Affordability Recap

A few posts ago I dissected the CMHC housing report which still stubbornly refuses to acknowledge that the Victoria market is anything to be concerned about. I concluded that the only explanation for their report might be that affordability of single family houses is not out of line with historical norms due to our very low interest rates.

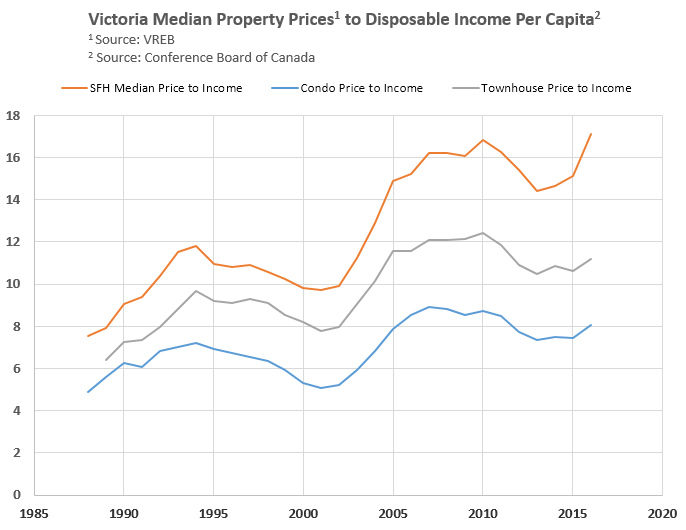

Overall this fell in line with previous measures of affordability that I’ve done using different data sets of income. But what about condos and townhouses? It is logical to assume that as the city grows it will become increasingly dense, and a greater proportion of residents will be living in higher density housing, whether by choice or necessity. Sales are currently split about 60/40 between detached and strata properties, and that doesn’t count all the pre-sales that don’t hit MLS and thus never appear in the stats. It’s safe to say that half of all purchases are for something other than a detached home.

First of all, the price to income of all property types has risen throughout the years. This is to be expected in an environment of falling interest rates. Like I’ve said again and again, people look at the monthly payment not the total price. That’s why we have a crisis in auto loans and that’s why we have a massive mountain of mortgage debt in this country.

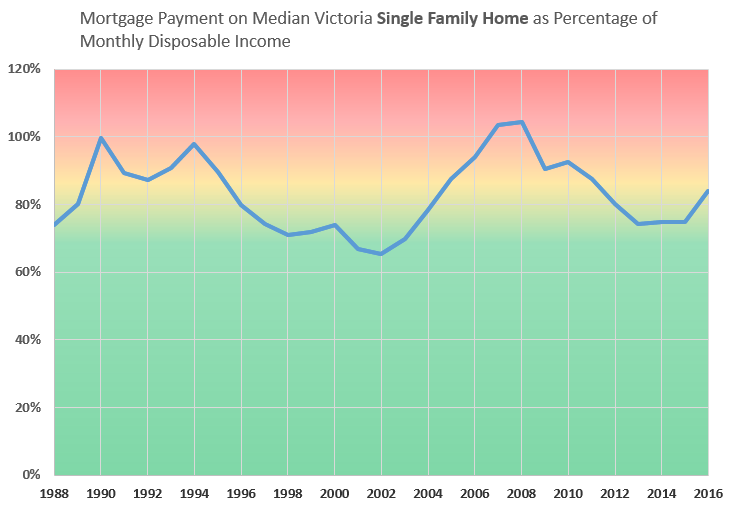

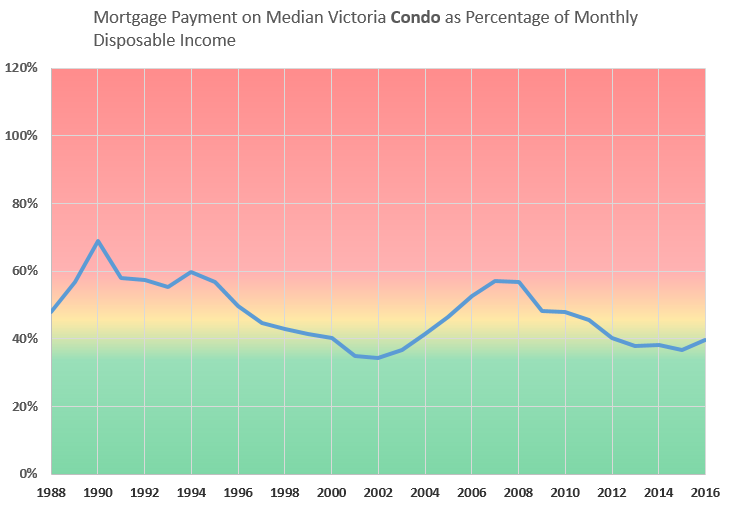

So what happens when we turn this into a monthly payment? Assuming a 20% down payment and the prevailing 5 year fixed rate of the year, here is the situation for single family homes, condos, and townhouses.

Pretty similar trend in all property types, with single family homes stretching affordability more than the other types. This is still the clearest pattern in Victoria real estate that I’ve seen. Price booms start when affordability moves into the green range, and it ends once it becomes strained for the property type (red range).

Now of course it doesn’t take into account all the factors. As Hawk points out, as house prices increase that 20% down is an increasingly large number and that can’t easily be financed. Also for condos, the trend has been towards smaller and smaller units so on a price per square foot level what you’re getting is probably less than what you could have had 20 years ago.

Now in the past the corrections have come in the form of price stagnation and gentle declines as the combination of rising incomes and falling rates restores affordability. In the future this will be quite different as rates can’t fall much further. When the next boom corrects we will either see larger price declines or need much stronger incomes to prevent it.

Just paste the link to the image in the comments, it will be automatically expanded

Also there is a new post https://househuntvictoria.ca/2016/11/16/november-14-market-update-and-the-mls-hpi/

How do I insert an image into my text?

James 5 year bonds are not controlled by the government and are independent of what happens in the US. Our bond prices are based on Canadian inflation and the growth of the economy. Our economy is one big pile of shit being managed by a bunch of morons in Ottawa. It is going no where and most likely down if all this housing manipulation works in killing the only goose keeping this economy from being total dog shit.

Hawk I would not touch housing right now. That being said I keep what I have since I like it.

