Nov 6 Market Update

Weekly sales numbers courtesy of the VREB.

| Nov 2017 |

Nov

2016

|

||||

|---|---|---|---|---|---|

| Wk 1 | Wk 2 | Wk 3 | Wk 4 | ||

| Unconditional Sales | 83 | 599 | |||

| New Listings | 157 | 786 | |||

| Active Listings | 1909 | 1815 | |||

| Sales to New Listings | 53% | 76% | |||

| Sales Projection | — | ||||

| Months of Inventory | 3.0 | ||||

20% below last year’s daily sales rate but that doesn’t mean much since we only had the tail end of last week in this week’s numbers. Will require another week or two to determine whether the stress test is pulling buyers forward, or whether the increasing number of lenders that are already applying it will start to put a damper on sales.

This is the season when sellers start giving up when their listings expire. We dropped 77 listings at the end of October and only a couple came back. While we will likely stay above the year ago inventory levels for quite some time, the market will still shed at least 100 more listings through December.

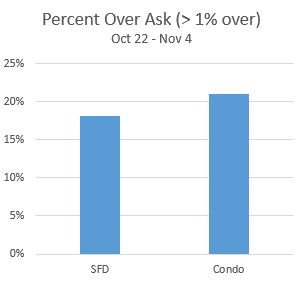

The over asks have definitely cooled down, with 18% of single family going over, and 21% of condos. In the spring we had up to a third of properties going over list price. The lowball of the month award goes to a house that sold for almost $600,000 under the original asking price and $500,000 under assessment.

Reader Barrister brought up the point that the days on market numbers are often distorted due to properties being relisted multiple times. “House down the street was on the market for over two years and every time they changed agents it came out as a new listing. When it finally sold it was recorded as 11 days on market instead of over 700 days. In short, the MLS stats as to days on market are next to meaningless.”

Which raises the question: How should days on market be defined? If a listings is cancelled and relisted or sellers change agents it makes sense to keep the days on market counting up. But what if it there’s an offer that collapses and 2 months later the property is back on? What if a seller tries to sell their house every spring for 3 years? Same property, but perhaps one could argue that the market is now different, so DOM should be reset there. Thoughts?

New post: https://househuntvictoria.ca/2017/11/10/dark-sales/

One of the issues is separating out the actual property from the season. While I believe that places tend to sell for lower on a price/ask ratio in the fall/winter, that is likely more to do with them being places that are less desirable (left over from spring) than the season.

Could maybe be done for condos that are more uniform.

Leo, I have an idea for a future post: you analyze and rank the four seasons in terms of when it’s most advantageous for sellers to sell.

LOL. Here’s an interesting tactic:

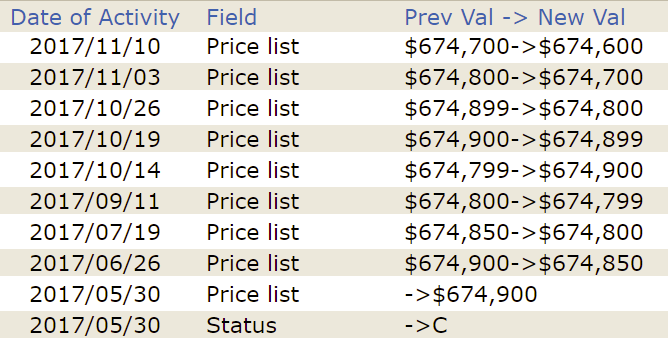

8 price changes of $50-$100. Granted for a development so they try to keep it fresh over time but still ridiculous.

The foreclosure that I’ve been watching finally received an offer after 203 days on the market. I might just watch this one at the court house as someone just might be getting one of those special deals by finding the right property at the right time. It ain’t pretty and it needs lots of cash to repair but that’s why someone might make some good coin.

That’s it. If you happen to be ready and the market conditions favour what you’re selling and buying you can profit. You could also recognize that it is currently happening and jump on the opportunity if you were going to upgrade anyway. But waiting for such an opportunity is unlikely to be successful.

Entomologist, the leaky condominiums in the 1990’s were one of those good times to be an investor with lots of cash. When you could buy newer condos in Victoria for $25,000 and $50,000 cash and rent them at $900 a month. The banks wouldn’t lend a dime on these properties and that meant few people could buy them and the prices tanked. Just a fantastic rate of return. And after remediation the prices went back up to a quarter of a million each.

Most of the time the remediation costs were paid by the banks too.

In my experience, these theoretical arbitrage opportunities never happen in the real world. You’d have to be 100% focused on trading for profit, rather than actually looking for a place to live. You get lucky with this sort of timing, unlucky, or it’s a wash. Doing it by design, I’d say forget it unless you know the risks, you have cash in hand, and the place you want to sell is already vacant (in which case you don’t need advice from internet blogs).

It takes most people months of getting to know the market, going to open houses, and going to property showings before they’re ready to make an offer on an appealing property. It takes even longer to decide to sell if you’re already living in an owned place. And moving takes days to weeks (to months), unless you hire pro movers. Then all it takes is thousands of $$. And are you going to buy first or sell first? Condition of sale? Condition of finance? You’re going to pay more.

The idea that you can analyze the market, decide when to strike (buy), and the place you finally decide is worth your hundreds of k’s comes up for sale immediately and you jump on it (and get an accepted offer), and immediately turn around and sell your existing property as some sort of designed strategy that you can profit from in, all within a single market, is fantasy.

Of course it happens all the time between markets, though – buy quickly (overpriced) in a cheap market, say in the maritimes, and sell quickly (underpriced) here. But that’s not the same thing.

Very little in the majority of cases. There is some (small and theoretical) opportunity for arbitrage if you are buying and selling in types of properties that are experiencing a temporary disconnect in price changes. For example, last year single family house prices jumped several months before condos. There were a few months where you could have sold a SFH after the runup and bought a condo and profited from the gap. Alternately it would have been a particularly bad time to upgrade from a condo to a SFH. That gap has now corrected itself.

Similar things can happen in core vs houses in the periphery or houses at different price bands for temporary periods.

Barrister also makes a good point. Another thing to consider is the very high transaction costs involved in selling and buying real estate. You might consider if it were not cheaper to renovate your $600,000 house into an $800,000 house (obviously doesn’t solve the location!), because selling a $600,000 house and buying an $800,000 house may very well cost you $38,000 in fees, taxes, and commissions.

Great answers thanks!

So essentially, provided that you have enough equity or cash to prevent being underwater on the more expensive place (perhaps underwater isn’t the right term, perhaps keeping yourself from being a high risk borrower at renewal is more accurate), and provided you can handle the payment if interest rates go up to 5-6% from a cash flow perspective (i.e. stress testing yourself), and provided you don’t lose your job or catch barrister banging your wife… if all those boxes are check then its more or less a wash.

Makes sense. Makes me feel better about perhaps not waiting if the right place shows up on the market (which is a big IF with our inventory issues as Local Fool points out).

swch25:

That is a good question which deserves a better answer than I can provide. But let me give at least a bit of a shot at it.

First, you logic is correct if you are buying with cash. Where the logic is different is when you are dealing with a mortgage. Lets assume that you sell for 600k and then buy for 800k. (I am too lazy to work out all of the math here so I am just tossing out general numbers. Lets assume that you have about 160k equity in the 600k house. The market goes down 20% and you lose 120k of equity or roughly 3/4 of your equity. At the end of the day you are still worth 40k.

Now let us look at the other scenario. You have sold your house and put your 160 of equity into your new house bought at 800k. The market drops the same 20%. Your equity is now zero; zilch; nothing.

That is the main difference along with the fact that you now own the bank a lot more money.

