How to mislead with charts

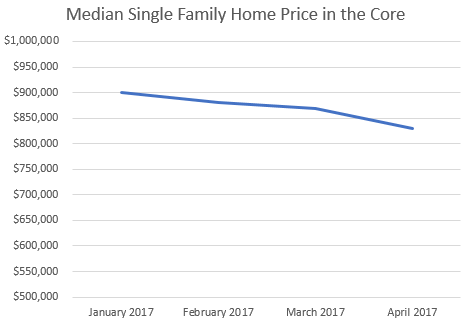

What would you conclude if I showed you this chart?

With 4 months of declining medians it seems like prices are declining in the core, right? Are people maxed out on price? Are the Vancouver buyers not coming? Are people scared of the green party winning a landslide? Is it those Chinese capital controls beginning to bite?

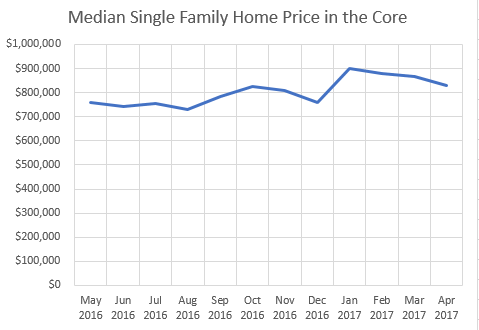

Let’s zoom out a bit.

Hmm.. Looks a bit different but perhaps a market top? Doesn’t this stupid website say the market is “ludicrously hot” on the right side?? Hardly seems like strong appreciation in the last year with prices in April 2017 and May 2016 close to $800,000.

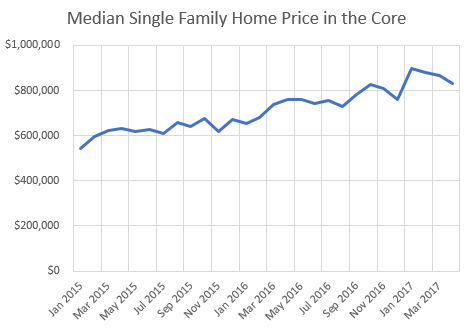

Let’s zoom out a bit more.

Now the graph gives a totally different impression. The big decline from the first graph is lost in the noise and the actual trend of about +$100,000/year reveals itself. Monthly medians are notoriously variable. Sometimes that variability manifests itself in large changes (like the increase of $140,000 from December to January) and sometimes it results in a stretch of steadily declining prices.

Could it be some sort of top? Sure. If we get another 4 months of price declines then there is something going on, but so far it’s just that much noise. It’s human nature to spot patterns in noise, and so we glom onto these things when we see them. This is why I think that while data is interesting, it doesn’t really help people form an accurate opinion of the market without interpretation. For example Zolo has a great page of stats for Vancouver but what they are actually highlighting in many cases is the noise, and in other cases they have the signal but it’s not obvious to someone not familiar with the details of real estate markets.

Regarding our market, I still believe that before we see prices slow down we would need to see a matching pullback in market conditions. This would be something to watch out for and I’ll look into what a market top actually has looked like in Victoria in the past. When the current runup is over, will we get any warning, and if so, what should we be looking for as an early warning of the market rolling over?

That picture was from an old article from last year.. https://househuntvictoria.ca/2016/07/08/how-many-skyboxes-for-a-dirtbox/

I didn’t look up the prices at that time 🙂

New post: https://househuntvictoria.ca/2017/05/01/first-hints-of-a-decelleration/

$1.6m

Does anyone know what 528 St. Charles, in Rockland, sold for? It has been on the market for months now.

Leo:

In your VV post you used a picture of Black and White as the background of your no. of condos to purchase a SFH graph. I know it’s a minor detail, but you could buy a SFH in a core-ish area with what a Black and White condo costs.

Just saying…

10 years of damage could be done in one or two as the US found out the hard way. Can’t happen to us cause we’re…..we’re…. conservative ! Yeah….conservative ! 😉

http://blogs-images.forbes.com/jessecolombo/files/2014/04/USHousingBubble1.png

totally

@LF

“I would presume that any or all of the “Big 5” buying HCG loans would be a contradiction in terms, would it not? The reason HCG said yes to the borrower in the first place, is because the former said no.”

They will buy at a discount that reflects the risk involved. The loans are backed by collateral, i.e., real estate, so at a 50% discount the loans are probably a good investment. Or at least so we can infer if the Big 5 buy them.

The size of the discount is what would be interesting to know. It would indicate how far the Big 5 think RE might fall.

Hawk enjoy your imaginary Victoria market crash for the 100th time in the past 10 years. Maybe an imaginary house will go down 50% and you can buy it. Than you can imagine you moved into it. Than

you can imagine the market goes up 100% and than you can imagine to sell it. Its a wonderful life of fantasies and adventures. Who cares about reality in Hawk`s fantasy world.

