Equal affordability, but some affordability is more equal than others

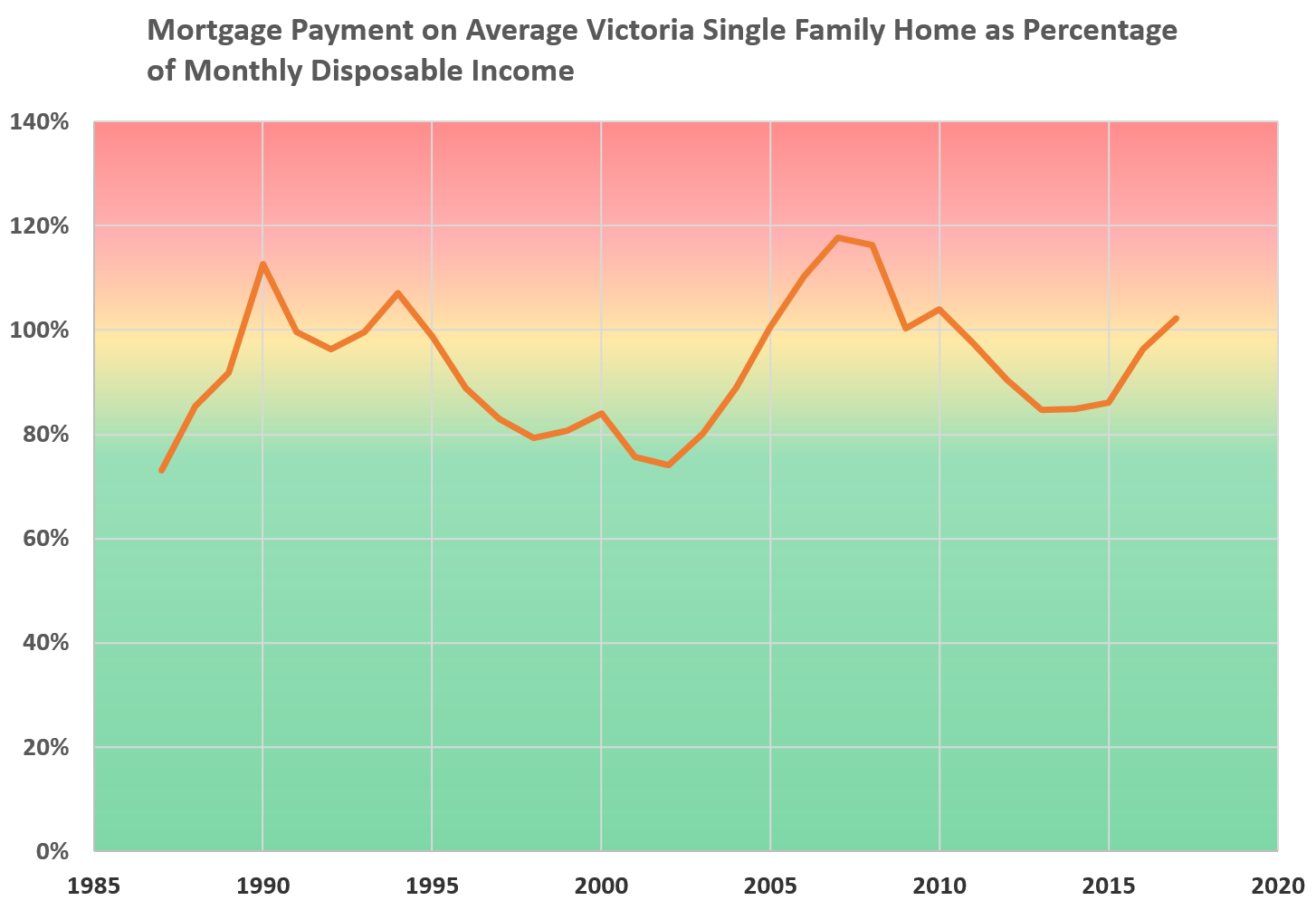

I’ve yammered on enough about affordability and how despite being at record high prices, mortgage payments as a percentage of incomes are only middle of the road compared to historical norms. Looking at the latest numbers for January, that is still true, although it is getting more and more stretched.

So despite the fact that today’s average house price of $800,000 has more than tripled since 1993, it is taking about the same percentage of the average income to service the mortgage. Of course this doesn’t take account the down payment. In order to avoid CMHC, someone purchasing today’s average $800,000 house would need $160,000 while in 1993 they only needed $50,000.

Put another way, someone buying in 1993 would have to save all their disposable income for 2.5 years to come up with the down payment for the average house, while in 2017 they would have to save every spare penny (and by that I mean not eating) for over 4 years. Of course people are making it happen somehow. Larger gifts from the bank of mom and dad, fewer percent down, or some free money from Christy Clark.

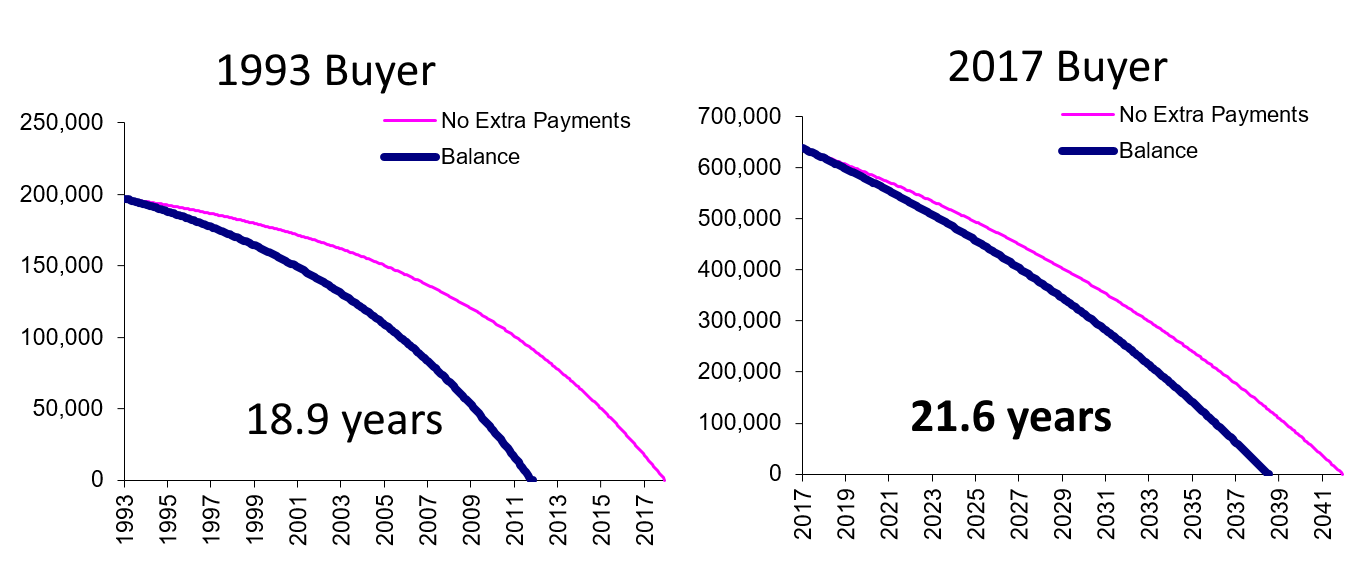

However that’s really not the main problem with the idea that since affordability is OK, all is well. Let’s take the same hypothetical buyers in 1993 and 2017. At the beginning, they both have mortgages that take the same percentage of their income and will take 25 years to pay off. That’s where the similarities end.

Now imagine they both get a 10% raise and put the extra money towards their mortgage payment. How does the situation change?

10% extra on payments carved more than 6 years off the mortgage term for the 1993 buyer compared to only 3.5 for a buyer now. No matter how low interest rates are, you still gotta pay that $640,000 back somehow.