You sort of suggest that this is not important since you will just keep paying the mortgage for the next 25 years. The main problem in my mind comes up at mortgage renewal time. Assuming that you dont have a big piggy bank of cash sitting around the bank may well decide not to renew your mortgage. Once there is no equity in the house the bank might simply decide that they want to get their money out of the house rather than take the risk that the housing market is not going to go down further. But lets say you have a very nice and kind bank manager (played by Jimmy Steward) who agrees to renew your mortgage but they will consider you a very high risk loan and might easily double your interest rate. The fact of the matter is that you cant go to any other bank since you have zero equity and they will not even talk to you. Time to put the dog down because you are about to be eating his supply of dog food.

The second scenario, using the same example as above, is what happens if you have to suddenly sell you house. You or your spouse lose their jobs or one of you is transferred to Winnipeg or your wife finally decides to run off with me and divorces you. Bear in mind the divorce rate is over 40% and this is a real risk (the world is full of people that never saw it coming). Suddenly the difference between having 40k of equity and having nothing becomes rather critical.

The last scenario is the more probable one where interest rates push up to 5 or 6%. You might be able to afford the increase with the 600k house but the larger mortgage on the 800k house might just be a bridge too far.

I might well be wrong about this and there are better minds out there but I just thought I would throw out a few thoughts.

If you’re selling your house for a ludicrous price, and buying one at same, then I don’t really think it makes as much difference. If you can afford the payments at roughly 6%, then most everything else in the market is just noise.

A true “bagholder” in this market is (IMO) probably going to be someone who has bought recently for the purposes of speculation, or an end-user that has recently overbought.

You’re fine – though a consideration atm is a lack of selection, so you may wish to wait until that changes, and perhaps wait and see what effect the OSFI stress tests have on the market.

Question for you all RE: market timing. How much does it actually matter if you’re both buying and selling into the victoria market? I figure if you sell a place for 600-800k and buy a place for 700-900k, that you’re not at a whole lot of risk of holding the bag. Is that flawed logic?

Even if the market drops 20%… you’d lose 20% of your sale value (so say 140k of a 700k house), and you’d lose 20% of what you spent on a new place (say 180k of a 900k house). You’re only really out $40k, which over 25 years isn’t that worrisome.

Where am i wrong? please help!

How will you recognize falling RE prices??

Perhaps the first sign will be as LeoS said:

“I see a growing number of places that were bought earlier in the year, renovated, and now sitting for ages. Seems the days of the easy flip are over.”

We are past the peak!!

Good news: CMHC collecting more housing data

“Data gaps exist in three key areas: housing finance, needs and markets

In the housing finance area, we are looking to collect more information on the entire mortgage sector, whether insured by CMHC or not. To obtain this information, we recently accessed a dataset from a credit reporting company that covers 85% of the total mortgage and credit universe.”

https://www.cmhc-schl.gc.ca/en/hoficlincl/observer/observer_206.cfm?obssource=observer-en&obsmedium=email&obscampaign=obs-20171110-mou

Yeah the common relist to appear fresh. What I don’t get the logic behind is relisting at a higher price when it doesn’t sell. What is the theory here? That buyers will suddenly panic seeing the same places being relisted for more?

I still see places reselling now for higher than a year ago, but I see a growing number of places that were bought earlier in the year, renovated, and now sitting for ages. Seems the days of the easy flip are over.

We are currently looking for a house and I must say I am seeing a fair amount of PC’s within the core. It’s also interesting to see, as someone else noted that people relist their same house with the PC as a new listing. I see 3125 Somerset St took off $100k and it now shows up as a new listing.

I made the mistake of looking at some listings this morning. They are asking almost 2 mil for a row house on St. on ST. Charles. Listings for tiny houses in Fernwood are going for well over eight. There is something not right here.

I am not co,paring it with prices of twenty or even ten years ago but with what things were selling for in 2013.

I have to agree with Barrister the prices compared to 2013/14 are seems quite high. We moved back to Victoria in 2013. We have been looking recently in either Fairfield / Oak Bay / Camosun but also west side of Cordova Bay (not ocean side) and Broadmead. It still blows me away at the prices compared to the flat lined prices of the years prior especially out in Broadmead and Camosun that were 20/30% less even last summer (2016). I have started to notice a few houses that were purchased in the summer of 2016 being recently resold (last 2 months), there also seems to be others who purchased last year and listing for quite high prices just hoping to resell it seems. I dont know how common that was in the past 2 years as I was not watching the market then

I’m hoping that we are starting to see a decline, from what I see on filters there are certainly PC’s going on but also over asking on some areas. I’m hoping to see what happens into the next month or 2 and then possibly the new year when mortgage rates change and NDP’s “comprehensive” strategy… whatever that will be.

lol.

Just looky loo. The tevent is on until 8:00; cant imagine buying there though.

How much longer do the burgers go for? I could be buy-curious if there is free food involved.

Barrister are you contemplating purchasing or was this just looky-loo?

My same thought, Once and Future.

Went to the open house at the Bayview over in Songhees. On the positive side you can get so really good free hamburgers; on the negative side they wont give you anything in the way of hard information including actual prices or any showcases of kitchens, fixtures or flooring. But do drop by for a good burger just dont expect any straight talk about what you might be buying.

Re: Commissions

Leo, thanks.

So commissions need to be determined in each case, with the possibility of some haggling.

Thanks very much for this, Leo S. Interesting indeed.

I am generally sympathetic to the message he is trying to convey, but this article is so full of goofy statements that it really hurts his message. Just one of many:

I don’t know where he is from, but things don’t work like that in Canada.

I made the mistake of looking at some listings this morning. They are asking almost 2 mil for a row house on St. on ST. Charles. Listings for tiny houses in Fernwood are going for well over eight. There is something not right here.

I am not co,paring it with prices of twenty or even ten years ago but with what things were selling for in 2013.

Makes sense. Sharks like ice cream flesh sandwiches 🙂

I had to look up the word “trenchant”. I have never heard it before. Anyways, I’m dripping with feverish anticipation. Is it this one?

You are in for a treat, Local.

It’s a trenchant, empirical, and perspicacious tool which shows where we are, right now.

Galbraith and Keynes would be envious.

Which chart does he mean, Hawk?

Don’t make me do it Jerry. 😉

Sounds like a shit-ton of work for $5k.

“The case of Ferland v. Groenwegen, illustrates the value of incorporating the representations in a PDS into the contract. A rural property contained two wells. When the buyer first viewed the property, she asked the seller whether there was enough water. The seller answered there had been no problem “since the new well”. In the PDS, the sellers advised that they were not aware of any problems with the quality or quantity of well water.

The contract of purchase and sale contained wording that made the PDS part of the contract. A licensee wrote the contract and we can reasonably assume that the contract contained language similar to the wording in Clause 18, described above.

After the buyers purchased the property, they experienced water shortages. When the buyer contacted the sellers about the problem, the sellers said they had experienced similar difficulties when they lived on the property. The sellers maintained; however, that they completed the PDS in good faith without any intent to mislead. The sellers genuinely believed that these difficulties did not constitute a water quantity problem. Ultimately, the buyers fixed the problem by installing a new well for approximately $7,295. The buyers sued the sellers for damages in Small Claims Court to recover the cost of the new well. Although the Small Claims Court dismissed the buyers’ claim, the Saskatchewan Court of Queens Bench reversed that decision on appeal.

The appellate court found that the property had an unusual water system that suffered from water quantity problems from time to time. When the sellers completed the PDS, they never mentioned the unusual nature of the water system. Instead, the PDS gave the buyers the impression there were no water problems. Since water quantity was important to the buyers, they relied on the information in the PDS. The appellate court believed the sellers’ assertion that they never intended to mislead the buyers. Nevertheless, the answers in the PDS were misleading. Standing alone, the information in the PDS amounted to an innocent misrepre- sentation. The doctrine of merger prohibits a claim for misrepresentation after completion unless it amounts to error in substantialibus, which would likely not apply in this situation.

In this case, however, the court found, in effect, that by incorporating the PDS into the contract, the statements in the PDS became warranties under the contract. Despite the sellers’ good intentions, their infor- mation was incorrect. In the circumstances, there was a breach of warranty and the doctrine of merger did not apply. The court awarded $5,000 in damages to the buyers, representing the maximum monetary award in Small Claims Court in Saskatchewan.