data:image/jpeg;base64,/9j/4AAQSkZJRgABAQAAAQABAAD/2wCEAAkGBxITEhUTEhMWFRUXGBwXFxcYGB0eHxgbGhggGh0bIBsaHSggGRolGxgfIjEjJSotLi4uHx8zODMsNykvLisBCgoKDg0OGxAQGzImICUrNS4tLS0xMDItLS0tLS0vLS8tLS0tLS0tLS0tLS0tLS0tLS0tLS0tLS0tLS0tLS0tLf/AABEIAMoA+gMBEQACEQEDEQH/xAAcAAABBQEBAQAAAAAAAAAAAAAAAgMEBQYHAQj/xABFEAACAQMDAgQEAgYHBgUFAAABAhEAAyEEEjEFQQYTIlEyYXGBkbEUI0JSocEHM2Jy0eHwFRaissLxJUOCktIkNFNzs//EABoBAQADAQEBAAAAAAAAAAAAAAACAwQFAQb/xAA3EQACAgECAwUGBQQCAwEAAAAAAQIDEQQhEjFBEyJRYXEFgZGhsfAUMjPB0SNC4fFi0hU0UiT/2gAMAwEAAhEDEQA/AO40AUAUAUAUAUAUAUAUAUAUAUAUAUAUBE0HU7N4uLThjbYo4E+lgSCM/MHPyoCXQBQBQBNAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAcD6p4rUnUqrXV1balj5zXCiG3b32ktHyyrooS40D3yTQHZvCb3G0ena7c8x2tK7PETvG6M5gAxJyYk5oC2oCr6/rmtINglmMDEx3J/l96w+0L7Ka81rLb9TVpKY2zxPkjPN4h1KlSwJXcJGztOe3tXJr12sUlxrbrsdKWi07TUXv6m0U19GjhntegKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAiazXpbwzKCc5IGPfNc/W+0I6XCabb8CcK3Ig2+voTBAUdyXXH2msj9twX9jL3pts8RW9X8ZWbQMkYMEhgYHvAnsP+1Th7QeoXBGLTf34FkdG1HjbKPxR4hF3TwrG2JDbrbnfE5+A4x9R3PFW1Qs/tIf0qu9OSMTbvu4QLr729s+pnA2niJfLDvBP24qN1ttSy47evI10xrseNvhzNt4L1a6XebmqN7zNoJe6W2FZMAGQPi4HyrNX7TnBvijnwW/7o91GkUl3OfuNM3i7T5h0PYevk/hVn/l31r+f+DMtBZ9/7OVdQ8LaZ/wBKnU6ctfu+Yt3ad1sl3LJukklhcExAlAYPaa9rPfuffwJLQSfP9v5OldO8UWrdi2r3LTOqqjbSVXcBGJBjjiTUF7XbeOD5v+Dx6CfFj+P5Hh4wswSzWxBj+sOf+DH3qS9q/wDH6/8AUk/Z0/vH8jOo8V2WBUm3EEN+tIiRH7mDXj9q/wDH6/8AUkvZ0vH5L+SH0frGk09gWFvKfLkw93c0Fiwk7RAloGMCKT9pWxe9ePXi/wCpUtG5PuvK938lh/vfb3KPQQxHDsTBPMFBOJPPakfa2ZY4fr+6Ra/ZssZz9P5NRXZOYFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAFAeMa8bBmOpdQ9bG4PSsGCk5mVX5mc/hXyGttv/ABfayj+Xknyx4v6/6OhVTxQSj1M91XrFy6GEDLAwFOW/ZEnkAQZqd2sldniws/Q6VGjhU0+ZzHxx1q2t+3pt5NtXVr7DG4z6uM8Y9663svTRX9SX2jD7Tvn2UoQ54fxwTPEt8WX9TKAxJVQSY9RwFPBHHzPExX0ClXJueeR8hDS3xrVU1zXqW/he1cuqNRqH3G2DbsLt5PBYnJMD04PZq+V9p6iMpOEfV/wfa6CidcIrHJYNH57sq20E7WOwBD67hmSfpJJP972rj10uU/N/Q2uEa27GyOUKmM+gwJU5uHk/TPb3PtU5Qw8Nb9fQtjJSWUTDpECl9zFU49Hx3W+3uY+p5xWrTw001LtZ4eNknvhGG3U2qahFbnk3DZjaTbtnczBD6rh/zP8AEZrKtLZJO5Lbx8i7+nG3d959Bi7bRQAHLR67h28vyAMe+c5wtVxcpPl6ehdCUnni2GrlsjDnbP6y56eI+EfIY7/umtFNrpsViSbXLPIhdWr63DOE9tuY9a0e9cbme56rgCHCAYHE+w78tFXe0NfLVWdrPCfJffqY9FpoaGDrXLL5839ozniLqLDU2FBG34gRycxPyxIx7/OpUUcNLn1NE9RFT4eiO0dE1nm2UcmTA3fWM/4/evoNHqFfUpdeT9Tg3QUZtLl09CfWoqCgCgCgCgCgCgCgCgCgCgCgCgCgCgCgCgM34p6o6QtowZyQYJPYD5AZNcb2hrZQkoQljHN/sjoaLTxlmUlnwRkr+ouuSWLMScerlu7Y/ZHt/DiMftLU6a6UXTHGF3m+bf39TT7N0uop4u3knvslyS+v+hkoewbuF9Xf9p/p/qM1zfX6fI6hVt4d07T+qPqGweskiObmTz8/p71qWtuX93Ly+RTLTwfQmN0HQncRYcsyhElziObk7p3Z5zMD97MJa7U5WJbLntz8jP8AhZZQ5atbVVbasABstieAOW54j8vnVEnlty9XtzNySSwiVZ8y2A9vcP2LfqH/AKmycjH3j51OEnW+JP12KZqFj4JEZyZkBznakkZczubn6/LBqLeW+LHi/wCCxRUVglxc8qYc20MKJA3PJBPOcn6ST7Gqu4pYysvnt0KU61bjqeHqFwWzaO820iR6Rucmex9zOO5HtWt6ix19lnuvpjoiS08OPtMbiNBsRgbvmEL634y3bg8CJ9OcLiss22u5jfkLlNxxEbvsXbIcbjveSML2XmO0fY1JPbOV4L1JwjiOC00dw27Zf1B7mVn2HA/DOc5NQWnlbao9PvJi1Ek3nwMx1bTPd0twmSw9duBkFRjAzkz+NfSOMV3VyMMG+Iuf6LPEu4iy8jcIz++OPyI/Cq9F/QucG9pcvUu1NPHVxrmvodRrtnKCgCgCgCgCgCgCgCgCgCgCgCgCgCgCgK/rXUPJtkj4jhZ4n3PyHJ/zrJrdUtPXnq9kvMv09PazUenU52SXJY7TMknOFmSxPYt/o4r5STfPfP1Z9HhR2W3Ql9RVWVWHlLIjav7CDvI7nGMRI5jNFWU2t3+7M9EnGTh82RmtIApm3Lfsg/Cg+fYn7RP9mulfpOyqjPiy30X30Fepdk3BLZdR3UbCVaLY3DCgxtQc5Hc8YgjHtWOuPBjOXj5k4Zw4r4iio1FwbFt2wwgRjag5iI9R+UHj2qeov34kuXzZGP8A+eHe3Y3qNEFUEG3LnagB4UcsMYJx+K+1URsy8b7fUnXfxvGBzpbBvSEUlpS2d2EUcsBHJxkf2K8uzFc+XzKtSmu8ngZ14UNFtEhf1aQe/duMxHPOD71KrOMyb8WXUZccs88tthMAqnpVSx9TnE8ZiYn+9U1BPf8AY9zFTxjcZFjaCSsrbyfVl3P2yc9+5FXQqc4uSeP4PZWqLwOaQKrDzU3Bf1lz1YJ7AzyBEx8hnNRqnBSzLfolgXKco4hsx1NI164wRNu872EwFQYC/KeIH9r2qu+6CbmuXJepDtOyrXG8sTqdQwbYJLSVUGSAVBkkjgGMf5109BX3ON9foc/VWRbSiSSAYBMH4oB5AP5Sa2mUwzN+jdQ8zIt3G3IfdhG7jIhs/aoyhFril/aXxtlGHDHrsd46bqxdtq47j8D3rp6e6N1anHqc6ceGWCTVxEKAKAKAKAKAKAKAKAKAKAKAKAKARduBQWYwAJJPYDk15JpLLPUsvCMh1bqdq9JF30xmIwvsMd+/OMdxXx2qtnqb3OS2W0fTx951tPTOrZrcpV1bBHAPpOXIGY7KPfH2z2mtGh0mlttzqZcKS2Xj/H7kfaVttajKmPFLPuQvQ3AQy3LgVY3PAyfZRPaPx+9c++GJ5gvTPh5+Zsmp4jLGZfIilGO6Tj4nO3gfsrz/AK+9WY22RpUlyY7e0p2ySDI3XTtkKvZef9Z968bSwlz6EFZmWGe6LT+YxFx1SRuckcKOFyeTn/i+VXU1RnLfZdDy+1wjlLJ5Y0huMVLKA3JIiLY45PLe3zPtVE2oZccvHLzPJ28EE2txsabexClDu9IMfDbHLc954+a+1exeMZ6fUk7EocUkN6i0VMqE/ctyIkd2+n4yBzmpSjw7Szjn6/yShJNbe8Xa03pLegi36UH77HE94zic/tVW5d5R333Z47MSxgji1GIUi2NzGfiY9uPnP3WrOLPV7/JE8dS+0OlS9ZNgWkVpFy5cYg95iYkZERxtDT8+nTdGzTuqCx58/ec2/NVqtk8+X395K9tM9pfNMAuYXacqAMHgfM/U1CfsuahGTlnyJfjq5ycWuhEt6xWO7c8KSPTkEmQQYEd5+tWyvqq7ngUw01k9/HzHRqw0qbbHtxEj7x/Cq5a6EeSZd/4+fVr5mf8AFeie9YVbVuLlttyic95A7ls8d63aST1Ccly6rKb96M1yjp5KMnz8tvc+WTS/0P8AXmcPp7k7gN0HkEQMg5GCPw+dT0marJVY2e6/cayMZ1RsXTY6dXTOaFAFAFAFAFAFAFAFAFAFAFAFAFAJuIGBBEgiCD3B7V41lYYTxujIeJ/DNlNM5sW9rKdxIJPp/a5PAH4VTVodO5JOJPU67UKDlGW5xvqXUtTZG3csuoaAASgM7ScelmWGg9mHFYtRoqIWbLkbdPqrbK1KT3GV6pqWUkR24Xg/L+dQhoq5dORfZrJx68y16Vd1DqSxVRMFSnYRJB3yJ+c1J6GiPMqettk8ovNKYUryD/hHvWaegqbT328w9VZKXEzxtKsGC3HuOPbIii0cPFlv46zyCSik+s4OAV7A4GaLRw8SL1k30QjpnU4kgumBAYxE5gEe05ryz2bGS5kJ6pzxlFlrup3LqopldnBBPtHHbitWph20VF7YIae3sZN4zkjaN3Ugh29xk4Me845rPXpVCXEmW26p2R4Wg1GoYNvLuZbcRznmef41CzRKyTeeZKGr4a+HBH/2g1xztdwS2w7gRPpmZPIjv9qhH2e4Y7x7HWrhxw+hOR3A9TFoyACZ/Dv96voqlWnFvJXfbGxppYMwfFb6G81oSykeoGDByBK8cAH3zUbfZ6sXFF/E9je2+98jT6DrukuWt4IDAElTJjIAiZnmYYdjmsP4KTsUOTbxj+P8m2d7UHNPKS+nj/j4Cf8Aa9o5GGMALiWY8AAyTOcfhSzRyhY4Rbkk8Z8j2q9Sqi5pLKzh9DT+GU1YvA+U1tWPrZwBKrwM+r5D/CuhodNfVZ14euTFrLKJReMN9DdV3DlBQBQBQBQBQBQBQBQHgagPaAKAKAKAKAidW/qLv/63/wCU1Ov869Su79OXozgnVOkXb94tGwG3bAPM7La25gEc7Zz71ktpc7ZZ23NVF0YUQ9DeeG7vTdNpVW+FUgsXd0bksYJfb7QM9gKujU4x5YRS742S2lksbnVuiXFKte0xVhBBeAQRkHPEVDhgizhn4Dmlfo4xbuacSZhbvJgDjd7AUcIPoO8iB1Hp4N5/KdVtwm1dob2LZJkzBHyrLfFQeEidb4uom9pFAJO0KASTt7ATx9qz5LME/o3TNJethm2knjgekgEGCJEg1rqqUo7lU5NPYsT4a0p/7r/hVnYQI9ozz/dXTdi34j/Cn4eI7RlT1zo1mx5UH4mI9TRmMRxJM8VVbUoxyicJ5eCp1GnZFLi2rryNrMScxgD5+1Z00yZGssXcqUe3tg98zIjPPv8AhXrWAjLdY8OJf1jbiygiZEdlHAjH396vq3j6Bz4R7pOkFkIlsk7rpkmJMbl9uPTxUabHKe5Cbyipu6HVXNTZuaZALtu5vDs5JfYQ4HrUgAH55J4xUp6uunexnnBJ8j6F6bcutbVr1sWrh+JFfeAfk0CR9q2cyknBq9B4ze1eA9Vq9AqgCgCgCgCgCgERXgFCvQe0AUAUB4aAjdRE2rn9xv8AlNSg+8vUhb+R+hzPS6cFSweNoggGcATETisVs5du0/8A6/cnSl+GT/4/sZsD0uM/A45/sGu4+TOJHmn5oyPTLIOnYsDIBg7ZGWwN3CwMZ+lcBt8aPqcPj8i18Mou8k/EASuM/CZz2itmn/Wj6Mw67j7KRrtFdbzFAJORhieJgnGZ2z962ax5pl99Tk6SOL44+9i+1oO7Fy6JSIUSJmd0nIMY+lfPw5o+glyZmxqGc7HllJ2kHIIJ4r6dpPbB8zFuK4k3kxXRrZZD62BUE/GRgD6/OuDZNqR9Om9kSOjG7cYg3buBIi4w4AJ7/OpyeMPzPJycW0kba3fddi8hWG0MN0RwZaTI9+a7fYwezisHzP4izGeJ5NHpvMNlTbG1jHpcQPi9XwjEiSPqJr5m1JTa8z6Wt5gn5EXX22LsGI2wOJBnv9oj+NeJkiv6R04C+26GGw7T7e/0rVU8xfoVTK3w6oI05jPmvn7M3/VVGm/UfoJciJoOlay5esjT37Vshz8SMZJOZg8QB8+c1KVNVvdmsnuZJZR3DTIwRQ5BYKAxAgExkgdhPauhjBQORQBFAEUARQHor0HtAFAFAFAFAFAFAFAFAFAMa/8Aqrn9xvyNex5ohZ+V+hzTS3ERHmATJxy3p+nNYdR/7En5/uWaZZ08V/x/Yqk6PdNtrq2rzLtJjyyCQy9geee012fxFbTaOUtJdlJpfEwmn6Lq0t7Wt3wOdptsADyRBX3rk52/L7+p9F2a7Tj4i26XeZDbtMjIPUJIOSwIAiJyxH8K0UTSmsmTWaeUq5OO/wDs1ek0727ilkJyMAZywkwRwBJ+1atXODqksrkcnS12K6LcXjPgahyIPP4H/Cvn480d58jKWk2mTAEiTI9/rX1mY88nymJYxhnPdJecIyhbcE4JEtBImDwMSf8AvXClGDeW3n5H1XDblY5bFh0prYHqCl5EbhgCAPpPJ+tex4Wkme3Kzdrka3y3LDkQwP2mu7jc+Ucu77jSaa1s0qzLNt5UHd6jiIzwa+Wt3sl6n1FX5I+iGOlm3aun9I33AAuXYtMntnAAMkk5iIESZxnWlmQlxIk6/XW7