“@all the bears who thought the 1.15m unit listed about a week ago @ OB/Foul Bay signalled the coming rapture, it sold for over ask. The buyer must understand the relationship between looming inflation rates & real estate ”

AKA as the greater fool. My penthouse is $1300 a month and a way better view than theirs of Save On Foods. PT Barnum was bang on. 😉

BTW Mike, high inflation with record historical debt combined with increased part time jobs and declining wage growth, cancelled building projects/ layoffs makes for real estate prices to go down lad, not up. It’s called a credit crunch. Just ICYMI.

Any practical suggestions, Oops, on the best way to short the bond market, e.g., via a short fund?

Michael

@James

BoC won’t move in step with Fed

I think that you are missing James point. Mortgage rates are pretty much determined by the bond market. As the bond market continues to sell off, albeit slower, reacting to Trumps “possible” direction it puts pressure on yields and they rise to attract buyers. This is currently happening in Canada.

When the U.S.A. raises rates in December, 90+ % chance, it will put pressure on the Bank of Canada to follow their lead. They don’t have to follow and in my opinion, won’t, but that would also put huge downward pressure on the loonie. That would create a situation where Canada would actually be importing inflation. Not a good situation as it would put further pressure on the Bank of Canada.

The bond market could become the FIRE industries biggest enemy over the next couple of years. During the Global Financial Crisis an historic amount of Canadian bonds were purchased by countries around the world, pushing yield rates to near bottom levels. If they decide we are not all that safe, watch out. Canada wouldn’t be able to purchase enough of our own bonds to stop that ugly from happening.

Pay attention to everything that could affect your life and plan accordingly.

@James

BoC won’t move in step with Fed

http://www.wsj.com/articles/bank-of-canada-says-no-need-to-move-in-step-with-fed-1479316880

@all the bears who thought the 1.15m unit listed about a week ago @ OB/Foul Bay signalled the coming rapture, it sold for over ask. The buyer must understand the relationship between looming inflation rates & real estate 🙂

“5 year Interest rates will be right back at .5 in a month as our shitty economy does sfa.” @gwac, doubtful, when the US are about to raise their rates, either Canada does the same, or people buy less/sell Canadian bonds. Either way, rate goes up.

CS should read this ….Some of what I was trying to say

When you say “what I was trying to say”, I take that as admission that you failed to say what you wished to say. I would say that there is the same problem with this piece from the National Putz.

What Trump will do, I have no idea, but if he implements a massive, Chinese-scale, infrastructure program and prints the money to cover the cost (also the Chinese way), the consequences will include:

1) A large increase in cash in the hands of working people who will mostly spend it. This is the essential prerequisite for economic growth in an economy of which 70% is attributable to consumer spending.

2) Substantial inflation, back in the 60’s and 70’s range of 5 to 10% or more.

3) A return to what our erstwhile commenter Info called “normal” interest rates, i.e., 5 to 10%.

4) Asset price collapse, i.e., stocks, bonds and real estate, and a flight from the dollar.

5) An end to the strong dollar will provide the protection that the US needs for a manufacturing renaissance.

Naturally, the globalist Putz is dead against anything like this happening.

The last thing a globalist wants is to see Americans happily making shoes and shirts, computers and car parts, furniture and floor coverings for one another rather than buying from global sources providing high profits to the global corporations that have offshored so many American manufacturing jobs.

What will actually happen, I have no idea, but the outline above of the unfolding of a possible Trump economic policy (a policy consistent with what Trump has been saying over the last 15 months) seems plausible to me.

And if that is what happens, Canada will undoubtedly follow a similar path. In fact, Trudeau was ahead of Trump on the massive infrastructure program, although because our currency is so weak, Canada currently seeks to borrow the money required, rather than print it.

CS should read this:

http://business.financialpost.com/investing/investing-pro/david-rosenberg-why-trumps-infrastructure-and-tax-cut-plans-will-pave-the-road-to-economic-ruin

Some of what I was trying to say

Mike and gwac, why aren’t you two starting an expensive newsletter for deniers of reality? Most folks don’t have money to burn buying some over priced King George shack. Bulls sounding more worried by the day. Wait til Trump actually opens his pie hole and the world markets freak.

Here you go Hawk. All these will be going for nickel on the dollar soon. Your rental days are soon over.

https://bcassessment.ca/Assessment%20Roll%20Information/Capital%20Top%20Valued%20Properties.pdf

5 year Interest rates will be right back at .5 in a month as our shitty economy does sfa.

237 king George

been for sale forever, listen to the dude in the video,

https://www.youtube.com/watch?v=UkkcWT0i7sc

still sold over assessment

Here’s where 5-yr rates (mtg rates) ended today. I suppose you could say “utterly annihilated”, but then this would be the fourth such annihilation in the past 2 years. The last annihilation saw Vic core prices jump almost 20% from Jan to May.

http://i.imgur.com/4oQx4TZ.png

Well the bond market is getting utterly annihilated, and it’s the same market forces that cause the housing market to pull back too – housing is just slower to respond. A lot of smart people think that this might be the start of a stagflation period if Trump spends and spends but doesn’t produce commensurate growth. I’m not confident that Trump will be effective.

I don’t see a lot of positives for a place like Victoria as far as local affordability goes. Among wage earners here, we’re fairly fixed-income (though that’s getting to be less the case with the software industry) and wage growth is going to lag. I’m quite nervous about the next few years, and I’m in a considerably better position than most.

Switching to the earnings-led bull will be confusing for most as it’s the opposite of what they’ve regularly witnessed since 1980. Now that we’re past the earnings trough, this earnings-led bull will see rates slowly rise and P/E ratios fall, which will be quite the flip for people.

@Michael

how many times do people need to tell you that correlation doesn’t imply causation before you stop with these stupid graphs.

http://tylervigen.com/spurious-correlations

There are some great correlations for you.

That’s in a perfect world Mike, where interest rates don’t go up and if they do wages do too , which they aren’t. More part time jobs are being created than full time and they don’t get mortgages.

The Canadian economy is based heavily on real estate and when the pool of qualified borrowers starts to dry up as is happening right now, look out below with historical debt bomb far worse than the US crash.

If you’re going to preach demographics then you can see high wage earners are slowing as the market ages. Another sign of the business/credit cycle winding down and spending is maxed out and turns to saving.

High Income Growth Is Slowing

The highest income group, those making over $30/hr, is growing at the slowest it has in 10 years. This segment grew by 2.2% over the past 12 months, not even close to the 7.8% it averaged over the previous decade. On the upside, 31% of all wages in Canada fall into this category, making it the largest group of wage earners. One year isn’t a trend, but it could be the beginning of declining high income growth for Canadians. This is likely due to maturity of the segment (i.e. there isn’t much more room to grow).

https://betterdwelling.com/tracking-the-future-of-canadian-real-estate-using-wage-growth/

I think I posted this one back in February.