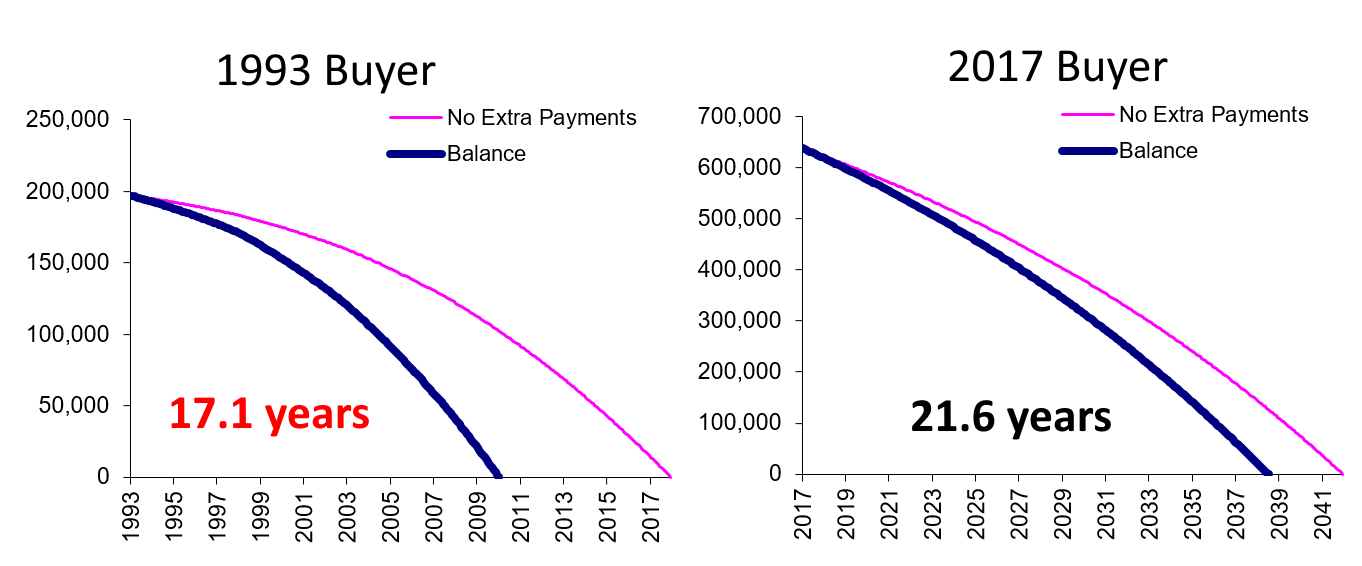

Even that isn’t the whole story though. In 1993 that buyer could have looked forward to continual drops in interest rates every time they renewed, with fixed rates dropping from 8.7 to 4.2% over the term. Meanwhile if today’s buyer is extremely lucky interest rates might stay as low as they are for their term. Here’s the effect:

So there you have it. Despite monthly affordability being exactly the same, today’s house buyers will have to save almost twice as long for down payments and will be paying for the place 5 years longer than an equivalent buyer 25 years ago.

The finishing doesn’t look that high end.

Where’s the helicopter landing pad, the pool, the gold plated faucets, the cedar lined closets, solid fir hand carved doors?

The home is custom but there are a lot of homes being built to that same standard for far less. Only 2,400 square feet is above ground. Surely you’re not going to pay $300 to $350 a square foot for basically a hole in the ground with average basement finish.

However, your basic understanding is completely off. Where in the rule book of life does it say that the cost to build has to be the same as the purchase price?

All that is different is the builder has increased the profit margin from 15 to 25% where there is a lot of new construction occurring to 100% or more where there is little new construction in competition.

As more contractors see the windfall profits they will enter into the market and drive profit margins down. Again, that’s why I’m thinking of building two new houses in Oaklands. At this time there seems to be a windfall. But you have to be at the start to make the coin.

@AG True now yes but they built that place in the slow times. Plus it’s just the finishes (like one bathroom per occupant plus guest) that are expensive. I bet it’s still low end framing and minimum code applications everywhere else.

You are over generalizing Totoro.

What if you sell the shares to a dozen investors? Is the property tax payable every time an investor sells their shares?

“Construction $750k”

That seems way too low for a 3600sf home with high end finishes. Retail cost would be more like 1.2-1.3m surely? I doubt you could build it for less than $300-350/sf.

726 Victoria Ave.

Land cost $650k

Legal, taxes, etc $13k

Design and permiting $50k

Demolition $40k

Construction $750k

Carrying cost $30k

Total Cost $1,543,00

That’s retail construction cost too so this probably cost the builder less. A profit margin of 50% for building. Pretty good! Same thing happening in lesser neighbourhoods for lesser amounts. Take the Mt.Tolmie area. Corner lot is bought for 600kish, demo, lot subdivided in two, build two low end houses for 300k each on super small lots and sell them for 1 million each. Similar markup structure. This is why we are in full tilt building wise right now. If you are a builder that can add value to the property then money can be made.

When a buyer buys a place with a corporation they pay PTT. Owners don’t generally incorporate to avoid PTT. The tax consequences would not be worth it.

The most common reason people buy through a corporation is generally to invest retained earnings if they are otherwise at a very high tax rate on their income. This is a speculative move as you’ll pay capital gains tax and income tax at the top marginal tax rate within the corporation.

John Dollar:

Being from Toronto most of my life, I also lived through the real estate boom in that city. I think we are returning to the question of how many out of town buyers are actually hunting in Victoria? But if this is the new benchmark then I suspect that most retiring boomers would look elsewhere.

Certainly, at these prices today, I would have probably felt there was much better value in California or elsewhere.

New post: https://househuntvictoria.ca/2017/02/20/february-20-market-update/

Your financing rate will be higher through a corporation if you need to borrow. You’ll pay approx 46% income tax on profits in the corporation prior to any dividends – not 15% – unless this corporation has more than five full-time employees engaged in the re business. I’d say you should go see an accountant.

Barrister, I’ve seen this happen before when I worked in Toronto. Where the sale price was well in excess of the reasonable costs to buy the land today and construct the improvements. It’s underscores an overheated market.

Think of the logical conclusion. If this home were to become the benchmark for housing in Oak Bay, then everyone would raise their asking price by a million dollars over night. That would likely crash the market. Sustainable prices rise by increments not leaps.

Thanks JD. Actually I’m mostly thinking about the fact that rental income is taxed at regular income rates. It seems to me that if I put the property in a corporation I can pay the low corporate income tax rate (~15%) and then draw out the remainder as is tax suitable for me (i.e. as a dividend etc.).

The fact that rental income is taxed at your personal income tax rate along with the fact that your second property incurs capital gains tax whereas your first does not are pretty solid disincentives to buying an income property!

Muklak, currently there is a 5 suiter listed for sale that is a private corporation. This isn’t the first time that owners have incorporated a property in the hope of avoiding the property purchase tax. The ideas is that since you are buying shares and not real estate, property purchase tax is not applicable. However, I think there has been a CRA ruling on this in the past so you should get written confirmation from CRA.

Financing may also be tricky. I believe in the past it was necessary to have the lender hold the shares at the bank. This is because a bank can not foreclose on shares. Otherwise, you could get financing and then sell your shares without the bank knowing.

The share value does not have to be the same as the value of the real estate. The property could have a real estate value of 2 million but you could issue shares with a total value of 4 million. For example you could sell shares to 10 people at $400,000 a piece.

And you don’t have to buy all of the shares at once. You could buy 51% this year and 49% next year.

Maybe Leo S can explain how a real estate agent is licensed to sell shares?

Here we are at the beginning of a new week. As some of you now I sort of keep my eye on SFH in South Victoria (James Bay, FairField, Rockland and Oak Bay). I am not sure about the rest of Greater Victoria, and on a totally unscientific basis what I am seeing is a mere trickle of houses coming on the market but also a mere trickle being sold. Well over half the houses listed were on the market at least since Christmas and a few a lot longer.

I am not sure what to make of it. It is like we are frozen in time. Not sure what it signifies for the market moving forward.

On a separate note, I am still shocked about the sale of the house on 762 Victoria Avenue for 2.5 million. Judging from the pictures it was a nicely done new build house but nothing spectacular.

There was only about 2,200 square feet above ground (yes, it had a finished basement in addition but still that is a basement). Not exactly a manor house in any sense of the word. It was a small lot of 7000 square feet. Not only was it not on or adjacent to the ocean it had no views of the ocean. Nor was it a short walking distance to Oak Bay village. Is this the new benchmark price or is this the last crazy sale in an overheated market. I cannot but help to shake my head when I think about what I paid for my house a mere three years ago and what this one sold for today. As much as i love Victoria, something does not feel right about this market.

@john Dollar “And that’s why there HAS to be a 2% tax (on assessed value) for condos that are rented as airbnbs for more than 6 months of the year.”

I totally agree there has be some some kind tax. I have just been checking out Airbnbs, and I am shocked by how many there are. A bunch just came up in the Janion, and I am now wondering if maybe those people who camped out to buy a suite a few years ago weren’t as dumb as I thought. I do wonder how these buildings will age, though, being used as a “hotel” vs. residential.

My story of renting vs. buying a condo is this: I did not buy a condo 15 years ago because I was only paying $570 a month rent for my one-bedroom and thought that was good enough. It was cheaper than buying. The building got sold a few years later, there was a renoviction, and rents nearly doubled. From what I can see, most condos have at least doubled in value since then. That’s not as good increase as a house, which tripled, but still ahead of renting (as long as one did not buy into a “dud” building).

Sorry to tell you, Hawk, but rent for a one-bedroom suite in the core that’s in a purpose-built building is around $1000 a month. Check out the Devon properties website. Newer condos are over $1700 (like in Era), even for a one-bedroom, which makes sense if it can be rented for over $3000K on Airbnb. No wonder there are so many sob stories on Craigslist of people looking for an affordable place to rent.

No, generally best to own it personally.

If I want to buy an income property over and above my primary residence, is it generally best to put it in a corporation to allow for tax mitigation?

Funny Local Fool, great use of adverbs & adjectives 🙂 I also had an experience with Lowe’s this weekend. I needed to buy something off their web site, but it wasn’t working (had to buy from wayfair.ca). I phoned Lowe’s to tell them; they said their site hasn’t been working for months. Makes you wonder how the whole Rona takeover is going.

Michael: “Vancouver’s sell/list ratio sure finished the week strong. Correction over?