jf8A04KL5Tk7h/ZwFnK9jg/UVoqthNZitipp4MX4S011Wtl3BXzGgAnnZzxU1dRJ4rjhlMIWJ5m8olafUsFZ7F9EdSeSJDT2JDKuJ+IGo0057zZ0IwUo8yV0Xq/VbzaMJ1VD+lJfaX01qbZsR6SFOdwaeREHmrfeUy4U33ST4f671m82hnVacrq7Vy9BtAFBaKgrI5Y7uYxnBjJ5xsRfCsrA1Z/pD1xuaZmFlbOoTzQlyVKrgAm6DtCEFiDtmUZY4JzTjPhw5b5I7N4jHIzqv6Vtbu3W7emFtgCFfzC6YyGYbVYzJ9OIxM1OM5Rik3lmhadPnsT/AA//AEl6vVai3p7dmwzuT3cAADcTMngAmrFOTfIjOmEVnJ1YVaZgoAoAoAoAoAoAoAoAoAoBnVn9W/8AdP5V7F5aIz/KzmmiUEOD6gcRt4xmGA7/AMIrn6t4vl6lmj/Qh6Iv7HiOxp7Vu2UuwihJEH4FA53g9uTVsL44wycq2ON4z0oGXdO53A8fZ8VNXRI8DPU8Z6KQPPbInCXCPx9QqxSTI4M/qes2TecrfIDSR6ZmHn9oTG3H3rLqINtNItraR7q+tKTtRGuKVMsp2x2jIn7iqa6JS57E5TSNJ0X9HXTWx+rEqAyuyljiPUxaWMdzW6EOFYKJPLyN2/DnTWGLGlHyCr/0vXvBHwJdrPxB/BHTmH/29s/3S4/5XpwR8D3tp+JX+INDasG1atWVCgKIBMxJWdzZMc8yajdbOMdpNFUaoSllxTFfpyXtOlm3KXWAt7ZBVYIcvOJby5YAGDIGRmsVuor7LD3f7luN8ozPV7TpqQrH0tbDJ6YODtYEMPeK5OslmCl4PDOv7PcZcUGU3Ueo3dOd1oKd3oYFf38DCkSZ+dW+zE25T8ET9oKEYqHL/A1otXqrTQLSMU/WfEMhlYfv5MW2wM4PyrdVbXHvp+X0/lHLara5spf9ppctbLdm2GaGe4UFw3AvY+YCAMLhYnaOatfdeW/In2MOZoOoePBcFtv0a0LtreLd3uBcQ22EBRyG94kAxSiEoS2YdK5tmTXq7KtlEJAsqyWiMFVuSzjcIJ3SZnsY4rRu+ZPudERRdc8YGOPaM15hHuWzwWSeTOKZCiX/AIH1SafX6e6Z2h4JE8OpTtz8QMfKpRluRshmLPpCtBzwoAoAoAoAoAoAoAoAoBLiQajJZWAc66vrLVjUnbeZFCvadlbcA7FGEgf2gVJJ9JYA/EK5Uap1vhUuqKrL6+N56Ii6EcnPPYMfy4q/Wfry9TRov0Ieh5qbigwVcyJwjMOYyexzx9aoWTTgdvdMtsrKQslSOBiRH86Kb5hoqR4VZTi5KhcDbmR8wPatMdV4oqdY3dItOiXNN5hgt/VqYHB+IjnjHvV8buJZiiPZ74bwRepeKNgQWrZMmNryABHaDziKqeqi846F/wCEl1ZVp124JLDdhv2vdgRyOwEV5+K8j16XzISanU3WIVQeWA2qMT7gieakrnJ90i6YxXeN/rNBpP0RFHl+YApIC5DyBcYsDww3DP8ALHPnK9Tct34ryK2tti36V0a0LO+TCbhO8jy1VZWf3hxkScj51dp1GyuU3L/BDiw9jPdEtXy117MtBJXABQiQFBgSIUQDJknJrDZRObxFNY8OW3v5r5+AexYXukWL1g6vV3Sb9oOXfeym3siE8tMOkgSCM7vnXSojCVOX8z2FkovujWpHT101lkZPMuC2basQb3mMpZt4narAdyIDAD2qvVxj+Hl2fvx8846CUpye7yQk0tq9aZil63buuFvuBDWyHVSHLEwu3E5UKS05BrFVC7jbUU0ltzxj/j4v5nibyim/pL6XpdN5Js7Ld1jBW2VgpHpdgIO9pHqPP2rVVO2xtTWUaqX0MdAJIz6ec/2twrVFYk2aHuhC2wOB/qIqbZHhPTd+VQcyagefpCzHf2mvc+R40l1HG1TWtQqAeoeW6sQYO5VdDBEkQwqUu7HiK1Lik4+4+gz440gncbi7RLbrbCAeCfaql7SofiVf+Pu6Y+JIHi7R97wUgAkMrAgHgmRgfOpr2hR4/JkfwN3h80Pp4l0h4vpxPPb3+lSWuo/+vqRekuX9paIwIBGQcitSed0ZmsbCq9AUAUBH1usS0he4dqjk1VbdCqPHN7E6q5WS4Yrcpb/ipf8Ay7F65/6do4nk1zbPa9aeIxb+X+fkbY+z2/zTS+ZXP4n1DEQluyp/aYliMTwMH5+2azT9qXS/Il9f4+ho/AVRWW2/kR72ouvuW7q7qmCQbSgJG2YOJGe8xVcNU7ovtJtP5fLf9iUa4rEq4Jrz5/F7FF1bo4a2hVF2q5a6CzFmlp7HdJcyPqeScS0+sipxhbyzz++f19Tna/2crXxV7S6eD8vD9vQidNv3AznyzkT6nCHkxAM4Oc/L510tRdVdNzreUyvS1WVVqFi3RdXdUifETniR/wDEVmSbNIaXy7pL7cgbZIzEzGPnRprY8H7gYtIu7REbdqnMzMnPGKJ+R4K1eiW4dx5Agfn7VKE3HkGslT1Twwl1gwG0qDAUxJPcwnNXKyElia+B4uKLzFlLr/CrbV2E78b9x9MQZj0e/vU5U18PcfzPY3yz3uRe9D6AtgElizOq7gYgETMEDIk9/YVWrFD8j36ibc+Y9q7MxtjntERM+2f86zzhx82QaITJIlgQRyIwPuCDGCO0/asMtPPfgWPfuytxZdeFLZWzccIHVnJgx6NgLKTLSRu/l2zWqnVWV7PfHMYytyl6p4fdZ1Lqr3JLPaQhdxuxtG5yARAOZOBGYr3WUzguLKSb89nnO3r8jxNciD4o6ro/0ArsYamIW0ELMl0XN3mC4y5UMmYwRCjtXulrllYe3XosY8M9SyLxsR+geN7lnS+Vd0wa4JNoi4UA3zuDLJIgGQB/wxNdKrhrjwo8cY52ZjND0m4RtUbiFJxGQilj+CqfwoaVZF8z18CoZL8G48Hf0d/plpNRc1Gy00jaikv6SVIJcQpBB7MKtjXxLOTNZfwPhxudI6J4J0Olg27Cs4/buetvsWwv/pAq2NcVyMsrpy5s4L1rpNtOsPpkTZb/AEhLYUOzelisnc2ZM7vlMSYkwsSyX0ybT8kaHr3RVTqmo2ArZ0y2USZPw6a3tG7JnjPMxVN+qrpkozhxZ6eR7Xp7NRBuM+F+Jd6C1uYLe9L/ANZc3XCpgD0pBEjgfgc5zwLrKo2OSh3c7JL5nRSshTGPFl43ZIujcVLHF0zAYEi2OFM/UDvyc1Ra4qbaWyNVLfBjqT9NcseXceX8x4VAygqRMBcSTySfl9M7NLTp7IuG/Fz8jJqp3Qak8cPI6HorQW2iiSFUAE84EV9JBYikcSTy8j1SPAoAoCl8W2EbTNvuG2FIYNIEGYEzgjPFZdXXCdfe6FtV/YPiz5blHptcLY/+uZOFG9Cww07WcECJiBkwZE8GuPCquTaks+fp9TRO3OODY9VrbkXLe22G+Fh6g/y7bW2gYOeM4zlvkspxj/Hw/wBM1rtIxxPf6r/HxRE1twsR6i4BweIJzE4JMQOZ+uaT086H3o4zvv19PvPqT01lVibrefHD+8ffIQloqBGwg4gZM+3AM7m9u+VzVKnnb7+/touck+ezX39/Ua1V+3tIW9tIiRcOVnAiOVO09iPpitEIJTi69s/T1M1stnx+5r+Pv3knw7c0nkD9IvAvPxPc2kiBEgED37V36qU47o5srN9mXFvQ6NspdUz7Oh/lUnp4DtJDrdGQ8O38D+QqP4WHix2rKrqVsW7mwNwAZJjmccEVntqUHhE4SckZvT+Ibrau9pzZBtW9oN1XHp3LIkEZn5cRR1xUFLO44nnBrOh9HQ2/6y5iFy+7CjB9QJJM5PeBVlVUbI5ZGc3F4RPfoo/fP4VP8LHxI9qxi50Pj1j7r/nXn4XzPe1K66RpFi7LliWQ28fAJ2tJ4z/E1m1Olf5snqlky1jRXb6HYu0FlBltoMtu28g7gD37jmubJ8M85z97eTI4beUVXiDrmovoNPfbfaB+EgZgkgtjMQIn/OuvVbKVa3JRWNyo0unlgqEJGYC/5ir64ZW55J4H71vSo0XHDXBkKTJHz2DH3P41fGHRIrlLCyy18AD/AMQ04JnL/f8AVP2qqH5icnsUPjbpq6bWaixa/q7bKVk5ANtbkfQFoHyA+tVzSTaN1Um4JnevDHSU0umt2ULMqgmWiSXJc8ADljWqMeFYRz5ycpZZL6mt42mGnZFux6GuKWUGe6qQTie9SIHziuhvp1Oy1+4ty42rtFmC/EblxXmTkwGjPHAwKx1amF6TS+08GquMo5XkbTxl1a5p9TdNwek3t3mBfT8PoUwewAHEyvtzk1FSsm3HHETpuUFwy5MpNT4pF12a6R6yJkH4RgKfliI5yaxWaSxvK6GynXUqHDBlt03xPaLuhKhLhCMTyFiIkj4cnPaflVEPZzlZFTyl4o9s1VdkOOMu8i+1F2291DbK7FG0QQfXzAgQQFB/E+1dTS6KvTym4NvK69PEwWXznFJ+J0m3wPpXWjyMgqvQFAFAUPjXpI1OldN21hDoZ4YcT8oJrNq5RjU2yq6jto8JyzqGp111reguFXCREYL7VkHeTkQZBx2Nc5cC76M39XKpl4Llz9+eZM6QNRo7lxvMWFUFrLQT6smCPTtiIAn7RUJV1z/T5/L3nX0+oil2DeeH4okt4k3NcItCSgVVImGmSPkuIgziY5q6ntOylXZuuie6T8upbONULI2Q/N1a2ePPzKbztS3Le3Jjg7hhe8nv/IVTHSx6sus1WdkiDqLBQM24nkwP4fh/h7VqhVCOMIzTslLmyH08s10BpKl4ZeQfV3HtX0Md9mfOzWFlGT0OmTYd20ED0k4JgDA9zNcabfFsfSLib8i48Ojc8F2wCdu8iecQDntV1STsivvkZtVOca5YXy8zc2eoXvgR1VjABZTAMgZAPGa26mqvs22uRydNdb2sVxPdmf0tnV2r9y495W37g42EhhvzgQZBXGcCPeK4v4mufcSex2VGS3OpeHdDZGiubUXG+CRJBFscEyRH1rVpXlb+JVfyfoZq71HyiAbrrIJEM3A5445rtzhXFZaPn67b5PEW/iLs9cuNIS/cJXn1Nj7NVarqksxRZK/UQeJM0Hi+xtOnA3vLNMsPSNoz6vyrkaj8p3aipv8AVho7foVH3MGdWBIXbklT++MQYiQM9xyZ99vO2xbLbcpvGlzRkLcsl/NLQ6QxGdxmSI3SIMGKs0rk1joEzC9R1VwKwypicYPE8jMfKu1TXHs8mOdku2S6FJ0pj5l2fb+dSp5slrN4o6Z/R6gPUtOciN+Dx/VNmPfNZovvFz/KV/8ASWf/ABDV/Vf/AOKCqrPzM3Ufpo79pxCqPkPyrYjnM9vISpAJUkEAjkT3HzFDw+cr2iNnrVuybr3fL1lkbnjc264hJMd81n4YxeEsGqtPhb8mXv8ASBr2uau9pEsiEdV3KJa4I3qIE8M3PML+OWdMa5OWTJdLupZafkV+m61Zt6VtK9m55o344Vw4wHkhgRIggcKKpcW58aZRHU9nDE1h+mxW9B6Rdu3ERFILgspYGIXnIBkdvqRUp2pJszwVlknwr0fTPv6HR+n6ZlFsMykEqSVUgNIHqGSSOfardPNTUn5HVzlLJ00V0EVHtegKAKAjdRfbbZpiBMxMfbvVN8Iyg8nseZzC014aoaqIbuoEqVjbt+Qz/CuZ2cOHhJSoTtVmeQ9qtty41wqBuRUC7TtVRnaBxG4k17CPCixQSlxdSvaxBI4Hy/wFTyTPHTuT8oH1+lECv6goggexqxEWVq6lLdjcLTeZulrxWdvqkBVIImJz7xINabJXSs41PEVyS/f3maCprqalDL659em/gPdQ8OF9CdRprV9F7rCbbihgN0CIMLPpEH2PfFC2ascZpNePgbk65qMovHkZzo+oQbUgBpYljGQQcT27V0aJR44r75Mz62qfZya5f5NTYBDDBAx7kD1D3rfqF/Sl6HGoku1j6jA6SbdxXfVM2TKkAbp7kjkfhmuInFraJ3OFrqdJ8KMP0O7BBBL8Z/8ALWtOm5e8pv5P0MhrLO5lxI2sOJ5j/Cu5KKksM+Zrm4PKEabT7FPucnEdv5CvIwUI4R7ZY5yyzd+J43Wfq/8AyiuDqvy+8+np/YwvUW3XCDJA/ZwADP8AdkkQO8Vw9ZZKDXgdbTaau+DTW6KrVZVgDkbYkz7+wFaNC3JZfIr1lcK2oxRlOt/Dcznbzx2rv0fonDs/9he4ruj6QFWaSCeWYgA8tAHfj+PacxVkYo12Rzj1N50PWXvPtHRLYXUIjMnmElGAtsTu2MTuKExxmAahxRk1hFlji1sih6p1K7qXbUXwi3Lyq7BJ2gMi7Ykk/DB55mqLF3maaf01g6Np/wCk/Xwu7pBYNp/0pdmoXNjHrjaYGRjn5VqMDUfEkp/S3EeZ0zWCbX6QNqh/1Rj9Z29GRJ7UI4OaajrVu71Ya3a6W21Fu6VZfWFUqcqDzCzzVEpd7JsisV+4vdb1i1/tC5r7QD23YyrCN42hMHt8PI7fI1Teu02KYrCKvqX68m4qQsBVUNLQPdjE/U9oHaq4VqKwVWaeux5ktzYa3VXfKs37a+TcKpcJVmIIHpBEiCx3CR9OayQUVNxZayZ0fVXbkPcJLm7luOFEYEZwPzrbTFRUsCXQ6iK6BQe0AUAUBF6os2bg/smqrv036Eo80YbqDpbIRiPW2wRmGADQe4MZniO9ciFik9i12JSUX1EsoCGIgD94/lxVhYUzqJO1InJPAY/9X39xUjwiX9cEWTzuKiB7dsVdVXxyxnBGU+FZKjWXp4MAggTM7pzI5mrbKnB459clVdqmslB4iPmmygaCHFsMRhQ+Jg9g0VPbgLK33mnyOtanrdl7BS2W8uyAGmQdikZAjOAR85rJCqyE48a2ZXC+qfFwPLjzSKrrPXOnWiqstm+S0MFRHKDOTj3HHP8ACtspxiWVwlNZTE61ka41xbYuWwJW5bVYHtwZkg9/Y1muuTlwKW/gShS0stENdEjRvcXPSNvqGfn6YmapUn0JGy8O2gulvBRGX/HyxW3Sttb+Jnv5P0Mdq9ayFQqbpBJzERHyzzXebaPl4pPmMXdQ7qYUqYIicGe/2qqxORfVKMOe5u/Fbeqz9X/5RXE1P5T6Koy/WLTEAou5sAAtHfOTPaudOiu3Cmbqr51Z4OpSanTFQWZNpxyZOf4DtV1dahHEeRXZbKx8UuZD0PSbTMWdZBIwRgH/AL1tplNrC5FDpz3ktyF4609pLlnygoHqVtvEgiJPc895xUNQm0ngto8ymTXtaG9ElkaVI4MiCCO8fSq9NPh68ydvEpZivtir2sa6DdcbWbJHsatseZZLa3mI/p/G4Xbl129JbQjJP6wkwY9o2/6FaTm8LLi14ssNpjcGoIvJ0r9D8oqOY5B7neFOOAPnilynxpY28Q8Jblf4g0/T7enS7pbrfpCwtyw53AnbBaQBtyJ5jOAMVmrnPixJbeJprk5w8sCtBrkvWrUkTsRTEiCqAd8dqnZJKbIqL4c9CfY0e5SFIBC7txEwAcnAnE/aaqnPh5kJb91Pcc8N9UueYtvU3nbTjcsLLBWJABjuojvj5d6z2OP9vM9qo1HOS2+8Gy6PcVtnlkMpuQXHpE4BwcgYn2zWnTp8Es8zxtPDOn10Sk9oDya8ATQGb8U9etLZu2repsLfEDaziRkbhA+FisgT3iqLrYKLTaJ9jbKOYI5lqPEOr1BUuN/kp6tgwGmGfcuR6fcxz8zXNioRe3UxfibONxS3W2Mcn1+Roeii5qUNwOdvpUqqh9rHuTyBnPMCDXllnZvDR0oNuKcuZEsvZZvLF194HLJyRE4BB7j5c1Yp+RVG+M5uC5jes6CzfDftgBiwDKQZPzzV9U61+dP3YPbIzf5Me8jjw0pM37wM5AtLJ9uTgce1bJ6+uMVGuGceJljo7JS4pyxnwHTptNa/q7Cl+Q1w7m/vAHA+1Yp3Tse/y2NkKow5fMydvrunZSNQGEKY27wzTMqREcEwcD3muvbxSiuFZwcTQ6Ts7Jys2yvjkoLl7f695Y9yTun79z2rnyb4nxH0dUIQgow5LwNBp9fd0oUbXW3cUETK7pUZEiG71kjVG6Xe59D1ysrjnxIWs63bcr5qKxtkrttCCfeexAI7HvWxKNe+TPwykdM/o2v230F/ykZAHdfVEk+SmcEjuKurkpNNFV0XFNPwKe9YJZSIwCPxj/Cu2fLINhAM14+R6azxvfFryGbjcy/cgRXz+oi2tj6qo571brbX/MshP1e4Q6n1AKQ0jkTOO1Y1KNbTec+41qqU1sR+o9QtogVWuDE+oc549pIHNaY6quW2Ct6WcSvs69ktuGZlV5IHvyPr7D71J2uPLkRXGk4rmQk6te2nSFEe1eeArictxsM+gqW54kz2qVd3cwiqNltdajOOPDPiTLPSHtF0VReZW2D9wCNpYnmZn8BGalHT4hxzjlmO3XuV3YwsUUlu8b58FnYrL9shjbA9RIUAe5IgD7mB9qpnJbvkdmlYrW+fP/Rp9f8A0fLZG+86sRt3KiyVWQOd6juBgYkYNYK/asbW1CPTZ52KezeOZH6t4Rs2dt23c821AMkgFP3g4iVETB7wQY7qtbZdBxcWpfJ+h7GmEpYn+XqUekt27GoZriMbTH0w3xCP3oPf3H+NXS4pVxz7+hohwQk4x5dOpbJoL7bhZtolp/UpbZuMT6QSJmMx6RxUVHCzJkbLIvMcbCtBrQqMRee3qBKgbQOeQTuHcnBEVB8Tl47klVUoZ25c+pG6Dd9A/wBdqru2k0aqnsdC8M2wPLtj4t2+Pk0Z+kg/hXRqi1F58jkTwnt5nUlNbCgVNAeUPTwUBwrqjk3rqn4muuD/AHt5n8q+fsTdj9TsfiYV14fRJ+4e8M6q6tgspsRIuBbjkMCBIIAcdj/KvJpt48CuNFcpOeW8vpyDrXicBUGiu3kuHFwkABQQQVB4+KCOYkmRNXVVNrilyOVrM1rK2w8bCvAdu3vuC9cQXNoZC5MNyX7wTEZNe2uaS4fvwM+hku8m/vxz1yW2ivl3uetwFchYgqyB5VoKyZHpnGPxqUU1FZ5m6lSSxJ53fw6FiNpPqkfQf/KhcRn1SiSiAEdz6m+x4pg8MR4+tXbhtuA7hN25oJCztiSMLma6egmo5TZm1EW8MzPTOgXXM+VdCkYYJyZxEjP2q7XTUIrKGljmWzRrrXgx3t7dVcwI2iR6e+RM/YRFcxOMd4m2Vjbwx3TeB7C7YusTjAgye/7P3qxQdjeNvV4K5X8G7R0fw/0XS6Wz5W8SSS53um4nHCtHwwOMxWqiGI93cz3WcT7xJbw7pXHokf3LpP8AzyK1dtYupk/C0y34RlvB1o/+Ze+5tH8lBr38TMg9DT0RF8XdSS2UFxxg9lIiQcEbie3tXN1Uko7nTog5PCOc9XuhrrOMq3wmIkAdjzFcqyWWdSqDUcFLrdM907Laln7Be/J/a4x9OKsp5nlvIk6bot5l2bfWpO1pJUH2MA4nHerJSfHwvl6Fa4FDjWM+pY3emai7ctrqyA4VnBkEKiQpO4Rkm5gewM84vrik2856GPUTUo4a2W/wFabTksCynawcqwAxsaGMe/q3d8Bu8V03YuLs84/k+dVDlB6pxzltuPjH+Ut0VfiLS2/N9d1hDbAWE7gDPM45j5V5KCklKx4fJrxwX6bUW1OdOnipJ95NPGOLxyWerQMQVUMHEjlsbQJHfHy5BQ96quhTXDuwWH9f2K9OtVbZ+o+0g910x4/U0VnpSi1b8u/cIgMNp9LYnBiQDM5JifnXBhOztOBxefcd6FijFR4SdZdOXG2M/ECCPnz9a6MqZroFJMOpXk8sqsBj8LG3IPvAn589qq7J4zk9UlndFXoukksh3WWIH7Vsbs8rIOfyx9q8XaLfJc5VtYS+ZZ39Fbsy4sWzu4KLBJyGBEwQSIJxyT2qvsnOWU2Qz0zg0HSOk7rqXymwgRxBI7D5D88fbp0VqMd18fvoZZybfPY1oNaCsVQDWs1AtqWMwPaqNReqK3NrPoelJ/vCWJFtQCDGTJmJxx2NU6bV9tV2klwr7++R6lkyP+6K3LrFLpDAyyjaSN0xnt9M/WsVnZqWY5LtQndBRk8Y6rn9sg6/wdpbBXzHZd4jb5vDHO4gmTkxiRxwK9jOE5LOEXV8cYcMFsh5dBo7Q2XV8wjPwn0iOTsHt9PpWi/ggvze7BXGuVyxw5XmNr0nQXXH6MpBXMKGx93iPqT3rHp5znbxcS4VzXiRu0kq3lLDLW10m2hhTPAjesgfwNbnOqUXth/L6fuRUbE+eV8/qTLHSncSmUPeQf8AqM1Tmvgy33vDBJuXFhLbx/wQX6HeV4gtGewBHzM894Bmo8ccE/QnHT3lAHpMcKqnGeA0j65iowqpnN9pNxXljb1Kr1ZjMPgSlV1WXJBPb0yf4marhVwtx4+LzfIlXyyyFcRCZNsFuxb4jA9/86311SguJSwRnwz7slsQ7VzUiCumt5MRuG5Y7swG0g44JrFOyyTyzXCqmKwnj3FhodHfYbruwt/YUggRiWPP+ua9hZOMeFv4ELI1OWYr4irPUrVuQFUkHJKieeJGatm7LN5Nv3lMYQjyQpdaSNwJziFUgD6ECD/Gs3BrMvgkiMslTf8ADJulmLXCxaS7g8HJj0gN9R/Cor+oszbybK9TwrZD93pyMFQncFwCSrEicgiB9MDvWlRlGOcbFPapyeHv5EK6NGlzy0tK1wZi3b3ERmfSMxVLnFM0RjY1nO3mxWivm6G8oz2g2mj/ANxkLHt+VXdtGa3RTKl18xF/oe6LgdVddwDCThsFTkEiYx7ge0VdC/G2CqUMjNvoeoLqSx9IZVC8DdySTDRgCAPx5qxyg4OSe/h1KcyU1Hh28ehS9R8Oas3Nq2bLqMC4y7oWB/8AkIE4iBPA5rU9bBwTeM+By6/ZsoXSinJRe7aeF5L3Dd3pWst7C9lmA7W1n4eIW2IUxAz7dwKy3X9rDhykjp6PSV0W9ru5cstl/wCFbD+WFa3cBAyziIYyxUAwSoJMfLtWWVik9jY6+Fcy9/QMerv22jB+Qn+deRluRwRTo7Y+NYIzGTOcNz8ifx9q0tcPeW69f4Kst7cmKuadrm3agNwboX35A/kc8fKpcNbzwJ89guJY4mjTdH6JtVTdALAD5gH+Zmtay+aXuKWknsXYtipYPBdegKAjdQtF0Kjk/OvM46ZPGs9TE63SaoehdOVAYEXP6wRO5htHqBbImcEzWeO8v08eaeV8C3GI548+WN/iO9N06oSWe6lxmLNAhTjaBB9UbYPPxVRZCyM+NxUkunIZ4lhPBC1fTN15mtLtfcuy8zbgfSJLIeO6+/evZaaVyd6h7kThquyj2UmWHmMltvOu2nZBLBDMKePQfUSQD9e1Y8Si1GUWn6FnaRlvEq9Y9y5uWyIQDkDaN5wZGCYBBng/WrFFR5oZyLv2ththkBVVJfYrSSAByPmZyZx9anGEpZcUyLlFcyTa1YKgWbX6tl3ElgCA0/sk75+RivIJKa4mevdCkUgbCzDd3bGfliCcTBBrRd2T3e78iuHETk0J2hgyYwScYn2E5ntNfP26VTnwylIk4+Y211EkGZPJif4DtXY0mgtsjiHJdWQs1EKdpM8TUcGS891aAPy/hNS/CWcWJLBPtYtZR7+nNuIS2Z53GYP3Hf6mflVi0cP77Eii3UTi8Qg5ANZcyWLIByW3RxVV1NUF3JqXoe6e2y14lDBLt2PMUsgDq+S24ENiOZJOBH2rPxpGlrDwyFZ0T22KWoBjcwEkicDkERg8kccVqpsocWro581zM9sbMp1y+I7+kX2ZRuO3Mv2xiDDAzPtHH4ysjpOzzHPF4M8h2/FiWMCL2mUGFVFYzDFAfqcEGs/azceFt48C9VQUuJLfxGhYdVzs3HuEyfryCay2uxPNaT9ScnLoIuSFy0PxyBn8CR/Oow1dif6TefeVybF3NYoTcRcMdgoLH7R/Kt7onw8WPd1JRkpPBATrdvyvMh9s7QDbiO0T8P3/AIVnc0uZoVMs4WDzpviFGaJW28gKIOflMR7/AI14pwk8ITonFZZoNZeuMm2QGIOFOSPlOfy+tTr4IzzKOV8PoZJxk44i8Mreo9Md1hrvpAklSVIgdxthh9eOa2WWaacWlBp+pRRHV1zTc016FRrNBaQobV11IZVYhy27c0CcxM/Qc4rFCnMlvjfxOo75YeVnYuNL0N7rbw5BI2lp+GMekHEzJz/33QqxJxW68f4MTtyllGt0HTktD0jJ5Y5J+/8AKtcIKKwilybZMqZ4FAFAFAFAFAFANPp0PKqfqBTOBghajoOmcy1pZwZEg444PbtR7vLC25DLeHrXZnH3H8xUXFNYZ6mwToxE+tW+qH8w38qoVEo/pzcT2TUvzIh63o+oJXyvKUAndLMdwjH7OM/OqI6OSbzLPuJ9oVY8NXRtDh7kEuZZWXeTMgMdwAJO0dhW+Ono59Sl2WEO/o7gP6O+nvCyT8aSMTvncuU9XzrDfBqTUIej6fA1Q3gpOSz4A3TLVvfF26wYSfNubysSfT7VXTbqKo8KbRGyELHxSSGrWqtSgsoSrLuO307RErKtB9WRjiM1ZGVzT3DUEOdN077V3EQS7FZMgMSVUgz6gDBzEzFZdTU7I8LyvM9wmsIR1TrFm2t2yHU3tsLaON7OvoXPpYsYA+sU0uhrhVhTSfoIuUHtFteIrw9pbtourmFwVCrtUlpnlBkQOPcVXGDjzZqtsjPkhy9f2AG9+rDPsDSpEs0J92wOOTXSjelDC3ZicN9yfaNuCUMgSDmMjmSozWKcpSeWXJYQ3pdWGAZZCx8LTPyJM+3/AHrlajWWVz4FH3+JBzwyKX89iVvIbYPAzDYgY+Lmcn8e23TWznHM4YfqSi2yTZ0rgmXEdo9Mz7kr/CtHElukSayITTvu/eHOBH5mD9Irq1aim2rFkuF+S/fc59kLoTzBcS82WOg3sY8knsXLARHyP8qwaqumGOzs4vd+5fVbZL88cDWsW4jDEEkDdtkH3EgmPuR9DVdMYS3ky6UnyQ1qNQB8Utx6VAPfngz+WDVs6IuPFW9jyMnnDGSy3YG5lETgTKhhKxxLcD5TxWdScGsLLJy5Fj0zw4sAMu1QdwXvMzJPbP8AoVujpUnl7lLuk0aazaCgAcCtSWCoXXoCgCgCgCgCgCgCgCgCgCgCgCgCgCgPGUHkTQEe5oLRmbaZ59I/OgIw6HYBkKQf77fkTFRlFSWGeptchF3ods9z8pg/yql6asmrZEHV+HLjEFNQVgERswZ7mTyKj+Fie9qzP2vBusskG1ctXILNDAiS5ljHGSZiYFQhTdXLig0/VFsrKZx4ZJr0LTTdO1Gw+baVWMz5cEGe+DM1dxSa79cW/IocYp9yTx5kc9CRGRgrE2wVQ7WG0H5Ng1jlxSWODHzJxa6sg67zFV93l7Q24PBLqOS8R6nB4j5V5wLDW6ZYpYeegxa1bpchtbbI2/A1sKTu+Ft09oP1n5Uoqg01ZNJ9MkrZt/pwfmXI1M2QUuB70CRI2E43cSQOY57VRJNWNbNZ5ni4sZaIy6u8t4yoW2ExBnc0+wEiAI+9Wxqc45ieOST3G7Ood1D77ZJ59U7WiCsdiDgiuhGzSQhwyreUvvcxOrUOeVPYiWF1V+4CloSjOPUSA2SgbInaq5nv2rDHtJdyK25nQxWlxSe5t+m9IFv1Mdz+/YfQfzroRqjHkjI5NlpVhEKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKAKARctK3xKD9RNAQNZ0HTXfjsofmBB/FYNQlXGX5lklGco/leCAvgvRhgyIysOCHYx/7iRVcdNVGXEluWSvskuFvYmWOiqsw26f31B/ICl1CseeJr0K1LBDXwyoOPLAJJMJByZP3NaouCxmKyupS4y8S40WiS0u1BA/P61DzLCTQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQBQH//2Q==