Are we on the verge of another 2-year launch?..the explosive shift from monetary-driven to earnings-led. If so, any implications for RE?

http://i.imgur.com/vp40NB7.png

Thanks Marko:

Not sure if either of those properties are really within the price range of the average Victoria familly.

Had a couple significant off asking price sales today….just so I don’t get accused of only reporting those properties that go over asking.

2560 Queenswood listed at $8.25 million and sold for $7.35 million

237 King George listed at $6,488,000 ad sold for $5,650,000

oopswediditagain, thanks, I try but most won’t listen.

A month or so back I mentioned the danger of syndicated mortgages and that one was involved in a couple of places being built/planned/marketed in Victoria. Guess it was one of my “weak links” and didn’t get any response on here. Where there’s smoke, there’s fire as they say. 😉

Syndicated mortgage payments delayed

Investors in Calgary’s Orchard project have been told of delays to interest payments.

http://www.mortgagebrokernews.ca/news/syndicated-mortgage-payments-delayed-217108.aspx#.WCs73UWTqpg.twitter

“If you truly believe that this market will never go down then go ahead and encourage people to buy.”

I can only think of one person who contributes to this blog that might actually believe this. If someone buys because they believe the “market” will never go down then they must be very naive and will almost certainly be disappointed.

You can’t go wrong with the advice to buy when it’s right for you and don’t overextend.

Hawk, it seems to be getting easier and easier to find bad news on the real estate front on the Mainland.

https://www.biv.com/article/2016/11/average-greater-vancouver-home-sale-price-down-alm/

You are doing a great job of leading a lot of horses to the water.

Just Jack, I always enjoy your stats and review, as much as Leo S contributions.

Barrister, some times subtlety doesn’t resonate with a lot of people. Your imput is appreciated.

Totoro, you’re intelligent enough that I enjoy your counter arguements.

Hey guys, it’s not always about hoping for a crash so you can buy a home cheaper. If you truly believe that this market will never go down then go ahead and encourage people to buy. However, if you think that there is the potential for a hard crash, people will never forget your advice, whether it was to buy or not to buy.

I suspect the other banks will be following soon. I asked the question about the 2% rate increase over two years after talking to ac lose friend of mine who heads one of the big six banks. it was a very interesting discussion.

Agreed. If families had an extra $500-$1000 lying around our national savings rate wouldn’t be close to 0%.

I’m working on a tool that will let you simulate this.

Trust me it’s not overly fun paying $20,000 a year for daycare.

Guess they don’t need a mortgage Barrister.

Royal Bank hikes mortgage rates

http://www.cbc.ca/news/business/royal-bank-mortgage-rates-1.3851423

There have been at least three sales in the last two days in Oak Bay.

Surprisingly all over a million.

Even US house buyers are feeling the pinch of higher rates. Life ain’t cheap.

Spike in Mortgage Rates Throws a Wrench Into U.S. Housing Market

“The spike in borrowing costs in response to President-elect Donald Trump’s pro-growth agenda is causing some heartburn in America’s housing industry.

San Diego mortgage broker Shanne Sleder said a third of his clients, many of whom were already stretching budgets to buy homes in pricey southern California, are having to reconsider what they can afford as rates soar.”

http://www.bloomberg.com/news/articles/2016-11-15/spike-in-mortgage-rates-throws-a-wrench-into-u-s-housing-market

There are no houses under 800k in Fairfield now either.

As a small point of interest my house insurance went up by 4.9%. The new sewer bills also are a major property tax increase. The city separating the bill from the rest of the property tax might be a way of them pretending that property taxes are not going up but that is politics by accounting. The 75 cent Canadian dollar is effecting people more than one might think. Roofing singles apparently all come up from the US and my roofer was explaining exactly how much that has added to his costs. Multiply that by a hundred other items that we import and I am sure that the average family is really feeling it at the end of the month.

“My point was that most younger families with kids will have a hard time if interest rates go up two percent.”

That’s the bottom line Barrister. The costs of life are going up and inflation is coming back and it’s going to get ugly. Add 2% on to all of Leo’s charts and see where they end up.

It’s not just the housing costs, it’s all the other costs which have gone up. I can’t imagine having a kid again and paying $1100 a month daycare for each of their first two years, if you can even find one.

On a different note, does anyone know if the house on Pemberton finally sold and for how much. That is the one that they tried to auction. We seem to be down to 4 houses for sale in Rockland and none of them under a million.

Leo:

Actually, the 5k is not all discretionary spending, property taxes, house insurance and maintenance costs

on a hundred year old heritage house make up well over 2k of that. Some supplemental medical care makes up another portion.

The “discretionary” portion of food clothing and entertainment is actually quite low. What my point was is that the average family in Victoria would find it very difficult to deal with an increase of mortgage payments of 500 to 1000 a month. I was never suggesting that I was average or spending less than most people in Victoria.

Certainly I sympathize with young families today. Looking back to when I was a young man the biggest difference is the increase in taxes for the middle class that has occurred over the last fifty years. The average Canadian family will pay about 40% of it income in taxes. When I was a young man it was under 20%. The difference was a large part of one’s mortgage payment. Not trying to get into an sort of political debate but it does make me feel sorry for the average family. It does not impact me on the years I have left but I do worry about the younger generation. Is government spending out of control? I dont know but does the dity of Victoria really need two artists in residence at over 70K each?

It really makes me wonder how people in Vancouver are managing it where the cost of houses makes Victoria look cheap.

Probably about right. Factoring out mortgage and daycare ($2000/month alone), we spend $3250/month on everything else for the 4 of us. I would say we are somewhat frugal but not crazy.

That and being a lawyer on Bay Street, having property in Ontario that has been sold, and having, presumably, assets in US dollars having relocated from the US.

Not to say you are not good savers or your budget is not reasonable or in any way in need of modification, but spending 5k after tax a month for two people with no mortgage, kids, cell phones or car payments is not particularly frugal. In fact, it is about 1500-2000k more on discretionary spending than the average family of four in Victoria spends.

It’s all relative and I say good for you, but it will seem slightly out of touch to some people to see it self-promoted as being cost conscious and frugal.