Wed 74%

Thu 77%

Fri 86%

http://www.robchipman.net/”

Michael, it’s useless to post these stats — condos in Van are doing great, townhomes so-so and houses tanking. Multi-family and commercial have been going strong the entire time. Lumping them all together completely skews the picture. Check out Steve Saretsky’s stats instead if you’re going to post stats, he breaks them apart and gives a more accurate picture of what’s actually going on.

Market Crash this weekend:

That was well-written, Local Fool.

OK, back to real estate:

Battle lines drawn in Cordova Bay: Too much, too fast, critics say

http://www.timescolonist.com/news/local/battle-lines-drawn-in-cordova-bay-too-much-too-fast-critics-say-1.10099321

An over-arching plan for traffic management is required, he said, given the shopping centre alone would have 320 parking spaces, the majority underground, and drivers will rely on Doumac Avenue for access.

Watching this project proceed (or not) is going to be interesting.

Well, now that Victoria real estate no longer offers subject matter for discussion, I guess we move on to less relevant things.

I went to check out the new Lowes in Tillicum mall today. I found it to be a lousy version of Home Depot, and their tool section was unforgivable. Angry from the experience, I went and got a chocolate frosty at Wendy’s drive thru – made everything better again.

Saw a homeless person nearby and felt lucky, and briefly marvelled at the burned out wreck of Blanshard Courts. Wanted to go to Canadian Tire Hillside, but I always find something on sale that I just must have. My poor bank account. No impulse control, guys. It’s horrible, but man is my tool chest well stocked. I could disassemble and service the space shuttle Discovery at this point.

Instead I went home and did laundry, and checked out some RE listings. Went to HHV to check out the banter; I learned that I best not use a semicolon incorrectly or Introvert might take me to visit a vivisectionist.

That’s it. Thanks for listening. I’m going to have a drink. Cheers, bulls and bears.

“…….a pedant like me can’t help him/herself.”

Attachment is the source of much suffering; attachment to rules; attachment to outcomes; attachment to the need to teach others the “correct use” of semicolons. All of this can cause colon problems and serious suffering::::::::;;;;;;;;;;;;:::::::::

“Ow! My Brains!”

Ten out of ten for grammar, but minus several million for content – Zaphod Beeblebrox

That semicolon should be a colon. [facepalm emoji]

They are, but some errors are so egregious (and/or repeated so often) that a pedant like me can’t help him/herself.

I’m guilty too. But I’m not taking it very far. Believe me, I could go miles farther (but I don’t).

Sign Post in the Bushes, you outed the troll on that one.

“The Tesla veered into oncoming traffic”.

Really seems like if you’re out to do that you might be better with a Ford Pinto. At least those exploded when you decide to go kamikaze.

I don’t expect people on the blog to be precise with punctuation, since ideas are more important.

But I’ll weigh in 🙂 since my job required me to be extremely precise with meaning, and semi-colons were important. A semi-colon really is supposed to be used only between 2 independent clauses (that can stand alone as noun-verb sentences themselves), or as a “super-comma” in a list of items where each “item” contains commas.

http://theoatmeal.com/comics/semicolon

But we’re all guilty of misplaced adverbs, misspellings, etc – there’s only so far you can take it on a casual forum.

At least Introvert has the self-awareness to know that he/she is a pedant.

“Welcome, Introvert 2.0” AG

Are you having trouble, following the thread AG? The Dictionary definition was for Introvert.

Welcome, Introvert 2.0

From the Oxford Dictionary;

semicolon n. Punctuation mark (;) indicating a more marked separation than the comma, and less than a full stop or colon.

Wanted to comment on the condo ROI based on 30 years of my own and friends’ experiences …

If I was on my own I’d probably live in a condo, but anyone thinking of owning one needs to know the truth …

1) Yes you can make money back on the asset if you sell at the right time. If I had sold mine in 1995, I would have lost 36% from purchase price. Because I hung on for a few more years, I gained 100% on purchase price, but that doesn’t factor in special assessments.

2) If you buy & then sell within 1 or 2 years & prices have increased & no special assessments have been charged, then Michael’s calculation is accurate. However, his calculations apply more to investors & speculators, not your average person that wants a home for 10 years.

3) Special assessments really do add up to tens of thousands of $ for things like: roof replacement, pipes, elevators, heating systems, security, underground parking lot fixes (water ingress in common & expensive to fix). As Hawk’s article points out, it can be > $50k.

If you’re thinking of owning a condo for the long term, be prepared for the following:

a) Allocate at least $10k to $20k over 10 years for special assessments. Do your own diligence, read the clues in meeting minutes, stratas will try to dress up an issue to protect property values – an inspector can’t tear apart the walls to find the truth.

b) Values don’t go up by the same % as houses

c) A downturn in the RE market may allow you to trade up into a house, eg., a $300k condo goes down 10% by $30k, but a $900k house goes down by $90k.

“I recommend you learn how to use a semicolon.” Introvert.

Thanks for your recommendation and your obvious concern for my education. Now where did I put my copy of “Eats, Shoots, and Leaves.”?

I recommend you learn how to use a semicolon.

Just Jack doesn’t have lots of money, so now I’m wondering whether John Dollar is him. But it has to be.

I’ve had a lot of expensive vehicles but my favorite has always been the cornbinder.

No one wants to park beside you and they give you plenty of room on the road.

https://youtu.be/Dyz_5bx-Lho

LOL

Hawk, that will scare the hell out of Chinese investors. As I have been told over and over again by people that manage Chinese real estate investments, the Chinese like to buy new and hold vacant. They do no want to spend any more money than the absolute minimum on repairs or maintenance. This is more cultural aspect as they focus strongly on family and less on society. Which is different from the West where they place a heavy emphasis of living in a community.

If you live in a condo tower that has a lot of absentee owners you are going to have increasing deferment in repairs.

https://youtu.be/_lAoTBVTTO8

yet who must drive the latest Tesla

https://www.youtube.com/watch?v=QtgTcoT1yRo

Rather pay a few extra bucks and survive or sustain less significant injuries….worked long enough in the hospital to see enough people coming in from car accidents.

or live in the best neighbourhoods

Can’t buy time back that you spend sitting in the Colwood crawl.

Just Jack – interesting thoughts. I guess being an appraiser gives you a unique chance to spot and take advantage of these opportunities. And by the way, I own several properties here so I guess I am a speculator.

Mikey likes it! We’re all very fortunate to have that ability. Well said, and I like your name too.

Uh oh, Jack John is thinking of getting into the market… could this be a top?! Unless it’s another one of his sneaky ploys to scare us 🙂

AG, there is nothing wrong with a speculator. Since they are currently soaking up inventory that will be brought back onto the market in a short time. Temporarily they will drive up prices but since their purpose is to sell in the near future and not to hold long term, they will eventually add to inventory and that should stabilize prices.

The speculator accepts a very high level of risk in order to get a potential windfall profit in a short time.

For example I’m working out the numbers if I should gamble a little under 2 million over the next 9 to 12 months to build two houses in Oaklands. I can take all the risk myself or spread it out with other investors of which I know a dozen or so that would come in on the deal. But there are some other deals out there that look good too. Where I don’t have to outlay that much cash and have a quicker turn over. Such as a property in Lakehill where I can go in with the adjoining home owner at the corner and subdivide a new lot off the back that would front onto another street. The same with a property in Fernwood where I just have to buy the house on a corner as the owner of the house second door in wants to subdivide.

If you are buying a house to live in it and renting the basement for extra cash that’s not a speculator. Or if you are buying a property to rent for the long term that isn’t a speculator either. So are you a Bull or a Steer without the balls to take a chance.

So what are you AG?

It’s a slam dunk investment folks. 😉

Judge orders Vancouver strata to impose $16 million levy to repair leaky condo problems

http://vancouversun.com/news/local-news/judge-orders-vancouver-strata-to-impose-16-million-levy-to-repair-leaky-condo-problems

Affordability; Houses are a very nice asset/liability to have, so long as one can afford to purchase one. To own a house in Victoria and save/invest for one’s later years, requires a very large income which, in turn, usually requires a significant expenditure of one’s life energy.

Life’s energy; If one has shelter costs of $2000/month and savings goals of $500/month and other living costs of $1500/month (food, clothing, transportation, vacations etc.), then one must divide this total by one’s after tax hourly earnings to arrive at how many hours of life’s energy is required each month to support oneself….? The young have a larger supply of such hours ahead of them than do the elderly. The value of life’s energy could therefore be better taught to the young, by the elderly (the rarer things are, the more they are valued)….ah! but would the young listen? That ability to listen and learn from those with experience is often trampled by the young person’s desire to do it their own way—-hence, such advice may as well be written on a “Sign Post in the Bushes.”

For those who are comfortable spending their life’s energy to support their choices, it makes some sense to live just as they choose. For others who earn average incomes, home ownership in expensive cities will remain elusive. In other words; they cannot afford to “buy” a home no matter what the money lenders, lawyers, family members, friends and salespeople say to them. Google Mr. Micawber’s advice to young David Copperfield on income versus outgo.

For a few people, financial independence will always trump indebtedness. For those who are not rich, yet who must drive the latest Tesla, or live in the best neighbourhoods, a well paying profession will be essential alongside an ability to be comfortable with debt. There may well be some extraordinary stresses involved with such choices(?). Thank goodness we each have the ability to make our own choices.