Wolf, Funny how gwac never said that back in the 1990’s. Now it’s not allowed to happen. Nothing worse than an angry homeowner watching the bubble pop. 😉

“It is in no ones interest to see this continue to unravel further.”

I don’t mind. Hardworking young people on the sidelines may not mind either. While it may get unpleasant for some, the impact on irresponsible ‘investors’ and over-extenders will be much greater. Many others have less to lose. Like I said before, looking forward to enjoying some of the wealth that you give back. Pass the popcorn and start the show.

Of coarse the world is flat. Anyone with an atlas knows that.

I would agree with you, because a chimp would be better at predicting the market than anyone.

A chimp would make a random guess. A human would also make a random guess, except they’d be convinced that they know what they’re talking about.

Mind you with that ignorance recognized, I do happen to think there’s something to what your learned friend is arguing.

And Hawk, regarding Gwac’s OCD – it’s “CDO”. That way, the letters are arranged precisely and in alphabetical order…as they should be.

Hawk if zerohedge said they were junk than they must be junk. 🙂

“Only a blind(and ignorant) person could not see this coming, just look at every god damn chart”

Market advice coming from you. A chimp would be better at predicting the market than you.

Another pretty graph from Hawk. Lucky us. Hopefully he posts it daily.

Local, this how bubbles pop. Shit credit pumped into the system for years and years finally comes home to roost. Credit squeezes for lenders to pull back lending and tighten like a vice.

Only a blind(and ignorant) person could not see this coming, just look at every god damn chart.

“Do not be surprised if a consortium of the banks puts something together to buy the loans.”

Zerohedge just said no one wants them. They’re junk. Just like Mike’s charts from the flatheads society.

“As we reported over the weekend, while Home Capital hired investment bankers for a possible sale, there is little to no interest in the loan book as the company itself.”

What I wonder is if the two sectors of the company are related, despite what some may claim. I would think they would be.

People may keep paying their mortgages, but I don’t know if that’s the issue. It’s the people that want a new mortgage – if everyone on the savings/investment side is drawing out their capital, how is HCG going to fund new mortgage loans?

“When people have to find alternate financing we might start discovering exactly what percentage of their mortgages are actually junk.”

Agree Barrister – we still don’t know what % are bad mortgages. The OSC said on April 19 that Home Capital had been “misleading …”

http://www.osc.gov.on.ca/documents/en/Proceedings-SOA/soa_20170419_home-capital.pdf

“HCG’s residential mortgage business consists predominantly of two portfolios: (1) the Accelerator mortgages, which are mostly insured by Canada Mortgage and Housing Corporation; and (2) the Classic mortgages, which are not insured.”

Also news today UBS had to pay $500M settlement for selling toxic mortgage securities in 2007

https://www.thestreet.com/story/14112398/1/ubs-pays-445-million-to-settle-toxic-mortgage-sales-claims.html

I wasn’t trying to be sarcastic. If you don’t believe the earth is flat you’ve swallowed the kool aid.

Local

There is no positive spin to this. Bay street needs to put on their big boy pants and deal with this before it gets larger. If this was the loan side, I would be heading into my bunker.

Me neither, but it will be very interesting to watch this unfold both specifically, and any effects it has on the wider market. I don’t think it’s broadly a good sign in any case, though.

Michael,

I always suspected that Lenovo monitors were junk, but this is just ridiculous. My apologies, I’m trying to find the image re-calibrate setting, because my made-in-Ganzhou screen makes it look like you just made a bearish statement.

BTW, I wouldn’t call post 01 + a few years a “rough patch”. That’s showing strong, but unbubbly gains.

I’m assuming that the big banks would buy the loan portfolio at a discount. That would make them more attractive.

And can’t they also buy insurance on the portfolio from CMHC?

Local the banks helped out equitable this morning. How it is put together I have no idea but I am would not be surprised to see them be part of this. Anyways something has to happen quickly before the GIC come due. It is in no ones interest to see this continue to unravel further.

I don’t. If you had looked at my ‘We are here?’ guesstimate below (made a couple months ago), you’d clearly see that I think Vic/Van are about to hit an extended rough patch 🙂

I would presume that any or all of the “Big 5” buying HCG loans would be a contradiction in terms, would it not? The reason HCG said yes to the borrower in the first place, is because the former said no.

Hawk

The company is done and will be sold in a fire sale. Already explained over and over that the issues is the deposits and not loans. You can twist this but by the end of next week the company will have different owners or the assets sold. A regulated financial company is as good as its reputation. Their reputation has issues.

The GIC issue only gives them a small runway to sale.

Do not be surprised if a consortium of the banks puts something together to buy the loans.

Contagion across the nation ? Latest on Home Capital looks ugggggly ! Another $12 billion ? Say goodnight Irene…. I mean gwac.

Confidence in the lending markets will spread like wildfire. No one wants to touch any of that junk.

This Is What A Bank Run Looks Like: Home Capital Loses 70% Of Deposits In One Week

“However, there is another problem: the company has another C$12.8 billion in Guaranteed Investment Certificate deposits, or GICS. As these 30- and 60-day deposits come due in the coming weeks, depleting HCG’s already tapped out liquidity, and forcing even more emergency loans. Without a deposit base, Home Capital can’t fund new mortgages.

As we reported over the weekend, while Home Capital hired investment bankers for a possible sale, there is little to no interest in the loan book as the company itself.”

http://www.zerohedge.com/news/2017-05-01/what-bank-run-looks-home-capital-loses-70-deposits-one-week

Local I love your whit. Serious than pow……

2017 prices defiantly up Hawk

Quick look and 5% across the board on page 6.

verb

http://www.vreb.org/current-statistics

805k benchmark vs 790k

She was posting on here somewhat regularly a little while ago. Prices will continue to double and double ad infinitum, despite wages or inflation. IE, extrapolation. Canadians are getting very good at doing it, so she’s in plenty of company.

It was rather interesting. It was a similar “the sky’s the limit” argument that you make, but you attach charts and aren’t quite as excitable.

She ran away screaming. 🙁

I am curious, Michael. I’m not trying to troll you here – could you please explain how you think Victoria will experience price inflation, from its current price point, to the same or similar degree to that experienced by Vancouver from 2001- 2017? If you don’t mind, dumb it down so that I may understand. Because…I don’t at all.

@Vicbot. Loved that chart. Made me laugh!

I see 1580 Despard, in Rockland, dropped its price by 145k; now they only have to drop it another 450k and maybe it might sell.

Not Santa, the guy in the “Red” hat Joseph Stalin.

Maybe 🙄 How do you know her?

Santa?

latest on Home capital

http://www.theglobeandmail.com/report-on-business/investment-bankers-look-into-possible-home-capital-asset-sale/article34862084/

The market is hot.

Agents that list their properties under market value by a hundred or two hundred grand are getting those properties sold in less than a week with no subject clauses or building inspections with multiple offers over asking price.

Speaking of misleading with charts …

http://i.imgur.com/AjLw9FM.jpg

Michael,

One of us is absolutely off our rocker. I guess it’s me. I was never an economist, so I can’t really argue. But lets just say:

Between then and now, Vancouver SFH’s had an increase of ~ 466%. So let’s extrapolate – if Victoria is around $850,000 for a SFH – in about 15 years, we should be looking at SFH’s just under 4 million dollars each.

In that case, my decision not to buy today is among the worst financial decision of my life. And yet, my MO is unchanged. I ain’t buyin’. Sigh…I don’t call me Local Fool for nothing, you know. 😀

Hey do you know db by any chance?

@ Barrister

“Do you really think Warren Buffet is about to resurrect our market?”

Nah. I meant the guy in the red hat.

@Local Fool

We’re likely around 01/02 on your chart.