In summary, the doctrine of merger tells a buyer, “Do your homework, and if you intend to rely on any assurances, put them in writing in the standard contract, because if you don’t, you will not be able to sue the seller after the deal completes, except in special circumstances.” A buyer can avoid the consequences of merger by inserting a warranty in the standard contract, in which case clause 18 stipulates that the warranty will survive completion. Alternatively, the buyer can avoid merger if he or she can prove the existence of a collateral warranty that the parties intended to survive completion.

Of these alternatives, an express, written warranty in the standard contract is clearly better because it is much easier to prove. A licensee representing a buyer best protects his or her client by ensuring that every assurance upon which the buyer intends to rely is warranted, in writing, in the standard form contract.”

It’s a bit more complicated. There are two kinds of conditions the buyer could put into their offer:

So what’s the importance of including the PDS itself as part of the contract rather than just saying the buyer must approve it? Well here is what the Real Estate Trading Services – Licensing Course Manual has to say about that:

“By making a PDS part of the standard contract, the buyer can treat the statements in the PDS as warranties, the breach of which enables the buyer to disregard the doctrine of merger and sue for damages. If the PDS is not part of the contract, the buyer cannot sue the seller for inaccuracies in the PDS unless the buyer can fit the claim within one of the exceptions to merger, such as fraud, or a mistake or an innocent misrepresentation that amounts to error in substantialibus, or a warranty collateral to the main contract.”

In other words, it is in a buyer’s interest to include the PDS in the contract, and it is not in a seller’s interest to do so*.

*as always, consult your own lawyer for advice on your own situation.

This is all getting very abstract. If Hawk would just post the graph everything would be clarified.

Seems like I need to rebut this chart in detail in a future post since it keeps getting brought up.

The real estate industry gets very antsy and particular about fees. They go to great lengths to say that you cannot imply there is a standard fee when talking about fees, or imply that fees are the same between agents. So here is your standard disclaimer: FEES MAY VARY.

The reality is that the vast majority of sales are advertised as offering 3% on the first $100k and 1.5% on the balance for the cooperating brokerage (read: buyer’s agent). Usually that also means the same for the sellers agent. So that means total commission the seller pays is 6% on the first $100,000 and 3% on the balance.

I don’t see any differences between lower and higher priced properties there. A several million dollar house will be advertised at 3%/1.5% same as a $250,000 condo.

Of course there are other commissions being offered. Occasionally one sees a flat 1.5%. Sometimes a flat 2%, sometimes a set dollar amount, sometimes 0.5%, sometimes 3.5%/1.5%. But those are in the minority.

Very true. The “increasing sales” mantra should be expected with increasing population. I used to have some graphs that were population adjusted that showed this.

UBCM endorses Victoria’s resolution to tax empty homes

A vacancy tax could be in the works for Victoria, requiring absentee property owners to pay for leaving their homes empty.

The Union of B.C. Municipalities passed a motion, lead by the City of Victoria, to ask the province to give municipalities the option to impose a vacancy tax similar to Vancouver’s Empty Home Tax that rolled out last November.

Coun. Ben Isitt, who put the motion forward with Coun. Jeremy Loveday, said he appreciated the support of local governments from across B.C. to demand the province take action against real estate speculation and commodity investment interfering with local housing supply.

http://www.vicnews.com/news/ubcm-endorses-victorias-resolution-to-tax-empty-homes/

Mike’s chart is two years old. Look at the new data via Steve Saretsky. These are facts that historically lead to credit crunches in the past. Canada hasn’t lead the pack since early 90’s.

Canada Accumulating Private Debt Faster Than Any Advanced Economy

“In the past 5 years, Canada has accumulated more debt than any other advanced economy. Private sector debt to GDP has surged 20% in this time.

There’s plenty of research which suggests the tipping point for private sector debt appears when the debt to GDP ratio grows by 17% in five years. Which we surpassed in early 2016.”

http://vancitycondoguide.com/canada-accumulating-private-debt/

Just saying…not everyone is irresponsible using HELOCS, we’ve used them for 20 years. Used properly, they’re a great tool to get ahead. Keeping in mind of course, it’s for business use only! No toys allowed!

@ Michael.

Look again at your chart. Notice the sharp increase and sudden, subsequent drop offs in Ireland, Spain, Denmark and the US? Every time they start spiking upwards, they eventually come crashing down – the magnitude of the latter is dictated by the degree of the former. Those guys had their mean reversion in their housing markets.

Your rebuttal just, in part, demonstrated my points.

Canada, Australia, New Zealand are all countries that borrowed their way out of 2008, and are all now simultaneously making global headlines for their precarious housing markets. These countries aren’t going to escape the inevitable, no matter how earnestly you attempt to disregard or explain away the reality that is unfolding.

Considering Greater Vancouver is 8 to 10 times the size of Greater Victoria that may be significant.

Fair enough Ento but the US has not been taking out HELOC’s at the psychotic rate Canadians have. Many HELOC lenders in the US are still shut down from 2008.

This is the massive bomb that will bring down the house of cards in the coming months as the buyers get squeezed out by the credit lenders.

Imagine if the averages and medians drop another $40K next month or even by Christmas ? Look out below.

Rising interest rates could spell trouble for home equity loans

The wildly popular line of credit makes it easy to pay only interest while piling up debt

http://www.cbc.ca/news/business/intetest-rate-home-equity-line-of-credit-1.4281279

I’m not saying I completely buy the ‘healthcare’ comparison (like Ento said it’s “hard to compare”).

Another way of seeing that the US actually looks to be the outlier, and Canada the norm, is here:

Healthcare costs are higher in the states but most of those costs are paid by employers or the government. And if you’ve ever lived in the states you know that damn near everything else is a LOT less expensive than Canada.

Hawk –

True, but US has no capital gains exemption for primary residences. They also have 30 yr mortgages. It’s always been hard to compare Canada vs. the US in terms of housing affordability.

Keep spinning your fantasy Mike. You’ll flog those presales one way or another. We don’t have mortgage interest deductions that the US has. 67% difference is not made up with healthcare costs. RBC snd CMHC thinks otherwise with red flags everywhere.

Once you factor in healthcare costs, US & Canada have similar affordability.

https://www.theinvestorspodcast.com/blog/the-shocking-truth-about-government-debt/

Healthcare is essential, and no matter what, people will make it their number one spending priority; because we all know if you don’t have your health, everything else becomes extremely difficult. This means discretionary spending goes out the window when you see premiums rising. Then there is less money to spend on food, clothes, and even housing.

You know that Canadian housing bubble that looks so absurd against US home prices? Well, it seems that Canadians have more to spend at the end of the month, meaning that basic affordability is roughly equal:

http://d33wubrfki0l68.cloudfront.net/56d603c19cf29b4250d6436e5e7164e11120b823/39b70/img/posts/05/20170927-realestate.png

REIN’s a scam unfortunately. I got suckered into it a few years back. Don’t waste your money, and I wouldn’t put much stock into anything they say. If you just use your common sense, you’ll be way further ahead.

REIN told me to put my money in Edmonton housing in 2007…Townhome is “only” worth $50k less than what we paid for it now…

While I agree, Luke, that policy needs to be changed, I don’t think any government will do it because it runs counter to their own self-interest and the interests of the 70% that own property. I would like to think a black swan event would set things back in balance, but we’ve seen what governments do in those circumstances…print more money.

Some will be hopeless and turn to drugs. Others, like me, will carve out an alternative way of living. More and more people are opting not to participate and more still don’t have the opportunity to participate even if they wanted to. In other countries, there would be riots in the street but we write letters, if that. Most of us just complain about it on blogs.

Good chart LF. When most don’t even know what a HELOC is yet they carry a large mortgage you know the end is near.