Remember when Bearkilla could only type one short sentence? He is still shit at math, and forgets the leaky condo crisis that still plagues this city on a regular basis. Just seen a few more in passing in the past month. Every winter the new leakers emerge. $100K kick in the nuts is not for the so called “safe guaranteed” investment Bearkilla is clueless about.

Why are Langford condos still getting price slashed ? I thought everyone wanted to buy there.

I don’t remember that at all Bearkilla. How’s the weather in Guandong today?

Rents for condos in Victoria are pretty close or at the levels of Vancouver. There is a second floor 2-bedroom condo for sale in Songhees that is rented at $1,895 a month. 1 bedroom and den (closet) in Shutters rent around $1,700 a month. Those are very similar to Vancouver rents. Older apartment buildings in the core are typically around $500 a month cheaper.

These are expensive rents for most cities in Canada and I believe a lot of this is due to airbnb’s that have driven rents up in the core. As a downtown condo owner you can either rent the suite out on a month to month basis or a daily rate and get more money. A renter now has to compete with tourists for living accommodation. And that’s why there HAS to be a 2% tax (on assessed value) for condos that are rented as airbnbs for more than 6 months of the year. The tax removes the economic incentive to gouge month to month renters but allows home owners to rent their condos out as an airbnb for a month or two while on vacation.

Hey everybody remember when bears screamed that buying a condo in this town was a sure fire money loser? Oooops wrong again bear. Why are bears wrong about everything? Is it lack of intelligence?

I’m a speculator – is there something wrong with that?

I am surprised to find so many court ordered sales happening in this hot market.

I counted 10 in the core and 18 in total. Ranging from a low of $199,900 for a condo in Rudd Park to a high of $695,000 for a basement home in Gordon Head. Not all of them are bank foreclosures – just 17 of them are bank foreclosures. Half are condos and half are houses.

It doesn’t really matter how great the market has become. There are always people in financial trouble. I am just surprised that so many properties have not been able to sell before the lender has obtained conduct of sale. For every property where the bank eventually obtains conduct of sale their must be many that are in pre-foreclosure and never reported.

You’re right, I’m not quite a speculator as there is not considerable risk buying in Gordon Head (or many other places in the core, especially if you bought two or more years ago), and I don’t expect a quick profit. I expect a slow-ish large profit. So far, this has been happening.

That’s true sign post. Real estate is both an asset and a liability. This is why I never considered it as an investment. However it turned out to be a good one for us so it’s hard for me to rail against it as such anymore. Although one would be very hard pressed to profit buying crap shacks in a crap shack subdivision for almost a million. I would wait this out if I was looking to invest. Or invest elsewhere. These prices for what is gotten are pure speculation. It’s too bad because not only are rents high for SFHs they are also hard to get. So anyone looking for that to live in has added pressure to buy. $2500 minimum for a SFH now it seems. $1500 ish is the premium to own it seems….

“Sure, but owning is still cheaper in many cases.” Michael.”

Mike’s examples are always on one bedroom condos and never on houses in the core. Looks like Mike is trying to flog his own CONdo flips whenever he gets heavy on the fake numbers.

“TOTAL about $825/mth

MUCH less than $1300/mth (from the pics you might have to pay more than 1300)”

You can rent an updated 1 bedroom in my building for $830, with heat and hot water included. Not the brand new hardwood ( but that’s annoying hearing those above you clip clopping around) but new carpet/vinyl, same granite look alike counter tops etc , updated sinks/toilets/decks/windows.

Nice pump for the agent Mikey, but not the real numbers for a similar aged building.

“…….you end up with no asset….” Totoro

“An asset is something that pays you money. A Liability is something that costs you money.” Charlie Munger.

“Pity the poor fellow who inherits the farm and all its implements, for these things are more easily acquired than gotten rid of.” Henry David Thoreau

Victoria had higher rents than Montreal when I lived there 20 years ago.

As far as rent vs. buy even if renting for a hundred years is cheaper you end up with no asset – rent plus investing the difference has to be cheaper than all the associated costs and benefits of owning including factoring in approx. 4% appreciation per year on your leveraged purchase, any rental income, capital gains if any, plus maintenance,, insurance, repairs etc.

In Victoria owning has been cheaper than renting long-term for the same type of place as it is in many markets. It may be cheaper to rent if you live super cheap, have a high income, and invest the difference well.

Here is a couple who did that in TO:

http://www.millennial-revolution.com/

After some time spent meditating on the first three letters of the word CONdominium, the sensible solution will reveal itself.

Ok, an example perhaps. Far cheaper to buy the first 1 bd condo I pulled up for ~240k, than rent it for $1300.

https://www.realtor.ca/Residential/Single-Family/17795268/103-2095-Oak-Bay-Ave-Victoria-British-Columbia-V8R1E6

Let’s just say 100% financed (takes care of opportunity costs of downp):

Mtg interest = ~500

Mthly maint fee = 233 (incl H+W)

Tax = <100

Bldg Insur covered in fee (content insur about the same as a renter needs)

Util’s (heat & water incl) so extra util’s are the same for renter

TOTAL about $825/mth

MUCH less than $1300/mth (from the pics you might have to pay more than 1300)

Wow on 762 Victoria. Those are waterfront numbers for a house right next to the SMU junior school.

“Sure, but owning is still cheaper in many cases.” Michael.

He said, conveniently forgetting lost opportunity costs, interest costs, maintenance costs, taxes, insurance, utilities etc. There are many areas in Canada where buying is cheaper than renting, but Victoria is no such place at this time. To buy even a modest house in Victoria at current levels, the costs involved would pay rent for a hundred plus years. Most will not live in adulthood for that long.

Sure, but owning is still cheaper in many cases.

https://www.cheknews.ca/victoria-ranks-third-list-canadas-expensive-rental-markets-277865/

Surprising how Victoria rents are now higher than big cities like Montreal.

Victoria 1 bdrm = $1330

Montreal 1 bdrm = $1180

762 Victoria sold for $2,485,000, slightly more than asking.

Awesome looking 3600sf house, but a small 7000sf lot.

Looks like the developer paid around 700k for the original house/lot. Then spent maybe $1.1m building the house? That would mean a quick 700k profit. Does that sound right?

If you bought that house/lot today it would be more like 900k. But it looks like there is still some profit in there for the developers.

Thought this was appropriate to housing

I recall seeing recently, someone arguing that all home buyers are in essence, speculators. I didn’t agree.

I think the distinction lies in the motivation of the buyer.

You make it sound like all home owners are speculators. But that would not fit the definition of speculate.

“to engage in any business transaction involving considerable risk or the chance of large gains, especially to buy and sell commodities, stocks, etc., in the expectation of a quick or very large profit.”

source: dictionary.com

https://youtu.be/mjN3QfXU_y8

It would be amazing to see some kind of gradient map displaying land prices per square foot for each area and sub-area. Is that available anywhere?

This story sounds very appropriate for realtors over the next several months.

Trying to save face, they sold their home to ostensibly travel the world, but they are selling their worldly possessions to pay for their wedding and get out of debt.

You would think that the proceeds from their house sale would have covered all of this.

I like that it is advertised as a refreshing opportunity to live their dreams; not that they appeared to be drowning in debt and had to get out.

I think that many real estate agents who believed their own rhetoric are going to find themselves in similar positions soon.

https://www.kelownanow.com/watercooler/news/news/Kelowna/17/02/18/Kelowna_couple_ditches_mortgage_to_travel_the_globe/

From an absolute point of view, Uplands is the highest priced area BUT per square foot of house or land, it isn’t.

There are other areas that are similarly higher priced but not by square foot. I am thinking about places like Queenswood and Ten Mile Point with huge lots and larger houses. They appear to be expensive areas but actually they are not if you look at what you get for the price, they are much better value than say South Oak Bay or parts of Fairfield. I think the same goes for Rockland and Broadmead for that matter. So what appears to be the most expensive hoods by absolute price are actually not.

“Uplands has some of the lowest density and the highest land prices.”

Uplands lots are bigger and therefore pretty expensive, but are they that expensive per square foot?

Yeah, I like to speculate on them while living in them!

They sure are Introvert. It makes more sense to speculate on housing in the core.

That can’t be right. The lots in uplands are over 23,000 square feet this size of those off OB Avenue are about 5,500 and go for 1.3 million.

Wow, those are some crappy gains compared to the core.

Uplands has some of the lowest density and the highest land prices.

“Rockland, in my opinion, is cheaper because of too many multi-family having a lot of basement suites tends to eventually bring down the value of a neighbourhood”

On the other hand, surely increased density should increase land prices!

AG:

Rockland, in my opinion, is cheaper because of too many multi-family having a lot of basement suites tends to eventually bring down the value of a neighbourhood.y and too close to Fort and the druggies occasionally wander into the neighbourhood.

Housing in the core has become so boring to write about.

Is there anyone that would like to know what’s happening outside of the core?