Here’s the ‘road map’ I posted a while back. You can see we’re a couple years in to our ~7 year up-cycle (the yellow dashed-line), or near the ‘first sell off’ stage.

http://i.imgur.com/StTs6Bs.png

Vic

A radio morning show is more my thing.

gwac: “I don’t get married to any topic. Except Hawk”

Hawk: “Now you’re creeping me out with this OCD thing.”

You guys should start your own Comedy Central show 🙂

Need to fine tune my market summary page. Market still ludicrously hot, but also slowing down.

Just because I know how to post images now. I believe this has been posted before, but it’s a gooder.

Here is a series of predictions put forth by David Lereah just prior to, and during, the US housing market bust.

http://www.marketoracle.co.uk/images/2013/Feb/us-housing-bubble-1.jpg

“David Lereah was the NAR’s spokesman on economic forecasts, interest rates, home sales, mortgage rates, as well as other policy issues and trends affecting the United States real estate industry. Lereah was also the Chief Economist for the Mortgage Bankers Association during the 1990s and has testified before Congress on economic and real estate matters.”

“Lereah has been criticized for encouraging the rise of the United States housing bubble. According to a HousingPanic blog post quoted by the Chicago Tribune, “In October 2005 Lereah was busy calling the bubble believers ‘Chicken Littles.’ Many of the predictions espoused by the ‘Chicken Littles’ are fast becoming closer to reality. … David Lereah has lost credibility because of his irresponsible cheerleading.”

Hawk I know you do not like facts but here are the facts. Fraud is not what is causing this.

http://www.bnn.ca/amber-kanwar-home-capital-but-where-is-the-fraud-1.737658

Hawk the only thing sad is you on here posting daily crap because you stupidly sold your house and lost 100`s of thousands of dollars. You some how think your posts are going to sink the market. Seems the opposite happens.

I feel for all those on here who cannot afford to buy or cannot find something. You on the other hand are just a fool who speculated on your house.

Does anyone know if the two renovated houses that were for sale on Dallas Road (down by the breakwater) …did they sell? (They were asking around $2million each I believe, which seemed way too high.)

The for sale signs are not out in front anymore. Seems odd not to put a “Sold” sign on them if they actually sold. Perhaps they are switching agents? Any thoughts?

“Sales down 31% from last year”

Median down, sales down, and it’s raining out. Looks like another sad day for gwac.

“Just need a buyer for Home Capital to move on from this.”

Wishful thinking, down another 10% this morning. There is no moving on, this fraud will be busted wide open.

Cohodes gets fed info from those who quit from shame or got quietly let go. The fuse is lit.

“Cohodes remains convinced there is more to come. “Numerous shoes are yet to and will drop,” said Cohodes in an email to BNN, “and people will be outraged.”

Lol, good one Bearkilla. Where did you find them? Brietbart?

If you really want to have your mind blown re:science research things like this:

http://whotfetw.com/blog/wp-content/uploads/2016/05/Flat-Earth-Memes-129-9.jpg

http://www.bnn.ca/alternative-lender-equitable-bank-defends-itself-amid-home-capital-crisis-1.739529

Have we had an unusually high number of listings taken off the market this month?

CS:

Do you really think Warren Buffet is about to resurrect our market?

Leo Next topic is???? Conspiracy theories or climate change????

http://www.bnn.ca/home-capital-not-a-risky-investment-for-us-hoopp-s-jim-keohane-1.737275

Pension fund talks about Loan to home capital.

April:

885 sales

1270 new listings

1690 Active listings

Sales down 31% from last year

Inventory down 35%

@ Barrister:

“By middle of the summer”?

LOL

We’ve already seen it: no one but RE junkies at the open houses and four months of declining median price.

Surely only our Savior could resurrect this market.

Equitable will be able to cherry pick a good portion of the mortgages as they come up for renewal so why bother to buy the bad with the good. The banks dont want to touch any of these mortgages so who is out there that would want to buy these loans. it would take months to try to figure out which loans where fraudulent if it can really be done at all in a meaningful manner.

Rates will be going up for those who cannot get traditional mortgages.

So far the default rate is normal for their mortgages.

The company or portfolio hopefully will be sold this week. Home capital will bleed cash with their borrowing arrangement.

On Home Capital, has anyone figured out how much in the way of mortgages comes due over the next few months compared to GIC’s due?One assumes that they will not be renewing mortgages for the next while in order to redeem the GIC’s but how big a hole are they looking at?

When people have to find alternate financing we might start discovering exactly what percentage of their mortgages are actually junk.

Home capital draws 1b

http://www.cbc.ca/news/business/home-capital-monday-1.4093202

Equitable shores up capital, stock soars

http://www.theglobeandmail.com/report-on-business/equitable-group-moves-to-reinforce-liquidity-amid-rival-home-capitals-woes/article34862774/

Just need a buyer for Home Capital to move on from this.

We should have a new month of stats to pick apart soon. Went to a few open houses in Oak Bay this weekend. Did not see hardly any people. I know that my mind should have adjusted but somewhere deep in my brain I am really wondering if these small and often not well maintained houses are really worth over a million dollars. That is an enormous amount of money for your average middle class family.

There seems to be a lot of houses priced over 1.5 million that seem to have been on the market for months with no takers. If there is a slowdown we should see it by the middle of the summer after the hopes of selling in the spring market start to evaporate.

Please listen to Full 2nd hour at 16:45 regarding capital gains taxation on income suites:

http://moneytalks.net/article-and-commentary/michael-campbell/mikes-interview-of-the-week.html

When the scientists start to March I pay attention.

:large

:large

If there has been mortgage fraud (which it seems all too obvious) I sure hope Canada sets an example and gets some serious convictions with considerable jail time.

Vicbot

Don’t feed the trolls

Cahodes…and others… are also shorting Equitable Group, who also had a bad week last week. Problem, in my opinion, is contagion…international/large investors sell first then ask questions later…where does this lead in 2-6 months? The big Canadian Banks will likely be ok but they were sold off late last week and I’m watching to see if that will continue next week…I think it might. Not sure how deep the problem is, but where there is smoke there is likely fire….and there is a lot of smoke with hcg at this time.

Has he said if there are other companies he is shorting?

I think Hawk has some real big cahodes.

“I don’t get married to any topic.

Except Hawk”

Now you’re creeping me out with this OCD thing. You need to take up a new hobby like crocheting or something more relaxing. Good thing we have tight security here.

Funny how you want to sweep Home Captial under the rug like it’s no big deal. It reeks to high heaven of major fraud that will be the first major catalyst to pop this bloated pig.

“Cohodes remains convinced there is more to come. “Numerous shoes are yet to and will drop,” said Cohodes in an email to BNN, “and people will be outraged.”

Pie chart, please.

Yes there’s always a certain degree of error but unfortunately politicians exaggerate that when it’s a benefit to them (ie., money from the oil industry) instead of benefit to the Earth’s ecosystem (which would actually stimulate the economy, but they take the easy money route instead)

So there’s no proof that 99% of social scientists agreed that RE is a safe bet, and yet you’re asking for 100% certainty with climate science, so you’re holding the climate scientists to a standard that you’re not holding yourself to.

Even if the “whole planet seemingly believed” – that is not science.

Yes science is different than engineering but I work with scientists and we know what “peer review” means in terms of certainty in physics & biology. Math is also a tool used across all disciplines.

But the laws of physics are not the same as “laws” of economics – without the laws of physics, we wouldn’t have buildings, bridges, Internet, etc. The “laws” of economics are more pliable.

I also work with grad students and know the pressures they’re under, and I’ve also seen the effects of climate change first-hand – it affects real people, plants, animals today.

Interesting article: “Neoclassical economics is inconsistent with the laws of thermodynamics.”

https://www.scientificamerican.com/article/does-economics-violate-th/

The whole planet seemingly believed that about RE in the mid-2000s, most of whom didn’t know anything about RE beyond what they heard in the media. The same thing happens today with climate science. The vast majority believe it but most don’t know anything about it beyond what they read in the newspaper. As an engineer I’m guessing you likely deal with a certain degree of certainty in your work (i.e. design specifications, etc.). Science is different from engineering in that a topic/design cannot be conclusively proven (science is not exact); the conclusion instead has a certain degree of error. I’m not trying to convey that humans aren’t affecting the Earth system but instead that it’s not as black and white as some people make it out to be.

Climate science science and economics do actually have some similarities. They both attempt to make predictions about complex systems with massive numbers of inputs and variables. And they are both very bad at making those predictions.

Wolf could you point me to the study that shows that 99% of social scientists agreed with peer-reviewed studies that said that about RE being a safe bet, and what the bet was.

Local Fool I’m waiting for a CS arm wrestle at the next meet up. ☺

Vicbot, the mathematics behind real estate IS science. The same mathematics and statistics are employed across fields. You could further debate that it’s a social science. As for the fact that 99% of scientists agree, well that’s obvious. Many young researchers self-select themselves out of the field leaving a one-sided view behind; I noticed this regularly while I was completing my advanced degrees. Would you dedicate your career to disproving a notion or would you move on to something more constructive?

#2 example for incorrect mass consensus will be the decline in Canadian housing in the coming years.

CS and Vicbot:

Why don’t you two just agree that 9/11 was caused by humans. Bad humans. Lots of people died. Most perpetrators weren’t caught. The middle east is messy.

There 😀

Hawk, that Mr. Housing Bubble picture was hilarious. I laughed out loud. My g/f went to see what I was laughing at, and said it was “lame” and I was “even more lame to find it funny”. But it totally was, that’s what she doesn’t understand…

@ Vicbot

Did I say it did. No I did not. But the quote provides one of many reasons for doubting the US Government’s conspiracy theory about 9/11.

Here are some more reasons:

Not that I expect any of that to convince you, which I suppose is a good thing. If people don’t believe that governments tell the truth, then civil war is likely to ensue. You, Vicbot, are clearly a good citizen and believe everything the government says. Good for you.

Sorry Leo.

Can you tell I lost interest quickly. 🙂

I don’t get married to any topic. 🙂

Except Hawk

CS, your quote doesn’t prove that it was an inside job – your quote was related to the CIA’s cover-up of torture – that’s an entirely different matter than what you’re arguing about 9/11.

von Neumann was talking about global warming:

https://en.wikipedia.org/wiki/John_von_Neumann#Weather_systems_and_global_warming

“Von Neumann’s team performed the world’s first numerical weather forecasts on the ENIAC computer; von Neumann published the paper Numerical Integration of the Barotropic Vorticity Equation in 1950.[154] Von Neumann’s interest in weather systems and meteorological prediction led him to propose manipulating the environment by spreading colorants on the polar ice caps to enhance absorption of solar radiation (by reducing the albedo).[155][156] thereby inducing global warming.”

See what you did gwac? 🙂

@Vicbot

Von Neumann wasn’t writing about global warming. He was writing about planet-forming technology, in particular how to counteract a new ice age.

As for Able Danger, what’s that?

Here’s what Thomas Keane, Chair of the 9/11 Commission, said (among other things)

There is much more to confirm that the 9/11 Commission’s Report does not tell the real story of 9/11, but it has, obviously, no relevance here except to refute your mis-characterization of me as a conspiracy theorist. It was the US Government that insisted on the existence of a conspiracy, i.e., a conspiracy by others than the US Government itself.

Ya Hawk I think even you know that average and median is garbage in a small market like the core to determine market conditions over a few months. Not enough sales. It’s 2017 and you are still in an apartment because you speculated on your house.

Too funny.

CS, von Neumann was one of the first people to write about human induced global warming. From his 1955 article: “matter spread on an icy surface, or in the atmosphere above one, could inhibit the reflection-radiation process, melt the ice, and change the local climate”

For 9/11:

https://en.wikipedia.org/wiki/September_11_attacks_advance-knowledge_conspiracy_theories

The Chair & Vice Chair of 9/11 “issued a statement in which they stated the Commission had been aware of the Able Danger program, and requested and obtained information about it from the Department of Defense (DoD), but none of the information provided had indicated the program had identified Atta or other 9/11 hijackers.”

ie., they (US gov’t) investigated the theory and found it to be false.

House price surge ? Median in core is down $70K last 3 months. You’re a 2017 loser. Look out below.

@Vicbot:

If you won’t accept Scott Adams’s perfectly cogent argument that rubbishes your claim, how about John von Neumann:

“With four parameters I can fit an elephant, and with five I can make him wiggle his trunk.” Meaning, that you can find a function that fits any data series, e.g., past climatic data or whatever, but that doesn’t mean that you have a predictive model.