ICYMI, 3 new foreclosures this week which is tied with Vancouver but whose counting right ? 😉

https://justice.gov.bc.ca/cso/viewNewCaseReport.do

Exactly the policy changes that were needed a long time ago and we wouldn’t be in the mess we’re in now, esp. in Vancouver. Major policy changes that are needed, I predict: probably won’t ever come from the current Gov’t, when they finally do get around to it in Feb. These policies def. wouldn’t come from the Liberals if they got re-elected. The 15% foreign buyer tax in Metro Van and even the new 1% empty home tax in Van, aren’t enough. More needs to be done.

If policy changes needed don’t occur, then here in Vic we could continue to plod along toward a more hollow emptied out, despairing city full of inequality like what Van. has already become for so many. I’d hate to see that happen. Where people can easily despair, become defeated, or eventually be forced to leave to live a more normal life somewhere else, unless they are already established there.

Part of the problem we have in our society where some people are falling into drugs/despair, essentially where they are ‘giving up’, is being caused by this lack of action on affordable housing, in my view. When they have no hope where else do they turn? This is partly how our society is being damaged by this problem. We now see the opioid crisis accelerating, with more people die-ing, and I feel that these problems are interconnected.

If foreign money did get completely cut off, then we would finally really see if it was a big part of the problem or not. They are going to largely ‘see’ this soon in NZ, so I’ll be following what happens there, as up until their policy change, a very similar story had been playing out in NZ compared to here. (though part of me wonders if there are any loopholes in NZ)

Unfortunately, the cynic in me says that our Gov’t likely won’t ever take enough needed action here. They fail to connect the dots. So, we won’t get to ‘see’ if that would dramatically change things here. I hope I’m wrong about that, but probably not.

Would anyone comment on typical agents’ fees on Vancouver Island on a sale of just over $1 million, i.e., the first 100 K and thereafter, and the split between buyer’s and seller’s agent.

Thanks.

http://www.sbs.com.au/topics/life/health/article/2017/10/31/our-crowded-lengthy-commutes-are-making-us-more-lonely-ever

20 min increase in commute time was equivalent to a 19% pay cut in terms of job satisfaction.

Awww… now I’m hurt Hawk – they all agree w/ me that Vic is one of, if not the best spot to be in or visit in Canada 😉

Great post, Beancounter. One of the best I’ve seen on here in a long while. To elaborate using that source:

JR: What causes bubbles like that?

MH: Debt. The reason bubbles burst is that they’re financed by debt. People will lend more and more and more against real estate or companies and the cost of servicing this debt, the interest and amortization, exceeds the cash flow, the profit or income that’s being earned, and there’s a break in the chain of payments. The tendency of debt in every economy is to grow exponentially. Every interest rate is a doubling time. It can be thought of as that. And the debts grow independently of the economy.

When debts grow faster than the economy’s ability to pay, there’s a crash. That’s why the booms, the build-up and expansion of a business cycle are rather slow, but the crash comes very quickly. So it’s really not a cycle at all. It’s not like Schumpeter described in his book on business cycles: a very smooth sine curve. It’s a ratchet effect.

http://ritholtz.com/wp-content/uploads/2013/10/Canada-US-debt.png

Thanks Beancounter. Great article.

For anyone interested, here is an interview with economist Michael Hudson that provides an excellent summary of our local economy.

We are going to need some major policy changes to right the ship. Unfortunately the current government is on a coffee break until February.

http://commonground.ca/michael-hudson/

“JR: So what’s different today from 30, 40 or 50 years ago in terms of the housing situation?

MH: Well, here’s the issue. Vancouver is part of a naturally rich British Columbia territory. It’s well situated geographically. Who is all this natural wealth going to benefit? Is it going to benefit the citizens who live in Vancouver or are they going to let one percent of the population – the political insiders, the real estate developers and bankers – siphon all of this rising property and rental value of real estate, just take it for themselves and shift the tax burden on to the wage earners and the businesses? That’s what’s happening now.

The fact is that if Vancouver acted in the way that Adam Smith, John Stuart Mill and the classical economists urged, they would say, “Look, all this rising land value should be in the tax base.” Suppose this vast amount – really, I think a trillion dollars by now over the last decade of increased land value – suppose that instead of leaving it to landlords to be paid out as interest to the banks, this had been the tax base. Vancouver could’ve supplied public services freely. It could have free transportation, free schooling. There’s no need for Vancouver to have a sales tax. There’s no need for it to have an income tax because these taxes raise the cost of living and, therefore, raise the cost of doing business.

When Vancouver lets the real estate developers and the banks benefit from all this rise in the price of land that increases the cost of living to new buyers, that means you’re priced out of the market. In order to get a job in Vancouver and live here, you have to earn over $100,000 a year. In other parts of the world, people are able to do the same job for much less because they haven’t had a real estate boom. So it turns out the real estate boom that people think is a sign of prosperity and wealth is actually impoverishing Vancouver by driving it into debt. In order to buy into the real estate boom, new buyers have to take on an enormous new debt and the result will leave Vancouver debt strapped.

JR: People are pressured into playing the game.

MH: They really believe it’s still possible to get rich by going into debt, and for 50 years after WWll ended in 1945, that was the case. You could buy a house and as the economy got richer, the value of the house would go up and cities built more parks and schools and urban amenities. The value would go up, but all of that has now reached a limit.

When I first went to work on Wall Street, with the Citizens Savings Bank And Trust Company, basically banks would lend mortgages only if the cost of servicing a mortgage absorbed 25% of their income. If the mortgage costs were more than a quarter of your income, the bank would say, “Sorry, you can’t afford it.” Well, now in the US, almost all residential mortgages below super castles are government-guaranteed up to 43% of the wage earner’s income, of the borrower’s income.

Now, just imagine if you have to pay 43% of your income for a mortgage or for rent. In NYC, it’s common to pay 40% of your income for rent. You may also have to pay another 10% of your income for other debt – credit card, student loan, auto debts. There’s about a 15% automatic wage withholding for a very regressive social security tax and a healthcare tax. Then about 10-15% more regular income taxes and sales taxes. People don’t realize that only about 25-30% of the average family budget in America can be spent on goods and services. So how is the economy going to afford to buy what it produces? It can’t. Most people in NYC cannot afford to go out and eat in restaurants anymore so all over the city restaurants are closing down. In fact, all over the US. In March, it was announced that corporate and business bankruptcies are way, way up. The trend is for bankruptcies.

The Barnes and Noble where I live in New York has gone out of business. The bookstores I used to know are all out of business. Near NY University, on 8th Street, the main street, which used to be the street for bookstores and other big shopping, half of the storefronts are all boarded up, for rent, empty, going out of business.

And in Vancouver, the first day I was here, we walked down a big major street with wonderful art galleries going out of business. Other stores for rent, going out of business. Other buildings obviously had just been renovated, empty, nobody in them. So the effect is to empty out Vancouver.

JR: And who profits from that?

MH: Ultimately, the banks profit because most of the real estate is bought on credit. As I said, the motto of real estate investors is “rent is for paying interest.” They’ll pay all of the increased rental value to the bank as interest because they’re hoping for a capital gain because that’s where the action has been for the last 50 years in the US. Not income. Most people have got rich, not by saving their earnings, but by the capital gain, which includes middle class families that got rich by their house appreciating. That’s why groups that are left out of home ownership have missed this whole capital gain bit.

So you’re having a bifurcated economy: an economy between a generation that inherits trust funds and is able to sort of live on money that their wealthy parents have made in the financial real estate sector and people who don’t inherit trust funds and are literally the disinherited. This polarization is going to widen and widen and become increasingly a political crisis.

JR: The inequality gap that’s occurring is astounding.

MH: And that should be what economics is all about. But if you look at all of the economic models, they’re all about equilibrium. The pretense – and this is junk economics – is that if an economy gets out of balance, automatic stabilizers return it to equilibrium. The reality is just the opposite: once an economy gets out of balance, it tends to veer further and further out of balance. Mathematicians call that hysteresis. Until there’s a crash.