Here are some year over year price increases for other areas

District Percentage Change

Sooke 12.0 %

Duncan 6.9 %

Malahat 11.6 %

Langford 14.2 %

Sidney 18.6 %

Gulf Islands 1.0 %

Colwood 8.5 %

AG, the one on Pemberton Rd looks good – probably the good ones don’t come up very often. I can only speak for when I was looking in that area, we didn’t want to live beside a B&B or a tall apartment building with dozens of neighbours with full view of our back yard, and so that limited our options, and maybe affects some of the values. (Duplexes/triplexes weren’t a worry)

“The market can remain irrational longer than you can remain solvent.”

– John Maynard Keynes

And…

“When I see a bubble forming, I rush in to buy, adding fuel to the fire. That is not irrational.”

– George Soros

“Ha ha – Hawk – I feel much better being a home owner than a renter”

“Someone who buys, when renting is cheaper, is betting that he will later sell at enough of a gain to make up or exceed that difference.” Alain De Botton from his book “Status Anxiety”

This is a gold nugget of an observation.

I bet you wish you still owned, so that, like Luke, you could casually check out a few open houses! But, alas, you sold thinking we were at the top, and prices have only increased dramatically since then. Oopsies!

The buyer of 920 Pemberton Rd got a nice piece of land (13,000sf) and an updated house for their $1.338m.

Can someone tell me why Rockland is so much cheaper than Oak Bay? Is it just because it’s too far from the ocean? Or because so many of the houses there are multi-family or B&Bs?

For George St, the value seems to be in the location. There are layout problems to solve to live comfortably, so I’m guessing $200k to fix those (expand the kitchen/living area, make a proper entrance, etc), if you can find the right people to do it. But at least there’s a good 7′ suite below to partially fund it (then again, have to account for potential capital gains taxes)

Built in 1912, there might be other problems like insulation, windows, etc. If those problems are fixed, it would definitely increase the value long-term. Would be interesting to see what it goes for.

Thoughts on 1337 George st?

I’m curious to what you guys think about FTHB eventually being tapped out. In my social circle, 95% of the people that have been toiling over housing have bought in the last year, many times do to FOMO.

How many more FTHB looked at our sudden rising prices last spring, then looked at what happened in Vancouver and ran to the nearest real estate agent.

Thoughts on FTHB eventually being tapped out? ( not that I think they are the main drivers of this market. I still maintain my belief it is Vancouver and foreign buyers tipping the scales.)

Michael: ‘Vancouver’s sell/list ratio sure finished the week strong. Correction over?’

or in a bull trap? Fits the mold perfectly wouldn’t you say? I’m not positive on this motion though, but worth a thought no?

Yep there’s a sold sticker

Leo, small favor, can you put a dot on the monthly disposal income for the current date as if prices had remained at January 1st, 2014 levels. I am just curious to see if it would have been the lowest point ever.

Anyone know what 762 Victoria sold for?

Still showing as active, is there a sold sticker on it?

Anyone know what 762 Victoria sold for?

Note that the OHs with delayed offers are becoming a lot more popular, so my comment about being “already sold before OH” is probably applicable more in the past than now (I don’t know what the % with delayed offers is), but who knows what the future holds, and I’ve seen downturns where none of this applies.

I go to some OH as well, they’re pretty useful to get an idea of what’s going on in the neighbourhood (to verify reports of local or out-of-town buyers, under- or over-pricing, talk to realtors) and sometimes to get ideas about our renos, eg., to decide what fixtures or finishes add long-term value and which are just personal throw-aways.

Having said that, traffic at an OH doesn’t always indicate how much a house will go for. Based on our own experience, houses were often sold beforehand, eg., at one near UVic with heavy traffic, I noticed a family sitting very relaxed on one of the sofas and talking to the realtor. Sure enough the house had already sold.

John,

I wouldn’t be surprised in the least. It’s done on stock chat boards/blogs all the time.

Zero frustration here Luke, markets eventually tank like Vancouver is and it’s only a 10 minute plane ride away, not another country and I’m in no rush.

When Victoria heads down 30% plus this blog will be in severe panic mode and probably a whole new group of happy posters of those who had the brains to sit on the sidelines.

Irrational exuberance can only last for so long when CMHC, BOC and every other financial entity in Canada and internationally, except the real estate industry, is telling you a major correction is in the works, but don’t diss those who can see through the marketing bullshit of an industry being exposed for fraud on a level never seen in Canada before.

Siskinds LLP files Securities Class Action on behalf of Home Capital Group Investors

http://www.newswire.ca/news-releases/siskinds-llp-files-securities-class-action-on-behalf-of-home-capital-group-investors-613630393.html

Canadian Mortgage Fraud Spikes 52% As Home Prices Soar

http://www.huffingtonpost.ca/2017/01/11/mortgage-fraud-canada_n_14103764.html

I wonder the same thing Hawk. I think some of them may be paid trolls.

https://youtu.be/1-CuclqT2hI

Hawk – I only went to three open houses this year, and only out of interest as two were in my ‘hood and the other was a unique house (Grandma’s house). It’s always interesting to keep an eye on what’s going on in the market, and I like looking at houses as I get ideas and gain knowledge of what other people have done right/wrong. When I mention open houses it doesn’t mean I’ve attended them as most times I couldn’t be bothered. For instance, Falkland was such an ugly house I couldn’t be bothered with that one.

You clearly have pent up frustration about selling out at the wrong time and want it all to tank so badly. Sorry about that, but it’s very likely never going to happen in the core. If it does, it happens everywhere and I’m still happy b/c I love it here. Good luck with your ongoing postings about the impending ‘doom’ that’s supposedly coming. I think it must be depressing living in an ongoing vacuum of pessimistic attitude. Now if you start your attacks on me like you do to others on this blog… it only makes you look bad.

As for Margate – I had another look and agree about the fireplace… a bit drab. Also, gardens never look good in the winter, and I haven’t looked at the house itself, and probably won’t bother – I just thought at first glance it looked good.

“Vancouver’s sell/list ratio sure finished the week strong. Correction over?”

Too funny Mike. Vancouver sales of 115 on Friday are down 35% from Wednesday’s 175. More fake news from chief pumper.

“Ha ha – Hawk – I feel much better being a home owner than a renter”

That’s funny, all the times I owned I never went chasing open houses everyday to make myself feel better about owning. I feel way better as a renter right now knowing the market has a high risk of tanking huge like Vancouver is.

Ha ha – Hawk – I feel much better being a home owner than a renter… we’ll see what Margate gets won’t we? As for the garden, some people don’t like lawns… I also feel very fortunate at my age to have 90% home equity and more than enough to pay off the mortgage. It came with hard work, and a bit of luck…

I notice: 1234 Richardson is a ‘new’ listing today – but wait – it’s not – just ‘refreshed’. Love how they put pictures of birds, flowers, and a close up of a handle from the 1950’s in there. Open house today if you want to go see what a crap box looks like!

Hmmm….I think Leo might be right with his theory that prices can only go up with these market metrics. I would have thought lack of affordability would have kicked in by now but large price gains even in the last 2-3 months.

1512 Westall listed for $575,000 November 22nd, 2016. Taken off market December 19th, 2016 without a successful sale.

Comes back to market February 6th for $559,900 and sells for $599,000.

There is no doubt our market has broken away from fundamentals…. Vancouver has proven that it can move much much further though. Houses are selling for silly prices that is undisputed. Take the May st house and Ansell. Both should be considered lot value minus demolition costs. At least the May street house has some sidewalks, is walkable to places, was cheaper by 100k and the demo will cost less. Both are crazy but Ansell is crazier.

Vancouver’s sell/list ratio sure finished the week strong. Correction over?

Wed 74%

Thu 77%

Fri 86%

http://www.robchipman.net/

I’m glad to hear that someone from Broadmead is on this blog.

There are only 3 houses for sale in Broadmead currently. And about 3 houses per month have been selling on average for the last 90 days. Ranging from a low of $853,000 for a home along Falaise Crescent to a high of 1.4 million for an incredibly nice executive style home on a selectively treed one-third acre along a gorgeous no through street.

The median price paid for a home in Broadmead over the last 6 months was $920,000 which bought a circa 1985 built 3,100 square foot home on a professionally landscaped quarter acre lot. When I think of what million dollar properties should look like – I think of Broadmead.

The sales to assessment ratio for properties has ranged from a low of 114% to a high of 145% in this executive neighborhood with the typical property selling around 126% of its current BC assessed value or $300 per finished square foot. This makes the Broadmead neighborhood good value for the money.

“2565 Margate at $1,150k, it will get offers over asking I’d bet!”

Yes Luke, keep cheering on the bidding wars to make you feel better about sinking 90% equity into your Oak Bay shack. I bet you’ll be at the open house too.

Personally it’s not worth more than $750. No back yard except a dirt garden and looks like the ancient fire place that doesn’t work.

Approximately 40% less buyers are stepping into the Vancouver market, why is that ? Because average prices are down 20% and they are waiting for lower prices.

Just like in Greenwich, the Uplands and Rockland could be house pain central. You think you know your neighbors wealth / business interests but you usually don’t.

Pain of Foreclosures Spreads to the Affluent

Rare, perhaps, but not unheard-of, as the housing industry collapse starts to claim victims among the affluent. Personal traumas like business reversal, illness and divorce play a role. There’s no real pattern, with people as diverse as builders, restaurateurs and poker players at risk of losing their homes.