Ento:

Neither one of us needs the calories that come with beer. For us it is not a matter of not having the money since we have assets that would let us live comfortably till at least 200 years old but rather we simply are frugal by nature. (probably why we have the assets).

My point was that most younger families with kids will have a hard time if interest rates go up two percent.

We eat out a couple of times a week but usually things like Swiss Chalet when there is a special or the occasional pub grub but even at the pub we share one beer. .

Wtf? For god sake, man, let her have her own beer!

I just noticed that the Oak Bay home on Granite street sold for 1.877 almost 180 over ask. The house looks like a boring typical 2011 new built. I am having trouble imagining why this house should be worth almost two mil. Obviously it was to somebody.

Regardless of what is happening in Vancouver, I dont think the market here is softening any.

http://www.bloomberg.com/news/articles/2016-11-14/world-s-biggest-real-estate-binge-is-coming-to-a-city-near-you

“It’s just been a trickle so far”

China’s outflow of cash is nothing compared to the expected 5 times more per year till 2022

All of it focused on smaller more affordable places in stable countries near the water.

My wife and I spend about $5,000 a month (the average median take home pay for a family in Victoria) and we are pretty frugal already). Dont have cable TV, dont have a cell phone, dont go out to movies and dont travel on vacations.Most important we dont have kids. Nor do we have a mortgage or any car debt.

Yikes! I don’t post here often (although I’m always reading this blog) but this really caught my attention. If you don’t have a mortgage or debt or cable and cell phones, then what do you spend $5000 per month on?

West Van just getting pummeled 72%. North Van down 47% in sales as well.

North Shore home sales dip towards a buyer’s market

“Six months after a red hot real estate market on the North Shore peaked at scorching highs, a dramatic cooling has sent sales into the deep freeze and prices are falling.

“We have a completely collapsed activity level,” said Realtor Brent Eilers of Remax Masters Realty in West Vancouver. “What the market’s done since Aug. 1 is dramatic.”

Expensive properties at the high end of the market in West Vancouver have seen some of the most dramatic shifts.

According to recently released statistics from the Real Estate Board of Greater Vancouver, West Vancouver sales of single-family homes between Aug. 1 and Oct. 31 of this year were down 72 per cent over the same time period in 2015, from 266 to 75 – the biggest drop in sales in the Lower Mainland. Only 22 single-family homes sold in West Vancouver in October – the same number as sold in September. In October last year, there were 116 sales of single-family homes in West Vancouver.”

http://www.nsnews.com/news/north-shore-home-sales-dip-towards-a-buyer-s-market-1.2546222#sthash.A3meRwJw.uxfs

“I have a good REALTOR® friend that specializes in New Westminster and what I am getting from him is a $1,000,000 home 3-4 months ago is definitively not going for $830,000 now.”

I’m going by what you said this morning. It looks like your million dollar place is getting slashed into the $800 range going by what I saw on a brief look through MLS.

That must have been the rare loss you posted, as Jack has been the only one to point out sales that went south.

Not quite as when you pump all the over priced sales as the new norm, but ignore the other 90% that didn’t sell over ask, but say that’s not exciting to talk about… nor factual.

I post what I feel are interesting sales…..back in 2013 it was interesting to post loses.

Marko said…

244 King George just took a beating. Sold for $980,000 a few days ago. Purchased for $1,350,000 in 2011.

Auch.

December 4, 2013 at 2:18 PM

I went on MLS for New West and didn’t take me long to find several in the $800K range that had reduced prices.

My friends sold a house in New West 5 month ago in the middle of the super hot market for $820k, I don’t think you got my point.

“70% down” is going to get a lot more interest/traffic than 39%.”

Not quite as when you pump all the over priced sales as the new norm, but ignore the other 90% that didn’t sell over ask, but say that’s not exciting to talk about… nor obviously factual.

70% down in West Side Van were legit numbers that you tried to deny in order to deflect the reality of what’s happening in Vancouver for God knows why when they were coming from one of your brethren. Overall they were down 55% for SFH’s at month end.

“As far as average vs HPI your average Burnbany/New Westminister $1,000,000 home is not $830,000. Is a $10 million home down to $8 million….probably.”

I went on MLS for New West and didn’t take me long to find several in the $800K range that had reduced prices. Based on others posted on Twitter in the $1.5 million range in East Van that were slashed $150K, a $100K range slash would not be out of the question for not too far away. I guess it’s a matter of do you believe the agent or do you go look for the facts yourself. That’s why it’s called DD.

I suspect that the average family would have problems cutting back by 500 to a thousand a month.

My wife and I spend about $5,000 a month (the average median take home pay for a family in Victoria) and we are pretty frugal already). Dont have cable TV, dont have a cell phone, dont go out to movies and dont travel on vacations.Most important we dont have kids. Nor do we have a mortgage or any car debt. We eat out a couple of times a week but usually things like Swiss Chalet when there is a special or the occasional pub grub but even at the pub we share one beer.

My point is that for the average family especially with kids there is little room to find an extra 500 or a thousand in the budget if they are carrying a mortgage. If the roof leaks or the perimeter drains clog up I suspect there are very meager savings set aside by a lot of couples.

I am not saying that we are totally frugal but we are fairly cost conscious and look for sales. Being frugal is a habit of a lifetime and i do worry about the amount of debt some people seem to be carrying these days.

Totoro: Are you a realtor, banker, broker or do you have more than google and your armchair experiences to offer?

My ballywick is hardly real estate other than my own experiences.

I was actually a CEO prior to retiring last year. Mind you, on any anonymous forum you can be anyone, however I also spent close to 20 yrs as a trustee on a reasonably sized Pension Plan, (under 1 billion).

During my time on the Pension Plan we were sensitive to the fact that the biggest contributor to GDP is the consumer and we tried to stay abreast of the many things that could impact their contribution. Obviously high debt was/is a big concern because major pullbacks in spending can easily translate into job losses and possible recession.

When the FIRE industries overtook manufacturing, mining, forestry, agriculture, fisheries, oil and gas industries combined we had to be concerned with the possibilities of bubbles and subsequent crashes. You can imagine the kind of job loss and economic downturn that such a crash would create.

Most people are quick to point out that a bursting bubble is hard to predict (see Garth) but you have to prepare yourself for that probability. Read this as tweaking investment portfolios to reflect less exposure to those sectors. On a personal level, it would mean lessening your exposure to excessive debt.

I’m not on the Plan now and I have no upside or downside to a crash but I do try to warn family and friends that they should probably be wary of the signs that could impact their lives in a big way.