“

Yaks are extra and only available with the deluxe model.

Bitterbear: I seem to mix up yurt and yak. Be careful which you order.

32000 gets me a yurt.

That is some very slippery language right there. Made me laugh. Luke put up a similar, “Victoria’s going to the moon” piece from “Resonance” in early March, which appears to be a similar rag to what Vicinvestor posted. They really are pumper pieces, TBH.

There’s a few of them, and they’re unfailingly upbeat no matter how serious things are, even if the numbers they quote actually demonstrate the opposite of their slant. Incidentally, Resonance actually has a vice-president of “storytelling”. Kind of funny…

|This report identifies where relative affordability exists and regions which will continue to see upward growth despite current high values,” says REIN’s Senior Analyst Don R. Campbell.”

According to RBC we’re at the 2007 and 2009 peak affordability levels, with rising rates and tighter lending rules this seems like total bullshit. Sounds like a small cap stock newsletter trying to lure you into the “secret investment” when there aren’t any. We all have the same access to the info and trends.

As per the 10 year average, the population increased more than 10% from 10 years ago so VREB saying we’re beating the average still is another salesman marketing term for the naive.

Vicinvestor did you read the document?

“Sales appear to have hit a peak, and are fnally heading back to long-term averages. The Victoria Real Estate Board explains that, while the current market is diferent when compared to last year’s record- breaking numbers, “Now the tempo of the market is trending slowly – very slowly – towards more balanced conditions.” While sales are softer year over year, sales in September exceeded the ten-year average by more than 10 per cent, indicating Victoria is in an active market with the availability of appropriate product.”

Yet in their diagnosis they show Victoria is at the end of recovery just before a boom cycle.

REIN is a pumper outfit with teams that like to “coach for dough”. I like how they slip a mere mention of caution into a pumper report that says that growth will be huge regardless of high prices then says : “Affordability is creating challenging hurdles for many buyers to overcome.” That’s not being independent saying two things in same paragraph.

Might as well believe the BS travel magazines polls too.

Anyone heard of REIN? They recently ranked the top 10 cities in BC for real estate investing. Victoria was ranked highly at no 4. Their 2016 report on Victoria is also very bullish. Here is the link to the most recent report:

http://www.newswire.ca/news-releases/british-columbias-top-10-cities-for-real-estate-investment-report-released-655425443.html

Probably lots of contributing factors.

Offers are made by buyers and they can put in conditions they like. If the offer is accepted, the conditions will be part of the contract, aren’t they? If a seller wouldn’t accept the offer due the PDS requirement, then I would walk away as a buyer.

Haha …

But if you are the new owner, and you couldn’t get house insurance or have issue borrowing mortgage due to it, you will be looking for the previous owner for sure.

And no, I don’t have a grow op nor am I considering selling my house. 🙂

Vancouver condo prices have appreciated in a parabolic fashion in the last 12 months. For example, old wood buildings in New West have since prices jump 50% in a 3 month window! This doesn’t make any sense to me. Population & wage growth can’t explain it. Foreign $$$ (foreigners + landed immigrants with $$$) might be adding some fuel but why all of a sudden? It seems like FOMO and/or rush to maket pre-OFSI. Anyone have any more insight?

Sure, might as well use the standard form if you’re going to sell, but it’s really a false sense of security for the buyer. Just because a seller says they don’t know of structural problems doesn’t mean anything about whether there are structural problems. It also doesn’t protect you from being sued as a seller if the court deems what you wrote on the PDS to be insufficient.

As for sellers, no problem filling it out but I would not include it in the contract.

That’s the question isn’t it. If you know your house was a grow op but it was remediated and no longer represents a latent defect, do you still have to disclose it as a private seller?

I suddenly had the image of a house growing legs and lurching down the street looking for its previous owner!

Sorry, we all make typing mistakes.

It might not be the law then, but was the demand from the buyers as part of the contract condition, in addition to house inspection and financing. And they wanted the same format as regular PDS. For our two private Victoria house sales (1991 and 2009), as we din’t built the houses and didn’t make change to them either, besides the PDS we filled, we also gave them copies of old PDS from previous owners.

Think about it, a PDS is probably more important to a private sale. Be it a law or not, buyer should request one as part the sale contract, so no PDS no deal. Sellers should be happy to supply one if you have nothing to hide. If you know your house was a grow op and you don’t tell, it will come back to hunt you.

Thanks for the points. Ya I think a lot of what he says has a, “don’t trust them, trust me, here’s a few morsels to encourage you to buy my service” dynamic.

But his stance on the Vancouver / B20 did get my attention. Of course he didn’t say “no effect”, but rather that it would be the least affected.

Do you know if it’s just RBC applying it at this point or are others now? Thinking of CIBC specifically…

Regarding that Ross Kay interview, sounds like he is slamming BetterDwelling at the start. Some “bloggers” that take his stuff and then try to analyze it, then get invited to the CMHC housing symposium.

Other stuff:

He says the best time to buy depends on the location and category of home.

I haven’t seen any evidence of that, except for that fall may be better time to lowball. However this is an interesting topic to look into, deserves more attention.

He says interest rate increases will lead to reductions in average price after a delay.

While I agree that affordability is very important, an increase in rates doesn’t mean prices will necessarily decrease. Lots of examples where this did not happen, such as Vancouver condos that went stratospheric after rate increases.

“I can predict and forecast with 100% degree of accuracy” – This one requires no response.

“100 real estate associations will strategically release monthly sales numbers to benefit the overall members of the canadian real estate board” – VREB always releases their data at the same time, so I guess they’re not part of that 100.

I also doubt his argument that many people are making buying decisions based on real estate board press releases.

Don’t get me wrong, I think Ross knows a lot, and I am 100% in favour of Ross’s stated goal that people should be able to make their own decisions and buy/sell on their own if they want. I just don’t think his approach of obfuscation and difficult to understand reasoning is the way to do it.

Maybe he thinks foreign money is such a big force that credit availability is less important.

Or you could argue that if affordability for locals were a constraint in Vancouver it would never be at the valuations it is now.

I think that it will impact Vancouver though. I can’t imagine that the condo market which is currently on fire is not driven largely by absurd speculation on the part of locals that are leveraging other real estate in the belief it only goes up. Eventually the banks stop lending.

Listened to the most recent TDN episode featuring housing market consultant Ross Kay. Love him or hate him, he does have some decent knowledge of the Canadian RE scene.

One of the things he says emphatically in this interview, is that the upcoming B20 stress test will have a lesser effect on the Vancouver market than any other city in Canada. He makes his point at roughly 31:40 below. Despite him begging the question, he doesn’t really provide a reason for his assertion, as though it’s based off of his firm’s proprietary metrics. But he’s sure of it.

I was thinking about this, and what could make a stress test less effective in Vancouver than other markets. The only thing I can think of is there are either all cash buyers in abundance, and or, that there are huge amounts of downsizing buyers which in effect, is similar to an all cash buyer. I just don’t believe that there’s enough of them to really counter the effect of stymieing credit and a shift in psychology. RE markets are run on credit, not cash. Anyone have any idea?

https://www.youtube.com/watch?v=2DaHYukGvJ8

Not specifically. It is very tough to use it in court because everything is worded as “are you aware of”. So if there is a defect, a buyer would have to prove the sellers were aware of the defect.

What law mandates you must include a PDS if selling privately? You must disclose latent defects of a property of course, but I don’t think that means you need to fill out a PDS form as used by the BCREA.

Thanks for the link, Local Fool.

Along with the usual commentary about housing, I thought the interesting piece was the discussion about corporate sector debt being high as well. To me that is more worrying than household debt.

The vast majority of homeowners will just stay where they are if the market significantly dips. Only a few percent will be the poster children for Hawk’s weekly insolvency search. Major corporate debt could have a deeper effect.

