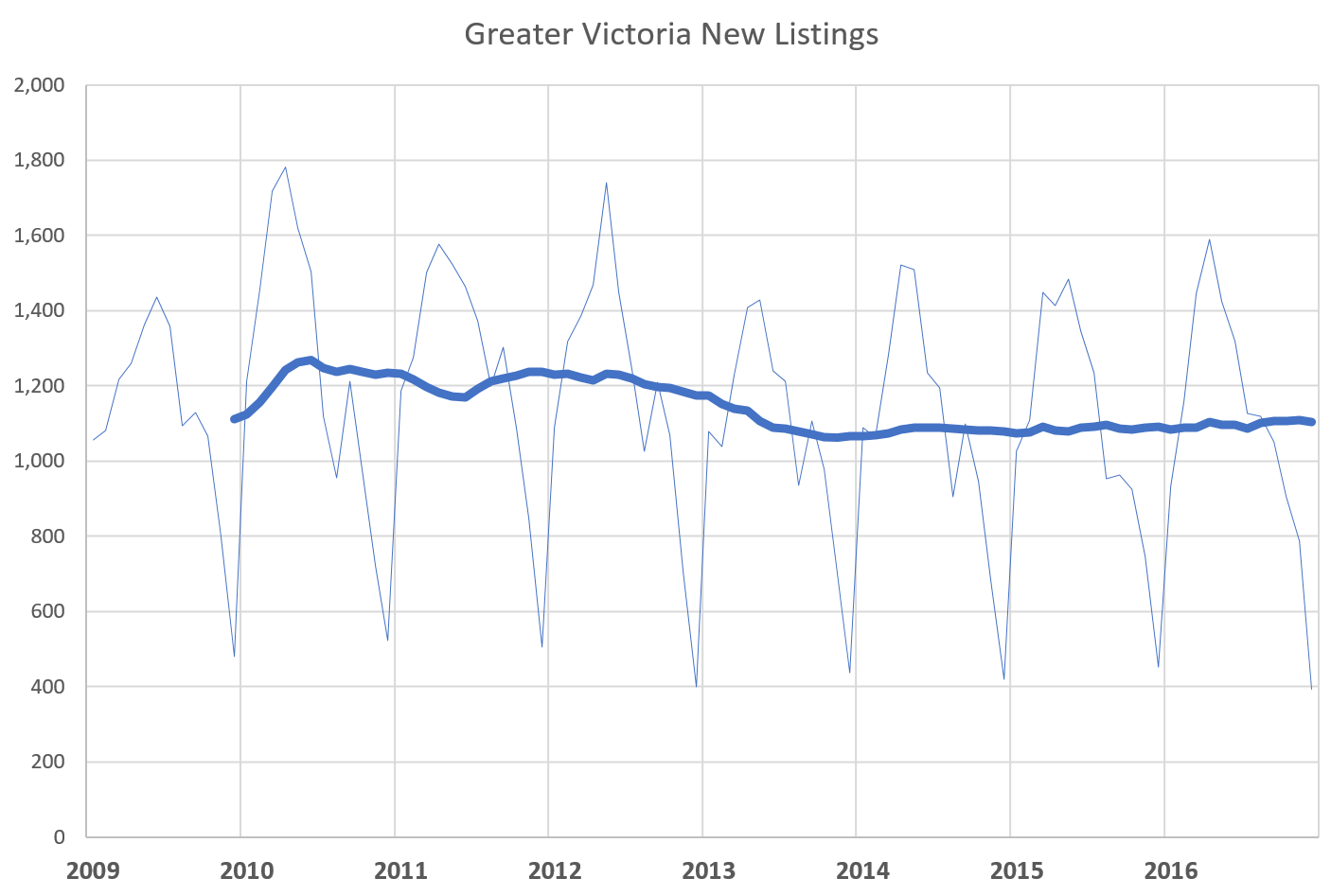

This post is 7 years old. The data and my views may have since evolved.Generally real estate is a slow moving beast. There are no flash crashes here, and without an external stimulus, there...

This post is 7 years old. The data and my views may have since evolved.Weekly stats update courtesy of the VREB. January 2017 Jan 2016 Wk 1 Wk 2 Wk 3 Wk 4 Unconditional Sales 65...

This post is 8 years old. The data and my views may have since evolved.First of the month monday market update courtesy of Marko Juras. December 2015 Dec 2014 Wk 1 Wk 2 Wk 3 Wk 4...

This post is 8 years old. The data and my views may have since evolved.November numbers are out, and it’s pretty much as expected. The trend of an improving market continues unabated, with both MOI...

This post is 8 years old. The data and my views may have since evolved.Monthly data will be out tomorrow, but here’s a sneak peak with only one day missing thanks to Marko. November 2015 Nov...

This post is 8 years old. The data and my views may have since evolved.If we lived in a world where free market forces set prices we might expect a buyer with a larger down...

This post is 8 years old. The data and my views may have since evolved.Another month another increase year over year strengthening of the market. In fact the president of the VREB reports that “This is...

This post is 8 years old. The data and my views may have since evolved.Thanks to Marko for providing the numbers. October 2015 Oct 2014 Wk 1 Wk 2 Wk 3 Wk 4 Unconditional Sales 268...

This post is 9 years old. The data and my views may have since evolved.Well my tables aren’t as nice as David’s, but it’s time for a Monday update. Thanks to Marko as usual for providing...