Maybe I am wrong in terms of where I see this market heading but I would rather be wrong by 1 year than late by 6 months.

Plan accordingly and good luck to all.

They are posting subregions of course. SFH in Richmond for example. Vancouver is big it makes little sense to just look at the overall when the market varies so wildly.

I do agree that it is hard to judge the numbers without context. Either way, 40% declines in sales is nothing to sneeze at.

Sales are down big time, but context yet again is important. Let’s assume sales drop 40% in Victoria next year….we are down to 2014 sales levels; a year prices went up slightly.

When a 600k Gordon Head box from three years ago that is now 800k drops back down to 700k than we have a legit correction.

They are posting subregions of course. SFH in Richmond for example. Vancouver is big it makes little sense to just look at the overall when the market varies so wildly.

I do agree that it is hard to judge the numbers without context. Either way, 40% declines in sales is nothing to sneeze at.

Perhaps, because you started your career in the middle of one of the greatest bull markets in our history you are blinded to the probabilities of an ugly correction. I apologize for being hard on you. You are just as naive as the millennials that are buying today.

I started in the summer of 2010…..condo and SFH prices dropped for the next four years with unit sales volume well below both the 10 year and 25-year average. I actually really enjoyed 2013-2014.

Am I naive and could everything blow up in my face? Sure, but it’s a risk I am willing to take as I still have 35 years to recover until retirement. Worse case scenario I still have enough years left to go back to VIHA and score a pension….they still can’t adequately staff my old department (respiratory therapy).

The thing is at time passes the odds of a blow-up drop quite a bit. What I mean by that is I pencilled my first contract at the 834 in 2009 for $198,900 when Garth was calling for a complete meltdown and laughing at people buying pre-sale condos in Vancouver (check it out on YouTube). I started off with a $158,900 mortgage that dropped to $139,000 on the 5-year re-finance. The market rent on the unit went for $1,075 to $1,350 and the value of the unit went from $198,900 to $260,000-$270,000ish today.

Totoro, I have no issue with Marko’s stats on HHV, however he then wants to argue the stats presented by mainland realtors. If the median price of a home is good enough for him to present to the public then why is it all of a sudden a “bear” argument to follow his lead?

The stats I post every week have been a direct copy and paste for 6.5 years.

The stats Vancouver realtors are posting right now are just all over the place. Like sales are down 70% and then two days later the monthly sales are released and the official number is 39%.

“70% down” is going to get a lot more interest/traffic than 39%.

It would be like me one week posting stats for the core, the next week for Greater Victoria then just for the City of Victoria. You can do a lot of manipulation that way.

As far as average vs HPI your average Burnbany/New Westminister $1,000,000 home is not $830,000. Is a $10 million home down to $8 million….probably.

If the benchmark has dropped so little this probably means the high end in van is being impacted disproportionately- as might be expected. Not sure why Marko gets targeted as he is on the ground and pretty good at reporting real life in the market in victoria As far as I can tell. Are you a realtor, banker, broker or do you have more than google and your armchair experiences to offer?

Of course the Bears have used the Teranet numbers for years. They are published rates that provide a cross check to other methods of estimating price appreciation. That doesn’t mean the Teranet numbers are right or wrong.

They are not much use to me, since they’re too general. For example, if I’m only concerned with single family rates in one sub area, a single Teranet number showing the combined rate for all types and all areas is useless to me.

District Percentage Change YOY -Single Family

Oak Bay 29.5 %

Saanich East 22.0 %

Victoria 26.3 %

Victoria West 32.6 %

View Royal 13.4 %

Esquimalt 18.7 %

Saanich West 14.9 %

https://betterdwelling.com/city/vancouver/timberrr-vancouver-real-estate-selling-for-less-than-purchase-price/

Totoro, I have no issue with Marko’s stats on HHV, however he then wants to argue the stats presented by mainland realtors. If the median price of a home is good enough for him to present to the public then why is it all of a sudden a “bear” argument to follow his lead?

He should simply state that the rest of the world has no bearing on Victoria Real Estate.

Marko Juras

November 13, 2016 at 11:11 pm

According to Realtor Steve Saretsky:

So how much have sale prices changed since it’s peak in January?

Average REBGV detached house prices have dropped 17%. Median prices have dropped 16% and benchmark dropped so little we’ll call it a wash.

The bears used the Teranet index on this blog for years, now that a benchmark pricing system doesn’t show a huge drop its immediately incorrect? Ha

“Interesting how the message has changed.”

No worries, everyone can easily suck up $500 to $1000 a month. It’s free money right ? Right ? 😉

Nearly one-in-four Canadians worried about how to pay for groceries: Study

http://www.bnn.ca/nearly-one-in-four-canadians-worried-about-how-to-pay-for-groceries-study-1.607353

Ash, what agent says prices are going down while he’s trying to desperately sell a $1.39 Million rebuild ? Carrying that much borrowed money I would be using every phony number possible.

Canadian 5-10 year bonds rates went up .25 just last week, and doesn’t seem to be slowing yet this week.

(http://www.bankofcanada.ca/rates/interest-rates/canadian-bonds/)

I’d be surprised if the increases were limited to .3 to be honest.

WARNING: ANECDOTE

Guy in the bank this morning wanting to find out what happens when he sells his house and how does he consolidate all his other debt. Lending agent says “Well, you know, house prices won’t stay this high forever.”

Interesting how the message has changed.

You nailed it Oops, Marko once quoted the Vic median for an article, so that pretty much does it for his credibility.

You guys really gotta lay off Marko, he’s having way too much fun at this!

Interesting, rates going up. What a concept.

“@FIVRE604

@hmacbe @jfyfe just got text from my broker friend – “big jump in rates today”, I asked if .25? and he said some even .30″

Seems as likely as anything to me given where affordability vs. available inventory sits. Marko has been pretty balanced in his presentation of the stats as far as I can recall. No-one knows for sure what happens next. I’d agree Vancouver high end homes are a different story.

Marko, have you ever heard the term “suck and blow”. It would seem that you have no problems using the “median” prices of homes to sell.

Perhaps, because you started your career in the middle of one of the greatest bull markets in our history you are blinded to the probabilities of an ugly correction. I apologize for being hard on you. You are just as naive as the millennials that are buying today.

http://victoria.citified.ca/news/one-year-in-victorias-real-estate-buying-frenzy-far-from-over/

For the remainder of the year Juras believes available inventory will continue to slide, possibly down to a low of 1,600, while median single-family-dwelling prices will remain in the $650,000 range as they have for much of 2016. Next year, however, if inventory remains tight, prices could start to rise.