Thanks for the link, Leo S. It would be interesting to plot some of that data on a graph of some kind, showing their estimates for different regions. It would also be interesting to hear if other developers agree with their numbers.

I am curious how much of a construction premium there is because of the current boom. If the general market softens, how much do construction costs go down? Materials are not in such high demand, and contractors are a bit more hungry…

“Much of that borrowing has been mortgage debt, and that’s fuelled the stratospheric ascent of housing prices in recent years – an ascent that has many observers warning about a catastrophic correction similar to that the US suffered in 2007-09.”

That’s hilarious Vicinvestor. The only ones saying my posts are nonsense are you homeowner pumpers up to your arse in major debt.

Mike probably just got sucked into a pile of condo presales he’s trying to flog to the sheep who just got cut out by the stress tests. Only the desperate pumps out that level of bullshit.

While hawks talks bearish none sense, Michael deviates to the other extreme of bullish delusion. Condo prices @ $2500/sqft are double the current Vancouver benchmark. What makes you think Michael that this will happen? What has changed? Why should there suddenly be so much interest in Victoria condos?

Michael:

Are you saying that a thousand sq. ft condo downtown will be selling for 2.5 mil? What thousands of new condo units going up in the next few years do you really think that there are that many people who actually have 2.5 million?

Dear god, Michael…

(hugs)

Local Fool:

Thanks for the stats. I wonder why I ever moved my assets out of Canada. The scary thing is how many of my Toronto friends either have or are in the process of doing the same.

After the Binge – Is Canada’s Debt Hangover Here?

“Canadian households are more indebted than ever before. One metric frequently cited as a benchmark for household debt growth, StatsCan’s debt-to-disposable income ratio, reached a record 167.8% in the second quarter, up from 166.6% in the first.

Much of that borrowing has been mortgage debt, and that’s fuelled the stratospheric ascent of housing prices in recent years – an ascent that has many observers warning about a catastrophic correction similar to that the US suffered in 2007-09.

That new debt drove private sector debt-to-GDP ratio from 182% to 218% over that period, prompting the CCPA to note that “This increase of a fifth in only five years is the fastest growth of any of the world’s 22 advanced economies over that same time frame…Canada has never before led advanced economies in private debt accumulation.

…Canadians might not be able to avoid a sharp, painful correction. The CCPA points out that countries that have accumulated private-sector debt at a rate similar to Canada’s in the past have frequently run into problems. It says Japan recorded five-year growth in its private debt-to-GDP ratio of 28% by 1990, after which its economy remained depressed for a decade. “Five-year private debt-to-GDP growth in Portugal and Spain topped 50% in the 2000s, which ended in calamity following the 2008 financial crisis,” CCPA says.”

http://www.cambridgefx.com/blog/insight-binge-canadas-debt-hangover/

Luke:

Just to clarify, what I suggested was high taxes on all foreign owned homes, vacant or otherwise (proving vacant is why to hard and too easy to get around); said taxes to be ratcheted up every year until we have milked the foreign owners dry and they sell out. The advantage to a gradual increase is that you dont have a thousand homes dumped at once. Then extremely high capital gains to capture any gains after they decide that they cant afford to keep paying the high property taxes every year. The idea is to milk them dry before we serve them as steak.

It’s interesting how the highest $ per foot ever recorded in Victoria, for house or condo, is $2500/ft. It was a 4000 ft unit that sold for $10M. I believe it won’t be too long before $2500 is the average, as core condo land skyrockets. For perspective, Central Park units are already pushing $10,000USD/ft.

I don’t doubt that for a minute to be true. But how many on this blog knew that an RRSP was protected before this morning?

Would those same people now think of cashing in their RRSP’s to pay down the mortgage? They would only be saving $400 a month for every $100,000 they paid down on the mortgage.

Certainly true, and never was a factor before. The globalized world where vast wealth is being concentrated in the hands of fewer and fewer looks like it’s just going to continue and possibly accelerate. Trump and Brexit were partly responses to people’s concerns about these trends. Now, with AI and automation set to threaten jobs for the masses everywhere, one does wonder how the world will look with 1% or less than 1% holding virtually all the wealth in the not too distant future? I found the Paradise Papers stat’s vastly interesting, where here we have 80% of that wealth hidden by only the top 0.1%.

This is why the Prov. and Fed. Gov’ts need to look at protecting housing from being used as a safe haven for this vast wealth, much as New Zealand’s Gov’t appears to have just done. They are already too late to the game, but ‘better late than never’ I always say. I think it’s time we all wrote to our MLA and/or MP urging them to implement some of Barrister’s suggestions from the previous thread… re. massive capital gains tax on non-residents, and massive property tax on vacant properties. We also need new protections to ensure housing is only reserved for Canadian citizens/ PR who are actually resident here as well.

I agree, and if house prices fall for the better of all society, because we finally see the light and implement protections for our residents then I’m not necessarily going to vote out the current Gov’t.

After all, I bought my house to live in (what a concept) and if all the other housing prices fall and I need to move, it will just all be relative anyway. High house prices only benefit me if I decide to sell and move somewhere vastly cheaper, and I have no intention of doing that in the near future. Baby boomers on the other hand, may beg to differ.

I strongly suspect this is why they’re so afraid to take any real necessary actions. They fear a backlash in the next election from the majority of the province that are home owner’s that will send them back to just two seats… the Greens, on the other hand, see it as boosting their popularity and hence you have Weaver heading on that tangent…

Here’s an interesting tool I just stumbled across. High profile development consultant in Vancouver has a tool to roughly estimate construction costs of condos in various munis

http://www.bdconsultants.com/index.php/tools/tool/cicalculator

Seems like about $250-$330/sqft to build + land. And selling for well north of $1000/sqft.

Here’s yet another price slash for ol’ Hawk… 1415 Monterery Ave…down $50k to $1,299k. I suspect it may have to fall further.

I recently took a look at this open a couple weekends ago, curious because of it’s location near the OB village, which is a cache that continues to elude me. I left quick, because – for one thing, the slow oversized flies, flying around… you know what that means… something is decomposing in the walls feeding the flies…

Then there were the creaks everywhere you stepped so loud they were annoyingly loud despite the busy open house crowds. Imagine trying to sneak around at night? Not happening here… Another attendant to the open happened to do a mis-step and a piece of wood below a door came flying off… I said ‘you break it you buy it’ to a look of horror…

There’s so many old places like this in OB/Victoria, no doubt a reason we see so many price slashes that when a rare quality home does come up that is also priced well (perhaps even more rare as they know what they’ve got) – the overtired crowds swamp it with offers.

A+ quote

I am sure there is a very small percentage of more or less “strategic” bankruptcies with assets carefully stashed in untouchable forms or transferred away well before the bankruptcy. That would be the minority.

The majority would be hard luck stories or bad choices. Many of those would never have had much of an RRSP to start with and certainly won’t by the time they reach bankruptcy.

Talk to a bankruptcy lawyer or trustee. Very few of their clients sale through the process with a big fat RRSP.

My favorite Galbraith quote is:

The only purpose of economic forecasting is to make astrology look respectable.

If you have not yet read “The Great Crash” by John K. Galbraith get the book from the library. It is both an easy and humorous read that has great insight into the psychology of a crash. One point he makes is that no politician wants to be the one blamed for pricking the bubble and ending the party.

John Drake: Three consecutive years of 10% losses might a have a very different broader economic result than a 25% drop in under six months. House prices have almost doubled in four years, a 25% drop is not outside the realm of the possible although far from probable.

Before I am accused of being Hawk, I should point out that I pulled my investments out of Canada a few years back and other than my house I dont have a dog in this fight as they say in Alabama.

That’s what it looks like to me. Prices are so high on south coast, society can’t afford to keep it going, and yet, we can’t afford to stop it.

Either outcome has a potential to disaster, it may just be more of a question as to how fast we choose to get there.

If prices fell say 5% in one year that would only be pull back. If prices declined at around 10% a year that would only be a correction. If prices fell 25% or more in one year that would be a bubble bursting.