Wow – a gorgeous home popped up in South Oak Bay today – at least at first glance it looks like a rare quality home that I would be all over if I was still looking. 2565 Margate at $1,150k, it will get offers over asking I’d bet!

Like Barrister I did not see many new listings, wondering where they were/are?

As for Broadmead – as a new Victorian, I was impressed by the homes up there Architecturally-wise. and the homes up there, to me, appear to be what the west coast ‘Canadian dream’ encompasses. It’s kind of quintessential there, for what desirable homes on the ‘west coast’ of Canada appeared like to me when I first moved here to BC, as a kid from the UK.

That said, when moving to Victoria late in 2015, I thought it was too far out of town for where I wanted to be and also, very dark and mossy (perhaps they left up too many big fir trees, but of course that won’t change now). Also, I think they have a lot of restrictions up there as to what one can and can’t do (and like strata’s I can’t stand too many rules) But, overall, a nice ‘hood.

I noticed the new Red Barn in Esquimalt yesterday – I think Esquimalt is ripe for gentrification and the next place on the ‘up’ for sure. It’s close to downtown and has a nice setting w/ the ocean nearby.

FrancVictorian/Barrister,

Although pricey, Greenwich looks like a disaster and getting worse even now. Since one third of the DOW move since Trump came in is from one stock, Goldman Sachs, it’s evident the recent stock market moves are not creating massive profits for the hedge fund boys.

More evidence of a stock market top as well as a housing top. Wait til Trump gets impeached soon.

These reports are from just back in the fall:

Greenwich Is the Worst U.S. Housing Market, Sternlicht Says

“You can’t give away a house in Greenwich,” Sternlicht said Tuesday at the CNBC Institutional Investor Delivering Alpha Conference in New York.

https://www.bloomberg.com/news/articles/2016-09-13/starwood-s-sternlicht-says-greenwich-is-worst-u-s-housing-market

Billionaire Capital Turns Into Ghost Town: “Home Contracts Down 80%”, Trophy-Cars Pile Up In Showrooms

http://www.zerohedge.com/news/2016-09-27/once-bustling-greenwich-turns-frugal-home-contracts-are-down-80-and-trophy-cars-pile

Kelowna certainly is in the desirable category. University, climate, new business and cheaper to live in than Vancouver or Victoria. My bet is more business will relocate there.

Hamilton was an under-priced market that is within commuting distance to TO with a big hospital and university – it was identified as an investment market ten years ago. Growth is understandable.

I don’t know Brampton or Guelph, but my guess is that they have desirable factors as TO becomes unaffordable for new buyers.

Chilliwack is growing for the same reason Hamilton or Langford is, proximity to a major center that experienced explosive price growth, but now that Vancouver is dropping it might too.

Highly desirable markets end up having an effect on outlying areas when prices jump. Outlying areas also tend to fall more in a down market and take longer to recover.

I agree rising interest rates could be a trigger for loss of consumer confidence in the market short-term and I agree “this risk has not been priced into the market”. Falling prices for any reason can be as well. It will be interesting to see what happens next in Vancouver to SFHs now that prices are down yoy – will this spread to other areas and what will the impact on Victoria be?

Prices do seem crazy and getting crazier. The theory to date by some is that this is a bubble that will burst. I’d say that is not the only option. There is also flat or slightly down for a longer period of time, like we experienced before this recent jump. And the market doesn’t go down permanently as far as I can tell.

I think Canada has many markets, many of which are not growing like the appreciation markets. We just happen to be in one of the appreciation markets and don’t forget we had years of no growth prior to this. Housing costs are insane in the states in these types of markets as well. And super-cheap and not appreciating in other markets. And even within cities in the US some zip codes are rising much faster than others.

I like how 651 Grenville has Red Barn Market in all caps. The realtor or homeowner must read this blog.

Looks like we’re already seeing the Red Barn effect in Esquimalt. Check out the description for 651 Grenville:

Totoro,

Thoughtful comments, and in some ways I can see what you mean about “desirable markets”. For that reason Victoria has historically commanded somewhat of a premium and probably will continue to. However, this should be considered in context. The phenomenon Victoria is dealing with is not just Victoria.

The periphery cities around Vancouver all are experiencing price explosions, as are the ones around Toronto. For instance, I don’t think Chilliwack, Kelowna, Brampton, Guelph or Hamilton are considered particularly desirable, and yet some of them are having even more rapid appreciation than Victoria.

Something else besides simple desirability is at work here – and the notion of certain cities being “appreciation markets” could certainly be true in a lot of people’s eyes, which is probably a part of the dynamic that feeds the positive feedback loop of “prices will continue to go up because others think the prices ought to do so”.

Additionally, the expectation of continually rising prices along with interest rates that hide the enormity of the principal you are locking into, in my view, has a role in anaesthetising people over time to the absurdity of the actual prices.

Franc Victorian:

Interesting facts, I was just passing on what I was told. My point still remains the same that some areas are much more vulnerable to interest rate increases than others in Victoria.

But I generally agree with you that the Canadian real estate market is sitting on the edge of a crisis. As a whole our market is much more vulnerable to any interest increases than the Americans. About

75% of American mortgages are for a 30 year term. Yes, I mean term and not amortization rate. The average term in Canada is about 3.7 years with about one third of mortgages coming up for renewal every year. I do not pretend to be an expert in this area but should interest rates climb up to 6% or 7% over the next three years then we might possibly be in a worse situation than the American housing crash. The situation is not identical to the United States for a lot of reasons that I am sure will be pointed out to me but that does not change the fact but that does not change the fact that a lot of people, especially first time buyers could not afford a doubling of their mortgage payments.

That’s because you DRIVE through the treed zone of Royal Oak Drive instead of walking it .. what do you call Boulderwood overlooking the city?, west side of Emily Carr overlooking the bog and the south side overlooking Galley Farms?

“Everytime we drive through Broadmead I remark on how dark and depressing it is. I think we can all agree that all the areas we don’t live in suck ”

This made me laugh – I totally agree! Well, on the second sentence anyways. As far as dark and depressing, the more people think that, the happier I am – it keeps the crowds away. 🙂

Marko:

You said a few days ago that there was a flurry of new listing come on. I was wondering in what area most of these listings are? In terms of SFH, I dont see an real change in South Victoria.

Compared to the beginning of this month, James Bay is still sitting with the same six, Rockland has two less than it started the month with. Fairfield seems to be at the same number. Oak Bay may have added one or two in total and Uplands has gone down by one listing. Fernwood has added one (actually the only one).

I am not disputing what you are saying in the least, by the way, but I am just wondering which areas are finally getting some much needed inventory?

I’m not so sure about your friend’s anecdote. Here are just the top two hits I got searching for 2008 foreclosures over there:

http://www.nytimes.com/2008/04/25/business/25foreclose.html

http://www.nytimes.com/2009/05/17/nyregion/connecticut/17forect.html

Moreover, I don’t think Greenwich is anywhere near a reasonable comparison. Median household income there is nominally more than 2x Victoria’s (~3x with today’s exchange rate), it’s the hedge fund capital of the US (if not the world) and it’s within a reasonable commute to one of the great cities, which has a GDP comparable to the entirely of Canada. Stamford, Norwalk, and New Haven are nearby as well. It’s definitely not a typical retirement destination.

It’s interesting to open zillow.com and check out prices there. I note a few things right off the bat:

1) A surprising number of pre-foreclosures (no mortgages, eh?).

2) Nominal prices are pretty comparable to Victoria based on lot / house size.

3) Prices are still well under 2007/8 peaks.

I don’t think most Canadians really appreciate how insane some of our housing costs are. And worse, we don’t collect and/or distribute enough information to clarify the situation, so it all comes down to vague opinions of what’s pushing the market, but nobody knows for sure. Is it interest rates, foreign capital, wealthy boomers, immigration, crazy leverage, FOMO, Bank of Mom / HELOCs, etc.?

I don’t know, but the fundamentals certainly look a bit unsettling to me. The only way I see this working out is if interest rates stay low in perpetuity. And that’s an enormous risk, which for some reason doesn’t appear to be priced in.

The benchmark value for a single family home in the Victoria Core in January 2016 was $616,700. The benchmark value for the same home in January 2017 increased by 24.4 per cent to $767,000.

Prices can’t keep going up like this forever, they will flat-line or drop for a while eventually, but prices can and do separate from income-based affordability in desirable locations over time. Leo’s graphs show that. We can see that desirable sub-areas of Victoria experience this at an even slightly greater rate and this is a snowball that grows faster and faster over time.

What Leo’s graphs don’t show is what happens to affordability if interest rates go back up to 4.2, never mind 8.7, which is something that could occur but might not given the impact this would have on our economy. I don’t pretend to understand all the factors that influence interest rates, but government policy is one of them. The graphs do highlight how hard it is to save up a down payment or pay off the greater than inflation appreciation our market has had and probably will have.

I think income-based affordability is a bit of a red herring. Income-based affordability works in markets that are not highly desirable – it starts getting off track in markets that become appreciation markets. Houses do become commodified and looked upon as investments in these markets so people are willing to pay more, and have more to invest as they move up the property ladder.

As far as the big bust goes, that could happen too, but appreciation markets recover a lot more quickly because they are desirable. Look at what happened to these markets in the US after 2008.