As for

You reveal your ignorance. The official 9/11 story is a conspiracy theory unsupported either by a forensic investigation or a judicial inquiry. Moreover, not only the Chair, and Vice-Chair, but also the legal adviser of the 9/11 Commission stated subsequent to the publication of their report that the report did not provide a true account of what happened on 9/11.

So, no, I am absolutely not a conspiracy theorist. And if you reject the US government’s unverified conspiracy theory, what remains other than an inside job?

Mtb hawk that is not on the road. It is on mountains thus mountain biking. Omg get some help. These house price surges are sending you over the edge.

Everyday hawk is another day to reflect on how much you lost by selling your house. Really sad.

Starting to think a gonfund me account is necessary for you.

“Home Capital assets will be sold as I tried to explain over and over to your simple mind. This is not a loan issue but a confidence issue about management so money is being pulled out that support the loans.”

That’s funny, that’s what they said about Lehman Bros and Bear Sterns. Then they got exposed for what they were, one massive ponzi scheme like the Canadian housing market is.

http://img194.imageshack.us/img194/4882/housingbubble.jpg

Gwac inhaled too many exhaust pipes on his bike ride. Daily price slashes in all areas including Golden Head where the foreigners have stopped buying still can’t get through his CO gassed noggin the party is over and only the few drunks remain. Sad.

Wolf, RE isn’t science. It was a question about scientific consensus 🙂

AG, people often confuse media consensus with scientific consensus. If it’s pumped 99% of the time by the media, they think that 99% of scientists agree. It’s not necessarily true.

There was never a ” 98%/99% consensus” on eggs, cholesterol, butter, high fat diets – it depends on exactly what action/result you’re referring to. Certain aspects of those factors may have had 50/60/70% consensus (eg., vegan diets by Dr Dean Ornish are still recommended to help people recover from heart attacks or deal with pacemakers – one friend who had to get a pacemaker at 60 went from carnivore to vegan based on doctors’ advice)

Also – eggs, cholesterol, butter, high fat diets. For 30 years the scientific consensus was that they are bad for you. The latest research says pretty much the opposite.

I’m just playing devils advocate here but I simply cannot resist:

An example “where 98% of the thousands of scientific experts on the subject have for decades been finding one result (made up of multiple results pointing to the same conclusion) based on theory and observation, and it turned out to be completely wrong”

Yes, that the real estate market in the U.S. was a certain safe bet in the mid-2000s. Everyone (almost everyone) was wrong and it crashed in 2007/2008.

Michael, yes I see your point on the C$. But I didn’t agree with your chart 🙂

“I have more science credentials than most of the IPCC.”

What are those credentials?

I guess the hysteria hasn’t fully subsided 🙂

Take a few deep breaths Vicbot, I have more science credentials than most of the IPCC.

And when you say…

…does it mean you no longer agree with what you said yesterday:

How appropriate that conspiracy theorists – who think 9/11 was an inside job – are now arguing against climate scientists. I shouldn’t bother with this but it’s sad …

The truth is too complicated so it gets crowded out – congratulations! Lazy brainfarts prevail. Yes the Great Barrier Reef is dying because of climate change – we’re losing ocean life & food sources, but who gives a shit because my house just went up 50% in 2 years. I’ll eat plastic! (yes I saw the reef in the 80s & now – it’s a disaster)

“Even IPCC ‘scientists’, or should I say bureaucrats …”

Michael is now saying scientists aren’t scientists. How ironic. He constantly posts nonsense graphs about data that has no correlation – and people call him on it repeatedly. Talk about the pot calling the kettle black.

“The diverge right away, but there’s a clear divergence in 2025.”

You originally tried to say that worst-case C02 should have resulted in worst-case temperatures immediately – not true. We’re not at 2025 or 2035 yet.

CS, Scott Adams is known for his Puff Pieces on climate change that are easily debunked. He spends too much time getting brainwashed by “alternative facts”

http://www.dailykos.com/story/2017/3/9/1641941/-A-detailed-reply-to-Scott-Adams-on-climate-science

“In a recent blog posting, cartoonist Scott Adams (drawer of “Dilbert”) took climate scientists to task for his own failure to understand how climate science (and as it turns out, science in general) works.

Actually, I quite sympathize with Scott. He clearly spends a lot of time reading “fake news” on climate skeptic websites, and that takes so much of his time that reading real science just gets crowded out.”

“For a scientist it is generally clear which arguments are valid, but it is indeed a real problem that to the public even the most utter nonsense may look “disturbingly credible”. ”

http://blog.hotwhopper.com/2016/12/scott-adams-puff-piece-on-disputing.html

Scott says: “In my experience, and based on my training, it is normal and routine for the “majority of experts” to be completely wrong about important stuff.”

Response: “Can you list three examples? … That is, where 98% of the thousands of scientific experts on the subject have for decades been finding one result (made up of multiple results pointing to the same conclusion) based on theory and observation, and it turned out to be completely wrong …

If as you say this is “normal and routine”, just three examples that are comparable to showing 200 years of an entire large scientific field are completely off track, should be a breeze for you. “

…and some money. Many trillions so far. At least the hysteria has started to subside. Even IPCC ‘scientists’, or should I say bureaucrats, have started to tone down the fear-mongering after all their failed predictions.

The diverge right away, but there’s a clear divergence in 2025. Regardless we’re supposed to be up to 2F and we’ve barely hit 1. It’s not going up another 1F in the next 7.5 years even though we’re continuing on the worst case scenario track.

True. Although the counter to this is that the herd has made plenty of money following the herd lately. So hard to tell if it’s a good or bad time to buy a condo. I wouldn’t, but I’m also not going to be wildly surprised if buying one now ends up working

I was driving through Sidney yesterday – and noticed sold sign after sold sign. Guess, the market is hot everywhere? Prices are probably, still, slightly more affordable up there than in the core… maybe Van. people like being close to the ferry and airport? Plus – it’s a very attractive (if not all that exciting) place.

Have Lower Mainland buyer percentages ever been that high? (with the exception of last year). How high was that in 2007 for ex.? This might explain junk houses like Carrick selling for $1,225k. If this trend continues we may well see price rises continue as we are still far cheaper than Van.

The Alberta numbers seem really low, given the number of Alberta plates I constantly see around town. (guess most of them are just visiting?)

Again, interesting on the US influence here compared to Asia. I didn’t think Asia was that high anyway, and most of the people of Asian descent here probably already Canadians or PR (unless int’ students).

CFAX was talking the other day about the recent vote in Vic council on asking the province to install the foreign buyer tax here. They said that they voted 4-4 so it got voted down. Interesting anecdote – the council member who was talking on the radio said there should be a speculator tax for anyone regardless of origin, not just a foreign tax, that way we can avoid empty homes like Van has, and keep housing just for living in? I thought – food for thought.

However, if Lower Mainland people keep coming here to live still in sig. numbers, I don’t see prices going down… if that continues I see disintegration of affordability for working people for SFH in the core continuing to accelerate. One of the things I remember about living in the Lower Mainland was that I encountered many many people, who, like myself – only could dream of living on the island – and when I left to come here many congratulated me on making that difficult transition happen. I made the dream come true for me, and now it would appear others are following (I know not everyone wants to come here but many do). Funny how long term island people who have lived here most or all of their lives forget or don’t realize that. It goes for people from other places too, like Alberta. It just doesn’t get much better than this in Canada…

Personally I believe the climate debate is moot and has historically been a waste of time. In my opinion society should be making the same improvements for other reasons like environmental and health concerns, quality of life, living efficiently, etc., not because there’s impending doom. But I suppose the stalwarts aren’t willing to modify their lifestyles unless they’re faced with catastrophic change. Kind of similar to real estate these days, isn’t it?

On another note, went to some open houses this weekend and didn’t see a lot of other people coming through. People holding out until after the election I presume.

@Vicbot:

Here’s what Scott Adams says about that argument:

Hawk

Home Capital assets will be sold as I tried to explain over and over to your simple mind. This is not a loan issue but a confidence issue about management so money is being pulled out that support the loans.

I think Marko and other have shown enough sales to show that things are still hot in Victoria.

I know you have the blues and are sad but coming on here is not going to fix your screwup. Maybe you can ask to go through the house you sold for hundreds of thousands less than what you could get now. Maybe that will help with closure.

Gold River just lost their only grocery store last Oct. Now, ‘Gold Riverite’s’ have to travel to Campbell River for groceries (a trip over an hour).

http://vancouverisland.ctvnews.ca/huge-loss-small-vancouver-island-town-s-only-grocery-store-closes-1.3187871

Here’s a listing similar to a 70’s Gordon Head Crap box… in Gold River… lovely mountain views, just like those views of Mt. Doug. 🙂 Here’s an idea, sell your GH crap box for over $1m – buy seven in Gold River! Become a Gold River slumlord! (but wait, no one wants to live in a town w/ no grocery store?)

https://www.realtor.ca/Residential/Single-Family/17448968/528-EAGLE-CRES-GOLD-RIVER-British-Columbia-V0P1G0-Z7-Gold-River

“We actually were close to the worst case scenario w/r to actual emissions produced, yet we didn’t haven’t even hit the lower emissions temperature level. Don’t know how people can take the predictions seriously when it hasn’t really been close.”

The graph you posted shows the opposite.

Related to history: The graph shows that the models (in green) accurately reflect the actuals (in black). That’s what the models are supposed to do – reflect history. Also they show temperatures increasing about 1 C since 2000, and they’ve been actually around 0.8C.

Related to the future: The blue, red, & pink lines (with best & worst case scenarios) are all the same up to 2025, so if the C02 increase was worst case (9B tons), the models are still accurate – because they only diverge (from best case to worst case) around 2035.

In fact we’re on track to be worse than what was projected in 2001. See the multiple, corroborating, peer-reviewed studies from 2007 & other dates – more info here: http://www.climatecentral.org/news/ipcc-predictions-then-versus-now-15340

Funny how some people trust science to give them pacemakers, but don’t trust the same scientific method when politicians get involved. Anyway, back to housing.

gwac or AG must have all their relatives panties in a knot. This is just more signs this bubble is about to blow when the one of the few bears gets stalked by a parody account. I’ll take it as a badge of honor. 😉

It is amazing how some folks are so chickenshit of reading the fact based news like Home Capital fraud exposing the housing bubble and call it “over the edge”, lol.

Wake up and sell ASAP before the easiest money you’ll ever make disintegrates before your very eyes.

Spike In Canadian ‘Housing Bubble’ Searches A Sign It May Be Ending

“Like in the U.S. before its bubble burst, the economy’s dependence on housing construction has reached an all-time high; household debt has hit an all-time high; the number of housing markets seeing rapid price growth has hit an all-time high; the quality of mortgages being issued is on the decline; and at least one major private mortgage lender is in trouble over its lending practices.”

http://www.huffingtonpost.ca/2017/04/17/housing-bubble-searches-google-canada_n_16061058.html

Out and out reckless. Anyone who makes an investment choice employing that kind of logic has more money than brains, does not understand elementary investing, and is at significant risk of becoming the poster-child of riches-to-ruin when the market turns.

“Suzy” isn’t alone, either. There are legions of people that are thinking like this and indeed, I suspect this is what is floating the market more than anything. There’s nothing wrong with a bit of speculation in the market, in fact it can be a good thing. But not this.

This is the sort of uber dangerous poppycock that causes me to think that when the RE cycle begins anew, the preceding reversion has the potential to be particularly traumatic, even for those who have behaved prudently.

A little Xanax with my coffee might be helpful?

Meant going Mtb. Should check spell check.

I wouldn’t say I’m a fan……I do enjoy the balance on here but it seems that Hawk is always going over the edge. I also love the fact that because I don’t agree with him I must have bought too much and I’m downing in debt. Ever thought that I just don’t agree? Also to Deb I never said for him to be quiet…..otherwise it would be very dull around here.

Hawk

How’s apartment living. How much equity has that apartment made for you? A big fat duck egg. Nice job dude. Nice day out there. Great info MTB willl check in on you latter Hawk to make sure no one believes your lies.

Totoro there are some good tutorials on youtube.