When a bubble is capable of erasing all of your house equity in one year then there is some serious shit happening. And that would put BC into a recession or depression.

Those being defined as…when you’re neighbor loses his job that’s a recession. When you lose your job that’s a depression.

Not if you are planning your bankruptcy.

Generally, I agree with what has been written but there is a difference between a bubble that deflates slowly and one that burst. Bursting bubbles often create a panic that might have far greater consequences than just readjusting prices. The panic from a bursting housing bubble has been know to bring down banks and freeze credit that might well not be effected by a slowly deflating bubble.

But you must supply one if buyers ask. We sold our homes privately before (twice in Victoria and once in ON), and all the buyers asked PDS as part of the sale documents, as they should.

You can state “no knowledge” if you don’t know, but you can’t and shouldn’t lie on PDS if you know, regardless if you could be sued or not. Remember what goes around comes around?

All bubbles burst because that is the only solid definition of a bubble.

And that means the only way you will ever know for sure that you were in a bubble is after it bursts.

Saying that we may be in a real estate bubble is forewarning people of a possibility of a rapid drop in prices in the future. We can go back and look at past bubbles and when and how they burst. And by those metrics we are well past those milestones. However we have never been in a market that has been fed by such humongous amounts of cash floating around the world looking for a safe haven. Our house prices are sustained by this constant flow of cash. If that cash flow was disrupted our prices would fall to historical norms supported by the local market.

So while it may walk like a duck and quack like a duck you won’t know that it was a duck until it’s on your dinner plate.

I believe RRSP would be protected in bankruptcy, except for contributions in the last 12 months. Pension plan would also be protected, so would life insurance with a beneficiary other than your estate.

Of course in the real world most people have probably liquidated their RRSP in the financial hardship that leads up to bankruptcy.

You’re welcome 🙂

All bubbles burst, without exception. The “degree” if you will, of damage when it bursts is usually dependent on the amount of leverage used to push an asset up to meteoric heights. Parts of Canadian real estate are a perfect example of this in action.

If an asset climbs in value aggressively and doesn’t go back down, then it wasn’t really a bubble, although that’s a pretty crude and simplistic generalization.

Thanks for the clarification. That is roughly what I thought. Do you know if there have been any legal cases involving what has (or has not) been written in a PDS?

I tend to agree that Victoria’s house prices will mirror Vancouver to a large extent. On the other hand I can easily see a major drop in houses prices in both markets. I am predicting such a drop but it is far from impossible. Why is it that people who see no problem with house prices increasing 20% in one year also find it inconceivable that they could drop twenty in one year.

In addition to watching our big sister I would a very close eye on the US Fed.yo see where interest rates are heading. A return to 6% mortgages over the next few years is as likely as not in the next few years. While far less likely any major moves by the BC government to curb foreign investment could easily crash the market. Last but far from least keep an eye on where the Free Trade talks are heading. The political realities could easily trump (no pun intended, well maybe a small one) the economic ones.

Not all bubbles burst but we should kid ourselves that the Canadian real estate market has all the hallmarks of a bubble. Tulips are now at low sale prices as well.

Yes, someone selling their own house without a realtor. The buyer may or may not be represented.

The PDS is a requirement for any house being sold by a realtor. The listing will not be accepted without a PDS. However it could be struck through instead of filled out. For a private seller, they do not need a PDS.

By “private seller” I assume you mean where a Real Estate Agent is not involved? That is a very interesting question that I would also like to see cleared up. Obviously, it is part of the standard PDS (Property Disclosure Statement), but I assume that is just industry “best practice” rather than a legal requirement?

I have been told (not by a lawyer) that the current PDS has largely not been tested in court. I always hate seeing a PDS on a house built in the 1970s where the owner claims they have no “knowledge” of asbestos in the house. Hear no evil, see no evil.

While there is certainly due diligence required on the part of the buyer, the seller clearly misstating this kind of thing should come with penalties of some sort.

Bankruptcy is a clean option but only if you dont have any other significant assets such as RRSP’s or a cottage property or a boat. If you have investment properties then those would be sold as well.

I wonder if we are going to start seeing mass timber condo towers as a way to drive down construction costs? https://www.citylab.com/design/2017/10/why-timber-towers-are-on-the-rise-in-france/544098/

Dasmo, maybe developers can use that technique to fatten up their razor thin profit margins.

@freedom_2008. I think that all applies to realtors requirement to disclose, not private sellers.

Also it seems the RCMP used to have a database of grow ops, but no longer. http://www.waynepasco.com/articles.php?ID=210

http://www.rew.ca/news/sellers-series-selling-a-stigma-how-to-list-a-former-grow-op-1.2095928

http://www.reincanada.com/aboutus/media-news/real-estate-news/stigmatized-real-estate-listings-are-disclosure-rules-fair-homes-were-grow-ops/

I am not personally supposed to comment on individual listings. Quick way to collect a complaint from the VREB. I will leave the commentary on individual listings to the comments 🙂

Problem is actual racists are also for the foreign buyer tax. Unfortunately that pollutes most rational discussion that can be had about it. One look at the forums for vancouvercondo.info will tell you that.

Barrister said: ”For example, in Vancouver perhaps the tax should be eight times the present property tax. This can then be ratcheted up every year until…”

LeoS said: “I see this very simply. Residential real estate should be for people living and paying taxes in Canada. ”

You two should run for federal politics; I’d vote for you.

The commoditization of RE for the benefit of foreigners and speculators must be stopped. My current RE would make me slightly wealthy by the standards of 5 years ago, while inflation is only up 10%. This is crazy, my meager RE holdings should not have appreciated to the point where young Canadians are deprived of the benefits of home ownership.

Politicians needs to grow a set of balls and get tough, without worrying about PC backlash. If my RE holdings drop in value by 30% I’ll be happy; it won’t be a sad event… although my kids might be pissed off that their recent paper profits are wiped out… but, they will eventually get over it.

Thanks freedom_2008 and Michael. Some more info on grow ops: “Under common law, the onus is on a buyer to satisfy him or herself about the quality of the real property being sold.2 It is the buyer’s job to find any patent defect, being one discoverable by a reasonable inspection or reasonable inquiry. A latent defect is the opposite. The courts effectively define a latent defect as one that is not discoverable by a reasonable inspection or inquiry, and which makes the property dangerous or uninhabitable.3 A seller or listing Realtor must disclose any known latent defect.”

http://www.bcrea.bc.ca/news-and-publications/publications/legally-speaking/legally-speaking—may-2016-(486)

What’s interesting is that it seems (my interpretation, consult a lawyer) a private seller only has to disclose a latent defect if it will cause the house to be dangerous or unfit for habitation, so it seems a remediated grow op may not have to be disclosed. Whereas the definition of latent defect is much broader for realtors to include unauthorized modifications, anything that would be expensive to fix, etc.

From http://www.courts.gov.bc.ca/jdb-txt/sc/98/10/s98-1050.txt

The doctrine of caveat emptor

will not operate to deny the plaintiff’s recovery in the

following situations:

latent defect which renders the premises dangerous.

Hi Aaron,

the open house I went to was 2051 Kings Road. It is an estate sale and I think it’s the lowest priced home currently in OB for $790k. If you go have a look – wear a mask as the smell of ‘cat’ pee was overpowering! The home has good ‘bones’ (I think) and could be saved but it’s definitely bait for bulldozers. I noticed contractors were there looking as well.

Luke we were there when the open house started and named that place “Cat pee” house for reference later in the day when we were recounting the houses!!!!

Actually upstairs was ok with a remodel but we are looking at a place to put in a suite and downstairs ceiling height would not work. I also saw a couple contractor’s in there.

For any current buyers on the fence, here are my favorite 2 crystal balls for seeing into Victoria’s near future – Big Sister and Mr. Market.

Recall how Victoria prices raced higher in Spring ’16, shortly after Mr. Market did. Likewise, how our prices stalled this Spring.