Everytime we drive through Broadmead I remark on how dark and depressing it is. I think we can all agree that all the areas we don’t live in suck 🙂

I’m in Broadmead. Personally I never understood the allure of the core, except maybe the ice cream at Beacon Drive-in. That’s good stuff. Otherwise, I avoid downtown or other nearby areas like the plague unless I absolutely cannot avoid it. To each his own I suppose…

Barrister, you’re probably right. Another point to keep in mind is that there’s obviously a population bulge with the boomers, so even if “average” life expectancy only goes up a few years, the total number of people in the “retiree” category is increasing. This demographic bulge, along with better health care, means we’ll have more people living in their own homes longer.

I still think, though, that when the economy gets rough the downturn will affect all areas, but it won’t last as long in “south Victoria”

I am not sure that the greater Victoria housing is either as vulnerable to a housing crash or as unaffordable if viewed from a different perspective.

Generally speaking, and as with all generalities there are lots of exceptions, one has to recognize that there exists almost two different housing markets in Victoria today.Areas such as James Bay, Fairfield, Rockland and Oak Bay (along with parts of Saanich (an area I will call South Victoria) are increasingly catering to an out of town retirement market. I would hinder to guess that the proportion of all cash purchases in these areas are much higher than in the rest of greater Victoria. This is significant because any major increase in mortgage rates would have a substantially reduced impact in the short run. One would expect far less house to be forced into the market because of mortgage payments becoming unaffordable or banks refusing mortgage renewals because of a lack of any equity. I have not been able to find any reliable statistics for the percentage of mortgages in these smaller areas but I doubt if many people are buying a house for over 1.3 million with only ten or twenty percent down.

In terms of affordability based on income of the average Victorian family the ratio might be more

realistically calculated if one looks at the average house price in the Westshore which is closer to 550k

rather than the average of 880k if one includes South Victoria.

Undoubtedly, what I just wrote will bring howls of protest about that I cant live in the core and I want to live in the core. it is not fair because fifteen years ago the average working person could afford to live in the core. All of which is true but the city has both grown but also has changed and it has drawn

more retires and affluent transplants from other parts of the country. I am not unsympathetic to the situation since I spent my whole working life commuting upwards of an hour in Toronto. In spite of being successful in my career I was never able to afford to buy in the downtown core. If it is any comfort, both in terms of time and distance, the West Shore would be considered living in the core.

Would a increase of mortgage rates cause a major correction in the housing market. Most definitely but I believe that the impact would be felt to a far greater degree in the West Shore than the core. During the American crash I spoke to a friend who was a stockbroker who lived in Greenwich Con.who stated that the crash had very little impact in that town since virtually no had a mortgage and new purchasers almost always paid cash. There was no forest of for sale signs like there was in Florida and California..

The season: winter. The place:

4434 Fieldmont Crt

A pretty unremarkable Gordon Head property.

List price: $750,000

Sale price: $820,000

DOM: 3

I bet the new owners didn’t require a $700k mortgage.

I really feel like it’s going to be another hot spring.

Who knows what the future holds but when $500,000 houses are selling for $880,800 unconditional and after days on the market you gotta recognize that we are in it. No way it can last. But it is happening.

@ Introvert,

While I am not convinced Victoria is in a blow-off-top, I don’t think I’d be quite so dismissive of the general premise. By nature, bears are always wrong until they aren’t. Conversely, those like you are always right until you’re wrong. That doesn’t strengthen your case to dismiss the notion of a market downturn; being correct in the here and now is just an inherent part of being on your side of the fence.

There has been an astounding growth in the amount of mortgage credit issued in our country, a lot of it in the last few years. Prices are spiking wildly in many of the urban regions, and wages are not growing in tandem. It’s not coming from wages growing or boomers; this is why we see the debt levels exploding. Canada’s housing market is not making global headlines for nothing, and the BOC isn’t speaking in broad generalities when they say “there is a crater under every bubble”.

No doubt this still has legs, Introvert. Springtime Victoria may see killer increases. But the underlying economy cannot support it indefinitely, no matter what anyone here thinks to the contrary. Victoria hasn’t suddenly been “discovered”. Our job market is good, but is not producing the kind of jobs to support a mortgage, let alone the size of one that’d be required here now.

No bubble could ever get started without legions of people saying, “what can go wrong, it won’t crash, the boomers/Chinese will buoy things, inflate the debt away, they can’t raise interest rates or we’ll all die” etc etc etc.

When the crash comes. Right. The crash that you say is coming but never comes. It was supposed to happen two years ago. Then last year. Now it’s right around the corner.

Spring is almost here. This is always such a rough time for our bitter renter friends.

February bagholders helping the blowoff top like Vancouver before the 20% plus crumble. Ignoring the warnings from every institution is detrimental to ones health. Financial and mental.

“An annual international survey rates Vancouver as the third least affordable housing market on the planet, and Victoria as the least affordable smaller housing market in Canada.

Victoria is deemed “severely unaffordable” in the 2017 Demographia International Housing Affordability Survey, which rates 406 cities in nine countries, including 35 in Canada according to housing costs in relation to one year of median household income.

See more at: http://www.timescolonist.com/news/local/victoria-is-least-affordable-smaller-housing-market-in-canada-report-1.8588407#sthash.dmYN3efz.dpuf

@Rook: Prima Strada is moving to Cobble Hill 🙂

… sign of the times!

Intorovert = charade. He’s never seen a bear market in his life,acts like a pompous ahole and will be the bigest whiner on here when the crash comes wanting the government to bail him out.

880,800…. The lucky winning bid!

That’s pretty good advice. Half of marriages end in divorce. You should protect your parents gift.

Although it is too late now to change the gift to a loan.

Similar advice for those that have a house and are about to have a lover move in. You should agree to a value for the home on the day the lover moves in or have it appraised.

Most of us have had stray cats turn up at our door over the years, best to protect yourself. Or put an X on the calendar marking 2 years less a week. Call it moving day.

$880,800

960k for that house! Argh.

Penguin, take the money as an interest-free loan. If they need it they you can repay and if anything happens to your relationship and the house is open for division of assets it remains a repayable loan… I’d be happy to help the kids this way and many parents feel the same.

“I’m a millenial and my parents have offered to give me money for a house and there is no way in hell I would take it. I just can not ethically take money from my parents who have worked so hard to earn that money and who will need it when they hit retirement.”

I too am a millenial, but I accepted cash assistance from my parents for a down payment (not for an $800k house, however). They would agree that they certainly worked hard, but the equity they built had more to do with luck and being born in a prosperous time and place. They bought a house because they needed to live somewhere. It appreciated more than they probably could have imagined. So why not pass some appreciation along?

In the spring of 2015, we bought a place; in the past year, it has appreciated, on paper at least, more than we could have imagined. This did not happen because we worked hard. We were somewhat lucky on our timing (though not as lucky as some), and then the market took off.

Our wealth is not always attributable to hard work. At least that’s my take:)

Speaking of dumpy houses selling fast. Anyone know what 3910 Ansell rd sold for?

“I would rather my parents blow their money on champagne and caviar than give it to me to buy a dumpy $800k house.”

Have you considered that seeing you in a house of your own would make them happy?

Sounds more like a man-crush, Introvert.

https://youtu.be/jRN1EOxyFK0

I’m a millenial and my parents have offered to give me money for a house and there is no way in hell I would take it. I just can not ethically take money from my parents who have worked so hard to earn that money and who will need it when they hit retirement. I don’t get how other people can feel good about this. Maybe their parents are richer than mine but I would rather my parents blow their money on champagne and caviar than give it to me to buy a dumpy $800k house.

Interesting charts Leo!

There’s a Red Barn in Esquimalt now; we know what that means for nearby real estate!

Speaking of affordability, this from the same man who said Vancouverites that complain of housing affordability should stop whining. Wow. We are in such good hands guys.

https://mobile.twitter.com/ausername/status/832716946328072197/video/1

Seems as though just about any home in Gordon Head will sell for above asking—and often way above asking.

4463 Fairmont Place

List price: $799,900

Sale price: $960,000

Not even a washer located less than one foot from the dishwasher could stop this train!

http://i.imgur.com/WZF2HOL.jpg

Yep.

I’ll probably keep calling him Just Jack, because I’m not eager to participate in his charade.

So ‘meat and bread’ and one of the ‘Pizzaria Prima Strada’s’ closed down this month. I definitely don’t know the ins and outs of both buisinesses but it seems crazy to me that a “booming city” like Victoria can’t support these buisinesses.

@Luke

Re. 515 Falkland Rd. Someone is looking to make themselves a nice ~$350k or thereabouts on that one.

SALES HISTORY (IN THE LAST 3 YEARS)

27/Jun/2014$795,000

I wonder if that’s working against the seller. Everything considered, I would expect this place to have sold by now.

Hawk: The problems here with homeless and druggies down on Pandora and Rock Bay are still minimal compared to Vancouver and the downtown east side. I should know I lived in Vancouver for 20 years. Here it is tame in comparison. Just compare murder rates. Victoria had just one murder in 2016 compared to two dozen avg in Vancouver. Vancouvers rate far below most big American cities. Not to say there isn’t increasing problems with opioids, etc, but that’s happening virtually everywhere… Also, if you go just beyond Cook St eastbound the problem appears to evaporate. Victoria is a small city not with the big city problems. Let’s hope it stays that way. Maybe the new safe injection sites will help?