No I’m not doing that at all. What I am doing is calculating the median SAR for all of the sales in April and comparing that SAR to the median SAR of all of the sales in a previous month to derive an economic conditions factor of how the SAR has changed or not changed during the two time intervals. I am not using this to gauge value but as a cross check to the analysis from other sources.

Since the assessed values are as at a specific date and have been acknowledged as a recognized and relaible estimate of value, I am comparing the current sales data to a recognized benchmark. And how that ratio changes over time gives an estimate of how market conditions are changing. This is similar to what an HPI does and what the re-sale method popularized by Case-Shiller does, except any third party can verify the data and can run the numbers and get the same answers.

The SAR does not always agree with the median or average of the sales in a given month. During the winter months as the volume of sales decreases to under 100 for detached houses in the core, the error in the data gets larger as the sample size gets smaller. Then you need to increase the sample size in order to determine a reliable cross check.

When you look back at the median and averages in the winter you’ll see big increases in the median and average prices followed by big decreases the next month. The SAR allows you to cross check those wild price swings to see if the median and averages are reliably portraying the marketplace or are subject to sample variability. This is similar to what the HPI developed by the Altus Group purports to do. Or the Case-Shiller Index but with a lot more data points.

One final post before I get back to work…..how nuts are things?

A home in the Westhills pre-sale purchased for $639,900 (gst included). Never moved into to and sold on completion of construction for $799,000.

Vancouver also still appears to be nuts. One of my clients is buying a condo in Yaletown. He offered $613k on a 462 sq/ft unit in Yaletown listed at $599k earlier this week and got outbid in a multiple offer situation.

10,000 sq/ft building lots on Braefoot selling for 830k+GST. Selling in as they are sold.

Eventually, people that can barely afford the payments hop in the market because they’re tired of being left out. This creates a sudden surge, as the buyer pool explodes. In a market like this, even homes that typically wouldn’t be desirable to buyers start selling at a profit well beyond fundamentals.

The amount of phone calls I am receiving about investment condos in the last two months is completely off the charts and the logic behind some of them is quite scary.

A woman called me earlier this week from Vancouver, we will call her Suzy.

Suzy, “Saw your YouTube videos, seems like you know a lot about pre-sales, I would like to buy one and my budget is around $300,000.”

Marko, “Not sure if it is a great time to buy to be honest as the cash flow numbers based on 20% down don’t really make any sense anymore.”

Suzy, “That’s okay, I want to buy so the unit appreciates over the two year build out.”

Marko, “Pre-sales aren’t selling discounted to market anymore; therefore, the only way the unit would appreciate is if the market goes up.”

Suzy, “Yes, around 20%/year so I’ll get an amazing return on my deposit.”

I can’t wrap my head around how quickly people forget that if you bought a condo in 2007/08 you were still under water by 2014, throw in a bad tenant or two during that 6-7 year period and a special assessment….many people lost their shirts. Seems like everyone has forgotten and markets can only go up?

In my 7 years, I guess my observation would be buy when no one else is buying. I wouldn’t go as far as to say sell when everyone is buying as it could be the start of an upswing but buying when sales volumes are extremely low, especially after a prolonged flat run seems to be the way to go.

Doesn’t even seem like it is too complicated to be successful in real estate, just don’t follow the herd.

Oh yeah I totally forgot to mention. The VREB is now publishing the buyer origin reports quarterly. Hooray!

Foreign buyer numbers are very similar to those collected of the province. Less than 5%. Even though I am not a fan of governments interfering in market the foreign buyer tax would have helped to cool off the madness by influencing non-foreign buyer psychology.

Gold river?

Love the smell of napalm in the morning. I was worried that Hawk-n-Gwac had reconciled or something.

With respect to the Vancouver buyer numbers, I’m curious as to what the ratio of shelter vs investor buys are. If some in Vancouver think Victoria is the next New Paradigm™, a few might look to tap into equity to make a speculative purchase. OB comes to mind. Doubt there’s any way to know, but curious nonetheless.

“I question everything.

Reminds me of a quote that seems to apply to you: “If you open your mind too much your brain will fall out”

Not much left to pick up. It rains for a couple hours and the guy suddenly has no life. 😉

“People like Gwac are around us, and it is fucking scary.”

Only the second thing I’ve ever agreed with you Introvert. I think he drinks a lot, no one can be that fucked up. Did you see Trump praising his record crowd rally last night with all the empty seats and no line ups outside other than protesters ?

Gwac is our HHV Canadian Trumpster. Next thing he’ll tell us is renting is the gateway to heroin. 😉

Nice to see I have a new fan club member. Must have bought too much house and feeling the pain of all that large mortgage payment going down the drain month after month.

Victoria is Vancouver’s Duncan. The great shuffle is happening. International money is pushing out the Vancouverites who sell their houses for three million and come here thinking a million is nothing. Victorians sell their house for a million and think half a million is nothing up island. Problem is I think Duncan has a .05% Vacancy rate right now…. Where do the Duncsters go?

Oh yeah I totally forgot to mention. The VREB is now publishing the buyer origin reports quarterly. Hooray!

For Q1 2017:

Victoria and South Island: 76.49%

North Island: 2.24%

Lower mainland: 10.06%

Other BC: 2.3%

AB: 2.42%

ON/QC: 2.12%

Other Provinces: 1.14%

USA: 2.36%

Asia: 0.55%

Other countries: 0.3%

10% of buyers from the lower mainland is a lot. In 2015 and 2014 it was only 6% (and sales are way up since then). Similar percentage from lower mainland as last year.

It is a very difficult concept.

No it doesn’t because that is jibber jabber. If you sell and get 94% of assessed the sale it is not off from assessed by 94%.

It seems that BCCA doesn’t evaluate this against all sales. They use the median sale and adjust for inflation/deflation (time). You also need to know the coefficient of dispersion, adjusted for time, to really gauge accuracy.

What you are doing, imo, is taking the SAR for the median house as of July 1, not adjusting it for time or applying a COD, and using it to gauge value.

This is also why sales to assessed for the median, never mind the rest of sales, is so far off of the July 1 number when you are looking at sales occurring in April.

http://www.dailyclimate.org/tdc-newsroom/2012/12/12fotos/emissions-500.jpg/image_large

Those are the IPCC predictions made in 2001 based on computer models.

We actually were close to the worst case scenario w/r to actual emissions produced, yet we didn’t haven’t even hit the lower emissions temperature level.

Don’t know how people can take the predictions seriously when it hasn’t really been close.

“The argument is inconclusive if you have even the slightest knowledge of partial differential equations.”

I’ve worked with differential equations in uni & in engineering – and no, the arguments aren’t “inconclusive” – 99% of scientists agree that the models reproduce past & present climate, and so they are useful in predicting future climate. Just because there are some drawbacks to the models doesn’t make them inconclusive.

The same math & physics equations that go into those models are the ones that make your iPhone & Internet work. So why don’t you just go out and design your own semiconductors, firmware, & software that operate all your electronic toys that you use everyday.

It’s the same reason I trust a heart surgeon to operate on my parents – not Dr. Quack who has decided that PL Premium adhesive is good way to mend arteries.

So yes, if thousands of scientists have devoted decades of hard work to understanding the models, and reviewing their peers’ work, I’m going to trust them, not some kneejerk “skeptics” that try to poke holes in things they don’t understand.

That’s the kind of lazy thinking that gets us quacks like Oneal Ron Morris injecting cement into people’s butts (look it up)

Of course. Problem is, many people can’t even imagine such an occurrence in Canadian RE, let alone accept the possibility.

Local Fool:

“Eventually, people that can barely afford the payments hop in the market because they’re tired of being left out. This creates a sudden surge, as the buyer pool explodes. In a market like this, even homes that typically wouldn’t be desirable to buyers start selling at a profit well beyond fundamentals.”

I’m not implying it’s impending, but the same is true the other way around when people have made a bundle of cash.

@Deb. The term “climate change” is not correct either. Climate change is a sexy term that researchers put into their proposals to win funding from the government. Online courses offer little credibility if that’s the bulk of your background on the topic.

I get a kick out of the people who use the Flat Earth argument to discredit deniers. This argument suggest that deniers are similar to those who believed the Earth was flat centuries ago, and that they’re a minority who believe in an incredibly dated premise. In actuality, however, at that time the Earth was widely accepted to be flat and those who believed the Earth was round were in fact the minority (who were stoned to death for being correct). A similar thing likely happens today when believers chastise deniers.

The argument is inconclusive if you have even the slightest knowledge of partial differential equations. But few seem to know what those even are and unfortunately most learn about climatology through the media.

Don’t worry though, the land value of your house will probably increase as it becomes waterfront with the previous waterfront homes crumbling from magnitude 10 earthquakes and washed away by 100 foot high tsunamis! Buy into the culture of fear, just like FOMO.

Victoria’s RE Market

1608 Michelle Pl, Gordon Head, was listed at $885,0oo and sold for $: $1,020,000.

Judt my opinion, but I think that’s ridiculous.

Perhaps I am stating the obvious but Heritage houses vary dramatically. A lot of them where crap house when they were built and time has not improved them any.

On the other hand there are a handful of the old manor houses that were of superb quality that have dramatically increased in price because of the value of the craftsmanship. Not my house but I looked at one house that had an intricate marble carved fireplace surround that took a team of master Florence stonemasons four years to carve. The solid mahogany paneling had detailed carvings throughout. These houses are the exception and the cost to reproduce these features in a new house would be immense just in the cost of materials alone but such is not the case in most heritage houses. They may be old, they may be cute but they also may be a nightmare for maintenance.

I don’t take the $motivations of either side too seriously, but I would bet we get “Another Ice Age” scare in the next decade or two (like the 70s), as I do think we go through natural cooling patterns as well.

http://i.imgur.com/RmQISPy.jpg

Sorry for the off-topic, but one has to admit it is an entertaining ‘blast from the past’ on a cold & rainy Sat afternoon.

I did. There will always be outliers.

What do you think that meant?

Because you’re not grasping the point about medians. Saying that the values ranged between 94 to 170 percent does not mean that the assessments are wrong by 94 to 170 percent. More than 98% of assessments are not appealed. If you look on BC Assessments web site you’ll find that they test their data for accuracy against sale prices as at the effective date of July 1 to within a 97% to 100% for the residential assessment roll.

Median: denoting or relating to a value or quantity lying at the midpoint of a frequency distribution of observed values or quantities, such that there is an equal probability of falling above or below it

Yeah this rain is going to kill sales for the month for sure. Probably the start of the long awaited crash. That’s what always happens in low inventory high demand periods. The crash happens.

Thanks Leo. Did you actually believe me about the climate change thing. :). I just love stirring shit and getting a reaction.

We are fucking up our planet so badly. Kids and future generations pay the price. Hey I bike about 10,000 km a year. Trying to do my part.

Where’s Hawk. House buying?

Nope I’ve calmed down again. Carry on.

Leo so fed up. Next week looks a bit better. Let’s. Hope. Sorry for causing shit.

No kidding. I remember 2011 was a similar summer, and at least one other where it was cold well into july….

Leo

Gwac script. Good one. You want me to stop. Your board. Just let me know.:)

Leo only on the weekend? The weekdays are for keeping Hawk in check. That work for you. It’s raining and I am bored.

My gwac script is getting out of hand again. Should have programmed less “shit disturbing factor” into it. 🙂

https://en.m.wikipedia.org/wiki/Climate_change_denial

I really like the oil/gas lobby. They have spend tons on studies so they say climate change is a hoax it must be. They would not lie.

Boring troll is boring. This nonsense only flies on the weekend gwac.

Donald Trump. He knows all.

And this guy.

https://www.google.ca/amp/www.cnbc.com/amp/2017/02/17/murray-energy-ceo-claims-global-warming-is-a-hoax.html

@Gwac “Global warming is the the biggest BS to come out ever.”

This is the comment you made and why I thought you might need a little help with the correct terminology.

Could you tell me what sources you consider reliable?

Oak island is a perfect example of how gullible people are. 200 plus years ago someone saw lights on the island and for the past 200 years people have dug up that island over and over searching for treasure. It has a TV show right now. For the past 5 years it is one of the highest audience cable shows

In general people are gullible and believe almost anything from what they may perceive as a reliable source.

It was, actually.

Deb “Hawk is the balance”. That is the funniest thing I have ever read on here.