As for Big Sister, many overlook that where Vancouver leads, Victoria typically follows within a few months. And Van prices have jumped alot lately.

Lol, hawk where did I ever say I bought a month ago?

You otoh, should really take my advice above and not miss your boat again 🙂

From what I read, in BC, QC, ON, full disclosure by owner of a former grow-op is mandatory regardless even if the house has been remediated. But it is not mandatory in Alberta, if a grow op has been professionally remediated there

But you only bought back in a month ago Mike so that means “we’re” down $40k plus. Ouch!

Neighbor house just took a big hit of $400K plus after many $100K’s of renos. A land hoarder who got caught I believe. So it begins.

@LeoS

I believe if you’re asked about it, then you can’t lie (or risk being held liable). Otherwise, I don’t believe you have to disclose, but not positive.

If we’re playing hawk’s game, then I guess we’re up ~18k past 2 months.

Aug 749,900

(Sept 795,000)

Oct 767,250

Does anyone know if a private seller needs to disclose a grow op that has been remediated on a property when selling?

Don’t mind Mike. He’s just choked he’s down $40K plus the first month back from buying back in after playing bear for 2 seconds. Shows how edgy he is when he doesn’t even read the informative article. Must suck to lose so quick on top of all those buyer/lawyer costs. 😉

I thought the article was good information for home owners that are sinking in debt.

And while we all want to pay our debts, sometime it’s better just to take the bankruptcy route and let the bank, their share holders and depositors take the monetary hit.

I think it would be good information, to explain how to both protect your wealth and how to prepare for bankruptcy but not go as far as to counsel people on how to break the law or how to stick it to the banks.

If you think Harvey Weinstein’s wife immediately going for a divorce wasn’t a move to protect their wealth from creditors then you’re naive.

Don’t think the article I posted was a Madani inspired doomer piece. I kind of liked the compare and contrast to the US market, in terms of legal remedies available to those who are in a position to default.

It was funny, the bankruptcy remedy seems so obvious, but I have occasionally experienced in conversation the same sentiments that this article talks about. Kind of wonder how many people have no idea that there is a ready way out, unpalatable as it may be.

Ah yes, the geniuses at Maclean’s, spreading their wisdom again 🙂

Here’s how Canadians could walk away from their homes if house prices fall

“…the legal risk faced by borrowers who try to walk away from their loans is so great, it’s been frequently held up as an argument for why Canada won’t see anything like a U.S.-style housing crash and its repercussions for the economy.

That’s certainly the position now widely held by Canadians, as well as people who invest in Canada, such as big international institutions, mutual funds, sovereign funds, hedge funds.

Only it’s not that straightforward.

What is far less known is the fact that insolvency legislation in Canada supersedes a lender’s right to sue a homeowner for a shortfall. In other words: if a homeowner who is unable to make mortgage payments files either a personal bankruptcy or a proposal in Canada, the shortfall (now unsecured) is included in the insolvency proceeding and fully dischargeable.

It’s the Canadian insolvency version of America’s jingle mail.”

http://www.macleans.ca/economy/realestateeconomy/heres-how-canadians-could-walk-away-from-their-homes-if-house-prices-fall/

There was that data on percentage of mortgages that are greater than 450% of the applicant’s income. However I was never able to find the source for it.

Gulf islands.

I would love to know the stats on local mortgages. I think debt education really is so bad that there are a significant number of people who walk into a broker and walk out thinkinging “Woo I’m a millionaire, let’s do this!”.

“I don’t think people are out there buying $1m plus homes in the core with only 20% down are they? I’d imagine it’s people with lots of equity already. Is anyone really taking out an $800k plus mortgage??!”

They buy it all cash then use the Smith Manoeuvre

True Freedom, race does not dictate foreign or not. This place was built on the backs of Chinese slaves. Pig Iron Jack made a pretty penny in the trade…. It’s why we have the oldest China town in Canada.

This is why it’s this is an easy subject to sabotage. Just pull out the race card.

The way around that politically is to declare a housing crisis and introduce a temporary “non-resident” buyer ban. Has nothing to do with race.

Those in the industry love that the racists pile on though….

1222 Crown Cres in Maplewood slashed $85K.

851 Coles St new build slashed $100K.

231 Homer Rd in Tillicum slashed $40K.

Looks like the $40K average/median tank last month is showing effects early.

Given heritage we have here in BC, Asian buyer != foreign buyer. Yes, people do like to have investment that can bring in more income, and Asian buyers normally may not mind sharing house with others, but these people may be from Local or Vancouver or Alberta. Leo posted before that in 2016 foreign buyers here were: USA 106, Asia 44, Europe 25, Other 23.

Hi Aaron,

the open house I went to was 2051 Kings Road. It is an estate sale and I think it’s the lowest priced home currently in OB for $790k. If you go have a look – wear a mask as the smell of ‘cat’ pee was overpowering! The home has good ‘bones’ (I think) and could be saved but it’s definitely bait for bulldozers. I noticed contractors were there looking as well.

Re. Asian buyers – I haven’t been going to many open houses lately so wouldn’t know if that was a trend, but interesting observation.

Also…

There may be lots of slashes on overpriced junk out there, or just overpriced even if not junk, but there’s still some examples of places going over asking as well…

Like 3356 University Woods – went at $100k over asking for $1,675k. Totally dated 1989 build and fixtures, but roomy lot and house in a very high end enclave.

3033 Devon Road is another that went $100k over for $1.4m and this 1957 build is almost certainly a bulldozer bait. It’s on a huge lot on a quiet street near Uplands though.

Did anyone notice the home on Landsdowne in Uplands that was priced well over $4m and that went recently too? My PCS doesn’t go that high so not sure what it sold for.

It appears there’s still some people with deep pockets still out there searching for whatever works for them.

Personally, I think the stress tests may effect the condo or cookie cutter entry homes out in places like Westhills where people are probably mostly buying with a mortgage and not equity. I don’t think people are out there buying $1m plus homes in the core with only 20% down are they? I’d imagine it’s people with lots of equity already. Is anyone really taking out an $800k plus mortgage??!

Back to housing –

Today I went to an open house and the place was complete bulldozer bait for almost $800k. Lot value I guess.

Anyway, it was busy, but the thing that struck me the most was the full spectrum of ethnic diversity that was in attendance. There were the whites of course, but also there was a muslim family, and groups of Asians. It’s quite evident from the latest census data that Canada’s demographics have changed, and that will likely continue, as most of our new immigrants are now coming from either Asia or Africa.

I’d wish anyone taking on that place well as it needs a lot of love.

Luke was this the place on Fernwood?

I couldn’t believe how many people were their on Saturday for the open house.

From the past foreign buyer thread. We have noticed the past few weekends how many Asian buyers have been out looking to purchase in the core for their child going to University. They seem to be looking at places with pre-existing suites so they can also bring in income as well. The places without suites / unfinished basements etc I have not noticed as many Asian buyers looking for their kids. But this is a general observation.

Barrister, I posted quite a few that had huge slashes like that but the bulls yawned while Rome begins to burn and credit screws tighten. I believe I know the house but if Leo won’t post it then he has a reason not too.

Hawk:

How did you miss the big price slash on that low ball?

While there is no perfect solution to the days on market I would suggest that if the house is relisted within two months by the same owner then it is not a new listing.The houses that are taken off for Christmas and then relisted in the new year are really not “new” listings. Changing a real estate agent certainly does not make it a “new” listing. Nor does it become a new listing because a deal does not close.

Trying to get anything meaningful from the stats over Christmas is difficult at best. Unless you get something unusual like an increase of listing instead of a drop the numbers dont necessarily mean much.

Does anyone know which banks are already applying the stress tests?

Not a good start for the bulls. Which hood was that low ball Leo?

I suspect we’ll see averages/medians continue down as stress tests kick in early as RBC is doing. HPI is six months old as Ross Kay has stated many times, and he helped create it.