Hawk:

I really dont see any Trump fallout affecting the market right now. Besides, I am confident that our border people are able to stop any drive across the border by the US First Heavy armoured division.

The tanks would run out of fuel before they were able to figure out and fill out all the importation forms.

What I have noticed is that the number of listing of SFH in Oak Bay seem to have doubled since the middle of the summer. The number of listings is still so low that this might not be significant. On the other hand the number of listings in Rockland, Fernwood, James Bay and Fairfield are extremely low.

I have not done a scientific count; just an impression.

Sales continue to drop, so much for the hot market theory. Must be more condos than SFH’s in there. Those are probably 2 week old numbers too, heaven forbid what the next few weeks bring from the Trump fallout.

Thank you for the numbers, sales look like they will be pretty close to last year but new listings are a bit short of last year. Inventory does not seem to be building up at all. It is really looking like we will be entering next years spring market with a really low inventory number. It seems to still be a sellers market to me but maybe we are starting to see a plateau on prices.

Mon Nov 14, 2016:

Nov Nov

2016 2015

Net Unconditional Sales: 236 573

New Listings: 299 747

Active Listings: 1,834 2,952

Please Note

Left Column: stats so far this month

Right Column: stats for the entire month from last year

Thank you for the charts; they are very thought provoking. It is still really early in the morning so number crunching is a bit beyond me.

The medium family income in Victoria, according to stats Canada is about 80k a year. I did a quick calculation in my head and that seems to allow for a maximum mortgage of 400k. ( I may have miscalculated that). If you assume they have 100 to 200k cash down, this still leaves them out of the market for SFH in Oak Bay, Rockland, Fairfield and James Bay. Even in Fernwood they would be hard pressed to find anything. Even when you add in an extra 20k in income for a mortgage helper suite it still leaves the average family locked out of a large part of the inner core.

I can certainly see Markos point about two bedroom condos starting to sell so quickly. I suspect the new mortgage rules may have had a lot to do with the increased demand for condos.

I’m glad their are agents around who aren’t afraid to see what is happening in Van is precursor to the rest of BC and Canada. This economy is built around more and more fools to keep buying.

“Happy Monday Morning!

The Canadian economy- an unhealthy addiction to real estate, is now bubbling up to something truly frightening.

The similarities between our current situation and that of the United States back in 2007 is uncanny. In fact, the numbers show Canada is in a worse position.

I summarized it all in my blog post HERE. Vancouver and Toronto home prices have increased more than New York, San Fransisco, and Miami since 1998. Our FIRE Sector (Finances, Insurance and Real Estate) now makes up 20% of the Canadian GDP- this is higher than the United States in 2007 (18%).

Any slow down in real estate will immediately slow the economy. As you know, Vancouver is already slowing significantly. Sales have plummeted and now developers are putting things on hold. New home starts were down 45% last month. Toronto appears to be the last strong hold.

Time for someone to check in with BMW to see how many lease returns there’s been.

An economic slowdown and a bursting of the bubble really shouldn’t come as much surprise though when you look at the fundamentals.

Richmond, the highest concentration of foreign buyers, increased in price by 80% over the last 3 years. It’s also seen the biggest slow down since the introduction of the tax. Coincidence?

But seriously, 80% in 3 years. There’s your Euphoria moment.

The Canadian Economy, and real estate in particular is extremely vulnerable right now.

Our growth has been fuelled real estate, an unhealthy addiction which cost the United States dearly in 2008.

History repeats. Pay close attention.

All the best,

Steve”

Marko, I’m curious, you mentioned you sold 6 condos recently. Where are condo sellers typically going after they sell? Trading up to a house can’t be easy in this environment.

Two are moving up to bigger condos.

One is moving up to house.

One is moving to different investment condo.

Two are selling investment condos and not buying anything else.

The bulls constantly used the average price chart all the way up trying to justify why Victoria should play “catch up”. Now that it’s tanking it suddenly doesn’t matter and it’s all HPI which has been proven to be a lagging number by 6 months or more.

$2 and $3 million houses( which is the average in Van)have been getting slashed by up to $750K or more. Those are facts. Eventually it works it’s way down to the $1 million level. Resistance is futile no matter how you pump it.

Marko, I’m curious, you mentioned you sold 6 condos recently. Where are condo sellers typically going after they sell? Trading up to a house can’t be easy in this environment.

And what will those high end places sell for now that there are no foreign buyers to buy them? The houses themselves didn’t go up in smoke.

I think what he is saying is if you have $10 million dollar homes selling for $7 million and $1 million homes selling for $970,000 the average will suffer a huge hit which can’t be extrapolated to the $1 million house.

And what will those high end places sell for now that there are no foreign buyers to buy them? The houses themselves didn’t go up in smoke.

The truth is nearest the benchmark. I’ll give you a hint why… elimination of high-end sales since the 15% tax.

I have a good REALTOR® friend that specializes in New Westminster and what I am getting from him is a $1,000,000 home 3-4 months ago is definitively not going for $830,000 now.

According to Realtor Steve Saretsky:

So how much have sale prices changed since it’s peak in January?

Average REBGV detached house prices have dropped 17%. Median prices have dropped 16% and benchmark dropped so little we’ll call it a wash.

The bears used the Teranet index on this blog for years, now that a benchmark pricing system doesn’t show a huge drop its immediately incorrect? Ha ha.

Be careful where you steer people, my friend.

People call me to save transaction costs buying and selling homes. My clients aren’t so dumb to think that I can actually predict the market. Garth hoards those winners.

The truth is nearest the benchmark. I’ll give you a hint why… elimination of high-end sales since the 15% tax.

step-by-step, here is the link: http://adage.com/article/news/housing-crisis-realtors-ads-defy-reality/123374/

Marko Juras

Problem is the average home on the coast has barely given up any of the gains seen in the last 12 months let alone the last 5 years despite slow sales.

According to Realtor Steve Saretsky:

So how much have sale prices changed since it’s peak in January?

Average REBGV detached house prices have dropped 17%. Median prices have dropped 16% and benchmark dropped so little we’ll call it a wash.

If you continue to parrot the Real Estate Boards obfuscation of the trend by falling back to year to year stats then you are either out of touch or deliberately misleading people. When someone is making the biggest purchase of their lives it would be nice to know that they can rely on a professional to show them the trend.