Michael, for me I think that the CIBC forecast is too 1-dimensional. There are too many other factors at play with how the elderly spend their money, and how much $ people spend on health care.

I also think it sets people up for unrealistic expectations, and in a way – almost unethical behaviour. eg., boomer kids have to make some tough decisions about health care. I hope that no one would ship their parents off to an ill-equipped seniors home because of an inheritance. Spend your parents’ money on the fanciest place they can afford.

At $5k a month for 5-10 years for a good home, a good chunk of the $500k gets eaten up pretty fast.

@Hawk My new neighbours told me they did something similar. Their employer inflated their paychecks for a couple of months so that they could qualify for a mortgage, and then after they qualified their wages were reduced.

That’s data from 5 years ago. We’ll get the updated data this year in May, so we’ll see if it’s making much of a difference. It might be decades for some people, maybe a year or two for others and still others will die earlier from becoming addicted to their medication, at the end of the day, the number of people in highest mortality ranges is increasing significantly, and the death rate will increase.

Hmmm, so how many here are in this club ?

1 In 5 Canadian Homeowners Commits Mortgage Fraud, Says Top Broker

“This one disgusts me,” he explains. “but it does happen a lot in Brampton, a shady mortgage broker may completely falsify all employment documentation, and facilitate the transaction with a known person, whether through the broker channel or through a bank not on the broker channel.” He further explains “A person can request company ABC – to create pay stubs, an employment letter – and confirm via telephone that this person is gainfully employed, when they are not.”

https://betterdwelling.com/1-in-5-canadian-homeowners-commits-mortgage-fraud-says-top-broker/#_

James, these new drugs and therapies have only been introduced in the last 10 years so I think we’ll see something different after another 10 years of data.

ie., national historic data doesn’t tell the whole story of what’s happening today with low inventory of SFH & health care.

To understand the low inventory of homes & how more and more people are choosing to live in their houses productively until their 90s, we have to understand how this is possible today – and that’s through the new drugs/therapies for heart, stroke, & cancer.

Living in Victoria, with a high % of retirees, this is an important thing to be aware of in the RE debate.

Also, it IS very much an individual decision how healthy a lifestyle you lead – or what therapies you pursue. Yes there are a whole range of health issues that cannot be solved (eg., diabetes) – but some are preventable, and will continue to be more preventable in the future. (also remember that environment plays a factor – Victoria’s warm winters help the elderly avoid trouble with transportation, falls on sidewalks, snow shovelling, etc)

Mike,

Did you not listen to the end of the David Lereah video I posted ? He said the same BS right before the shit hit the fan and The Big Short kicked in. Dead people don’t stop crashes.

https://www.youtube.com/watch?v=lPnA1cnewLA

Re: intergenerational wealth transfer

Boomers to inherit $750-billion over the next decade: CIBC

http://www.theglobeandmail.com/globe-investor/retirement/retire-family/bequest-boom-will-see-750-billion-inherited-by-boomers-over-next-decade-cibc/article30283057/

It says the average inheritance received by the 50-75 age cohort over the past decade was $180,000.

CIBC forecasts the average inheritance will be higher than that, due to the increased value of assets – particularly homes.

That means the average boomer couple could have ~500k inheritance coming over the next decade. That’s alot of extra spending money for the already wealthy boomers.

We’ve gained about a year and half in terms of life expectancy after 75 in the last 30 years.

http://www.statcan.gc.ca/pub/82-624-x/2014001/article/14009/c-g/c-g-03-eng.gif

Forgot to add that, from everything I’ve seen in studies and discussed with doctors, I think that people will spend more of their own money because they’ll be living longer, and there won’t a huge wealth transfers to the next generation. I say – good for them! They deserve it.

John Dollar, I have talked to dozens of heart specialists and surgeons in the care of my parents, a friend who has a pacemaker and another who’s considering one, and make no mistake that today’s heart/stroke drugs and pacemakers are prolonging life by many years in all people that have those problems (if they also lead an active life).

Without those drugs & pacemakers (and healthy lifestyles), all of these specialists have said that my dad wouldn’t have been around for the last 10-15 years (his dad passed away in his 60s, he’s now 90). This is shown in many larger studies, eg., from Harvard:

http://www.health.harvard.edu/heart-health/treatments-for-heart-failure

“few patients lived more than five years, and most patients with advanced heart failure died within two years. Now, I see patients with advanced heart failure living 20 years.”

Note that every person’s treatment and range of problems is different, and it’s only been in the last 10 years that some of these drugs have been introduced. Also for my mom, with osteoporosis, they have new injectable drugs that will make her bones stronger, keeping her out of a wheelchair, making her more active and healthier longer.

With the first of the boomers hitting 70 last year, death rate should increase dramatically in the next 15 years. The majority of people die between the age of 70 & 85.

Here you go Luke the top 30 neighborhoods where people have bought houses in the last 6 months.

Map Area Sales, Number of

GI Salt Spring 62

SE Gordon Head 61

La Happy Valley 53

ML Cobble Hill 47

La Westhills 46

ML Shawnigan Lake 40

La Bear Mountain 40

SE Cordova Bay 36

ML Mill Bay 34

OB South Oak Bay 34

Sk Sooke Vill Core 34

Vi Fairfield West 31

Si Sidney North-East 29

Sk Sunriver 27

GI Pender Island 26

SE Maplewood 26

OB Henderson 24

SE Broadmead 24

SE Cedar Hill 23

La Thetis Heights 23

SE Mt Tolmie 22

La Olympic View 22

CS Brentwood Bay 22

La Mill Hill 22

Co Wishart South 21

SW Glanford 21

VR Six Mile 21

Vi Oaklands 20

SE Mt Doug 20

La Florence Lake 19

“Did anyone ever mention Victoria much before? ”

Since you didn’t live here before, yes, Victoria has been mentioned internationaly on a big scale since the Commonwealth Games in the mid 90’s. We just didn’t appear on the map a year ago.

It’s what happens at market tops and the industry can’t make money in Vancouver anymore so they go to outlying areas and milk up a media machine and create a new market just like brokers do from blue chips to mid caps, to small caps.

Basic marketing game to find new territory to make money and convince people they have to be there and create FOMO for the locals.

Speaking about being Scottish, there is this great butcher shop on Cook Street that sells Haggis, blood pudding through out the whole year.

I warmed some up for my daughter and didn’t tell her what it was and now she’s hooked on it. She wants to join the Can Scots and since she was born in late January it looks like it is going to be a regular Robbie Burns nights out to celebrate her birthday.

mmmmmm mmmmm good

https://youtu.be/C8l2m3_2Xjg

Resonance failed to mention the taxed out health care system here, unavailability of doctors, as well as a severe opiod crisis that is evident all over downtown.

You don’t have to stumble down to Pandora like East Hastings to see someone dying on the street or twitching out, they’re everywhere downtown. Lets not get started on the increased traffic congestion. This isn’t Petticoat Junction, it’s a big city now with big city problems.

John Dollar: If the article you are talking about is Resonance – that was free for me, and now they’re sending me emails (maybe they try to get you to pay somewhere but that never works on me). It might be ‘marketing’ but it’s food for thought now that Vancouver is undergoing a kind of correction. Did anyone ever mention Victoria much before? It seems to be getting on the radar all over the place (i.e. New York times, articles from the UK). Don’t think barely a whisper was heard about the once ‘backwater’ of Victoria in the past, besides it being ‘quaint’ or a nice place to visit. That appears to be changing…

Any Stat’s that encompass all of the CRD don’t really hold much weight when you are talking about just the core. The Westshore is an entirely different, separated place.

When one starts talking about the core, one has to consider that there are so many varied neighbourhoods even within the core itself (i.e Oak Bay/Fairfield/Rockland vs. Fernwood/Oaklands/Vic West) Each area has it’s own flavour and desirability factor for different types of people. Even Rock Bay is in the ‘core’ yet could hardly be called anywhere near desirable. It’s hard to get solid facts that separate out different ‘hoods in the ‘core’.

Modern science has not extended our life times. We wear out at the same rate as our ancestors. Most of the science has gone into correcting the problems we have caused by polluting our own environment and bodies. Or making our lives easier with a hip replacement rather than a cane.

Of course if you are Dick Cheney you can order a couple of new hearts from Chinese prisons so you can extend your lifetime. That guy is STILL alive!

But most of the reason why our average life has increased is because more children are surviving into adulthood.

If your parents and grand-parents died in their mid 80’s, it’s good odds you are going to do the same.

Of course I did have an uncle that died at 55, but he was hit by a bus.

I guess if anyone wants to assess weather they think 515 Falkland is a crap box or not, they can go see it during yet another open house 1-3pm this weekend. The price reduction doesn’t do much in my opinion they probably need to go down more, but I’ve been wrong before! (once I thought I was wrong but I was wrong…)

At first glance it doesn’t look bad on the inside, but in my opinion, quite an ugly looking house on the outside. That said, it is in a great location – but even in this market if homes are overpriced they don’t sell.