You would have done well with the NAR in the U.S.A. The only problem is your reputation would have been shot down really quickly the very next year. Be careful where you steer people, my friend. When you tell people the truth regarding the direction of the market you can do no wrong. It’s their decision after that.

Real Estate as an Investment for Retirement

DOW: 59% increase last 5 years

TSE: 22% increase last 5 years

RE Vic: 20% t0 50% last 5 years depending on class

S&P500: 75% increase last 5 years

Stocks are more liquid and you can purchase on margin. If you put 20% down, you can leverage 4:1 on RE. If one was solely invested in the Canadian market, and you benchmarked in USD terms, you would actually be DOWN investing on the TSE. No wonder the amount of interest from boomers looking turning to real estate for income during the retirement years. Here is some of the logic around the internet justifying this strategy, not completely true, but lots of people do read it.

http://blog.reincanada.com/the-real-estate-retirement-plan-how-many-properties-do-you-need

No, I think the Vancouver market is a quite unique blend of crazy that will melt down mostly in isolation (just like it appreciated completely independently from Victoria in the last 5 years). I think we’ll see less spillover so hopefully the market next year will be closer to normal, but I don’t think it’s going to ease up enough to stop price gains.

I don’t think we’re at another plateau yet.

You don’t think the slowdown in Vancouver will move the Victoria market into a plateau?

And we just aren’t at the breaking points for affordability yet. Yes it is getting pretty stretched for single family homes (slightly worse than it appears in the chart above if you take just the latest monthly numbers), but it has been worse in the past. Condos and townhouses actually seem fine. Of course rates could be rising now, but there is enough buffer there to weather it. I don’t think we’re at another plateau yet.

Marko , when are you going back on TV and saying prices are cheaper now instead of saying a few weeks back they will flatline while you now say on Citified and9 that prices are heading up?

We make predictions on this blog at the turn of every year, review my last three years.

Deny all you want but bagholders are always the ones to say it will never happen here.

It will happen for sure, but the question is when. If the market goes up 25% and then drops 15% you haven’t achieved anything sitting on the sidelines.

In the last 28 years, the largest drop was in 1995 at 5.47% (this is after prices more than doubled from 1988 to 1994).

I just don’t see a 10% drop coming given what AG pointed out; free money, insane rental market, a 73 cent CND dollar, insane pressure on cost of construction due to government bureaucracy (people really overlook this until they go and try to develop or build a home), etc.

The odds favor that marketing flattening out for another 5-8-year period while affordability catches up again. For the market to correct significantly (>10%) I think we either need a large increase in interest rates or a combination of other factors such as vacancy skyrockets combined with a slowdown in the economy, etc.

It could happen but it’s not evident right now.

Not to mention Trump’s effects on the tech industry in Silicon Valley. It could be a disaster of massive proportions in the making and effect tech industry worldwide. Marko and the other bulls are completely discounting the sudden psychological change that can hit over night.

Vancouver average prices are down over $200K and price slashes all over. Your full of it to say nothing has changed in Vancouver. Deny all you want but bagholders are always the ones to say it will never happen here.

Marko , when are you going back on TV and saying prices are cheaper now instead of saying a few weeks back they will flatline while you now say on Citified and9 that prices are heading up?

Would be nice to see where you really stand on the record while Vancouver begins its massive decent and you claim Victoria is the safe zone of the world of higher interest rates and credit lending tightening.

I guess if I was trying to sell a $1.39 million rebuild I would say the same but that would be a bias opinion for my clients. 😉

@oopswediditagain – what’s the link to the adage.com article? I searched the website and couldn’t find it. Thanks.

Looking at those (awesome) charts, it seems clear that there is plenty more room for affordability to worsen before prices start falling. Affordability will likely worsen through a combination of higher prices and higher mortgage rates.

Honestly, I don’t understand how can anyone argue that prices aren’t going to go up again in the Spring. Find me another example in history where you’ve had the following situation, without significant price increases following soon after:

Very low vacancy rate

Very low inventory

Very low interest rates

An inflationary environment

A weak currency

Vancouver is just getting started. We are within historical affordability ranges but they are way outside of them. They were able to detach from local fundamentals for years because of massive foreign investment. Now that’s gone and if it stays that way then they have a long way to fall.

Won’t make an SFH affordable in Vancouver but it will come back to earth.

Most got into the market by the skin of their ass.

80% of buyers in Victoria are either paying cash or taking out a conventional mortgage (>20% down).

I’m not quite sure why so many people on the Island are turning a blind eye to what’s happening on the coast. Sales were dying and prices were declining prior to the recent initiatives. I try to learn from other people’s mistakes. It’s a lot less painful.

Problem is the average home on the coast has barely given up any of the gains seen in the last 12 months let alone the last 5 years despite slow sales.

As I pointed out with my example re the place in the Oaklands it was still more expensive by $2,000 in 2013 (extremely slow market) compared to early 2008 (very busy market) to purchase this home.

It seems like when the market in Victoria tanks in terms of sales we don’t see a drop equivalent to a gain when sales are strong such as this year. There is much more stickiness going down.

2012 – 5,747 Sales – Prices down 1.72%

2013 – 5,998 Sales – Prices down 0.77%

2016 – 10,000+ Sales – Prices up 15.26%

Apparently the narrative never changes. Perhaps the question should be: Would you recommend your family get into this market today?

SAN FRANCISCO (AdAge.com) — The housing bubble has burst. Almost three-quarters of a million Americans are in foreclosure. The median price of a single-family home recently fell for the first time in at least 40 years, and many are predicting it’ll drop further in 2008.

But none of that stopped the National Association of Realtors promulgating a $40 million ad campaign urging Americans to think of buying a house as a get-rich opportunity.

“We believe there’s a psychological block” to buying a home due to negative media coverage of the subprime crisis, said Frank Sibley, senior VP-communications and conventions for the National Association of Realtors.

I’m not quite sure why so many people on the Island are turning a blind eye to what’s happening on the coast. Sales were dying and prices were declining prior to the recent initiatives. I try to learn from other people’s mistakes. It’s a lot less painful.

Maybe. I think though it would take conditions beyond a rate increase of 2%. As Marko says, most homeowners can adjust their budgets somewhat and you can rent out a suite or a room. Even at the “margins” to be a homeowner means you had to qualify to start with and I’m not aware of the type of subprime lending going on here that occurred in the US where people were getting mortgages they clearly could not afford in their dog’s name.

It seems to me that a big drop in house equity combined with a rate increase and an economic downturn causing job loss could result in increased bankruptcy/foreclosure rates among newer homeowners who bought at the top of their affordability level or those experiencing disability and divorce.

I’m not holding my breath for great future buying opportunities in Victoria though.

Great graphs and commentary Leo. I really hope you are working on monetizing this. Much appreciated….

Yes on a global perspective. Higher rates are put in place because the economy on a national level is doing well and needs some dampening to prevent it from overheating.

But real estate is local. Say Trumpism improves the US economy and incomes and inflation increases there. This pushes up bond yields and mortgage rates increase.

That puts pressure on affordability here. But unless incomes are also increasing here the effect will be negative on prices, not positive. High rates don’t increase prices, high incomes and high employment does.

Maybe it’ll be different this time, but I’m with the CEO of the world-leading Blackstone Group.

“Twenty-five out of 26 times when interest rates went up, home prices went up,” Schwarzman said.

That’s exactly it. It’s the bottom few percent that are the important ones. People get into complacency by pointing out the average borrower will be OK. Yes of course they will. They always have even through the biggest crashes in history. If the average borrower was not OK that would mean that a full 50% of owners are in trouble. That would be cataclysmic. A crash happens with just a very small number in trouble.

Please show us where debt straddled families could absorb $500 to $1000 a month more and stay that way for years and years without effecting their quality of life. Canadians are used to wanting it all now. Telling them to cut back $500 plus would be like asking them to quit living.

It only took 11% of the margined to tank the US market. Millions went bankrupt is the bottom line.

Canada could not handle what the US went through as Harper propped up the margined when we should have let the market tank then.

Bond market says rates going up for years now. Not what a debt bloated country wants but will get. As per my friend’s credit counsellor friend, 70% of Victoria borrowers are on the edge of going under. Believe it or not.

$1 trillion gone: The global bond market has only seen a rout this bad twice in 20 years

“We do view the election of Donald Trump as a game changer,” said Adam Donaldson, head of debt research at Sydney-based Commonwealth Bank of Australia. “The strong bias toward fiscal expansion and inflationary policy represents a stark change to the malaise of recent years. This opens the door for the Fed to hike in December, but also more quickly in 2017 and 2018 than previously expected.”

http://business.financialpost.com/investing/global-investor/1-trillion-gone-the-global-bond-market-has-only-seen-a-rout-this-bad-twice-in-20-years?__lsa=7948-9cca

Most people could absorb higher rates. But most people also didn’t go into foreclosure in the US crash. It’s what happens at the margin that matters. How many people are living at the margin in Victoria and would be forced out with a rise in rates?

“And hard pressed is fairly subjective. A family having to scale down $100/month phone plans, $150/month worth of Telus or Shaw, stop eating out, etc., is not hard pressed to come up. Just eliminating a few luxury items.

The new stress test also basically has these potential 2% built-in now as well.”

So a 2 point higher 6.6% stress test once rates return to normal in a couple years is not going to be a big deal ? You need to do some math. You’re only getting the high demand due to low inventory and nothing else. By early next year this will be a whole new market.

Phone and cable are not luxuries, it’s how people function in the real world. It’s their entertainment to stop them from going out and blowing more money. You have it ass backwards.

“If you have any sort of financial discipline you would be fine as your suite now generates an extra $300 per month so you are only out $200 or so.”

You obviously live in a fantasy world where financial discipline is not happening or the household debt levels would not be at historical highs and climbing so far beyond the US crash it’s a joke.

Not everyone has a suite, nor the room to make huge adjustments. Most got into the market by the skin of their ass. Any changes they make or job losses will effect the local economy as they cut back spending. Did you not take Economics 101 ?

Keep pimping, I mean pumping the market and pray Donald doesn’t jack the rates bigtime once he turfs out Yellen in January. It’s inevitable he does, the bond market just told you that in spades.

When you factor in double the rent and inflation this home is cheaper now than in 2008.”

You’re factoring in high rents to stay or increase and interest rates stating near zero, ain’t gonna happen.

More rentals showing up in the core than in awhile. Like in 2012 when the landlords had to give away months free rent to attract. Our landlord was offering up cash to find tenants. Nothing is forever.

Has your $1.39 million box sold yet ?

Thanks! Fixed.

Excellent graphs. Two of the graphs indicate ‘condo’ rather than one being ‘townhouse’.

A home in the Oaklands sales history

Yesterday – $830,000

2013 – $575,000

2008 – $573,000

Interesting reading the notes regarding the suite

Current – (suite currently rented for $1600 fully furnished)

2013 – Tenant month to month $1150(incl utility & basic cable)wld like to stay.

2008 – The 2 br suite is currently rented for $800 per month & this long time tenant will love to stay!

When you factor in double the rent and inflation this home is cheaper now than in 2008.

Most average income families would be hard pressed to come up with half of that and that’s the reality.

If you have a $500,000 25 year mortgage at 2.5% and it goes to 4.5% that is an extra $500 per month. If you have any sort of financial discpline you would be fine as your suite now generates an extra $300 per month so you are only out $200 or so.

And hard pressed is fairly subjective. A family having to scale down $100/month phone plans, $150/month worth of Telus or Shaw, stop eating out, etc., is not hard pressed to come up. Just eliminating a few luxury items.

The new stress test also basically has these potential 2% built-in now as well.

In the last three weeks I’ve listed 6 condos; three 2 bed 2 bath and three 1 bed 1 bath.

The demand on the 2 bed 2 bath is absolutely insane compared to the 1 bed 1 bath units. I had over 100 people through an open house yesterday on a condo on Fort Street. We ended up with 7 offers last night and it sold unconditionally.

The reason I personally think the 2 bed 2 bath units are seeing huge interest is they are more livable, less investor like and a lot of buyers have been squeezed out the single family home market due to combination of prices and recent stress test. The buyer squeezed out of SFH would drop down to 2 bed 2 bath condos, not the 1 bed 1 bath.

As per that previous debt article, the average $500 to $700K mortgage most seem to be taking out in Victoria to be a SFH owner, the leap of 2 points which is more the reality in a couple of years ( as per Trump’s inflationary/higher interest rate rise/NAFTA rip up), will add $600 to $1000 more a month depending on what down payment you had. Most average income families would be hard pressed to come up with half of that and that’s the reality.

Toss in a higher stress test level of 6.6% and with Canada’s economy about to take some major hits and you can bet the banks are preparing bigtime for massive changes to lending to joe average for an over priced shack.