May Update

Another month another record run of sales. This will be the last sales acceleration before we start to wind down for the fall, but with inventory dropping for weeks now, we are entering into completely uncharted territory. Residential months of inventory is down to 1.5 which is lower than it has ever been.

Looking at the price trend, it’s not surprising that prices are going parabolic. Teakwood listed for $700k going for over a million, and Torquay being flipped after 8 months for a $400,000 uplift. These sales are the exceptions that get talked about, but the medians for the market as a whole are also heading up. As always, the key is to look at the trend as a whole and not get lost in the minutiae of month to month variations in medians and averages.

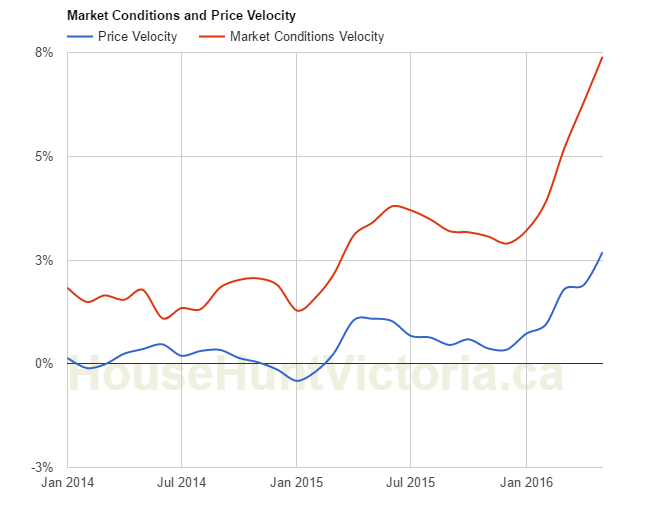

We can look at the price velocity of the graph above, and see that both for market conditions and prices, velocity is accelerating. This means that the rate of price gains is accelerating, as well as the rate that market conditions are tightening.

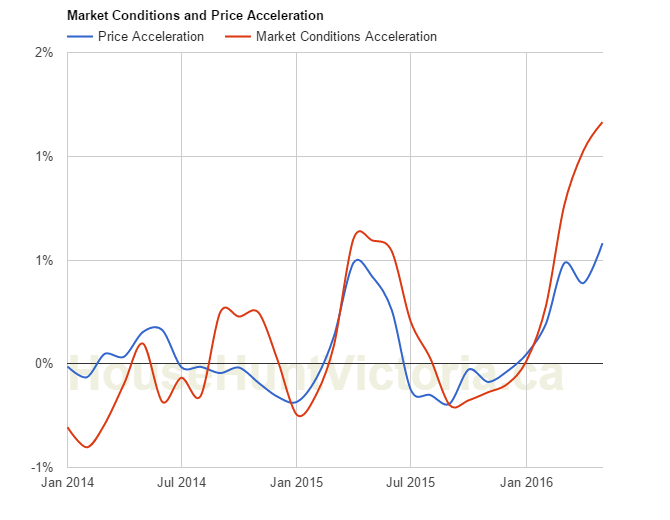

Taking the derivative again to get acceleration over the last quarter, we see that even there we are continuing to accelerate monthly gains.

How much are detached prices up? Depends on how you measure as usual, but about 15%.

The VREB still doesn’t really know what to think about the current market. Mike Nugent, their president, said: “There are influences in the marketplace that we do not fully understand yet, like the impact of out-of-town buyers and millenials moving into the market, and the seemingly sudden international attention our island city has started to receive. And some folks may be buying now because they are concerned that the market is going to continue to increase in value.”

I have definitely seen the people panicking about the market and trying to grab what they can before it moves out of reach. Looking at open houses and what drives up to a million dollar house, these are not wealthy out of towners in Bentleys. It’s ordinary people with ordinary cars, ordinary families, and dreams of owning a house. Fewer of those are coming true, with detached sales in May actually down 9% over April.

What are those ordinary people doing with house prices off the hook? They’re going into condos. Back in March I said there was still a brief opportunity in condos before the disease spread to there, and sure enough, there has been a huge increase in condo sales in May while prices have regained the peak of 2010. More on this later.

What’s next for the market? I think we are done with breaking monthly records for the year, but whether that means it will be any less competitive, I’m not sure.

Edit: For those who missed it in the comments, this Vice video posted by Hawk on Vancouver real estate is worth a watch. Remember the site crackshackormansion? Seems positively quaint now to imagine a vancouver house selling for a mere million dollars.

I didn’t miss your point. I was just being polite.

@Just Jack – I think you may have missed my original point which was simply this: sticking a new house on an existing lot in Oak Bay (except of course those that are not included in analysis which may be some but not all) increases the land value portion of tax assessments for everyone in Oak Bay (assuming the new build sells for an exceptionally high price, which all seem to do, but not so exceptional as to be kept out of the analysis).

Anytime you speak of new housing, you have to wonder about the GST.

I don’t consider the way GST is charged on real estate to be fair to everyone. Politicians have screwed around with how the tax is applied to the point that developers and contractors have found ways around the tax using rebates.

The appropriate amount of tax is paid. There is no problem with that. Otherwise the CRA would fine them big time. But what happens is the declared price the property is purchased at becomes inflated. The purchase price does not reflect any rebates. No one complains because no one loses money. But it corrupts the data that a lot of people use to do analysis. And the developer can show that all of the properties are selling at full price including GST.

And the banks lend on the value of the property including the GST. Not because this is market value but because of lending regulations. It has gotten so bad, that some lenders will not allow more than one comparable sale to be a contract price in the same building in an appraisal report. And the lenders are asking for four comparable sales now.

The last new complex I was in, the agent said to wait and she would print the latest sales in the complex. I told her not to bother because I would not be using any of them. If the purchase price can not be supported by sales in other buildings then it isn’t at fair market value. Her jaw almost hit the floor. A contract price does not mean the property sold at market value. Every contract price has to be tested against the market or you should not use it any analysis.

Weekly update up: https://househuntvictoria.ca/2016/06/06/june-6-market-update/

Thanks to Just Jack for sending the numbers.

A wee joke… guess it fell flat… just like the market is about to do before it tanks ; )

Your suspicion would be wrong. Again, because you missed the point. The assessed value has to be fair and equitable to other properties that have sold. It isn’t because the sale price is high or low.

BC Assessment is fully aware that sometimes people pay too much or too little for a property. They won’t continue that error into the assessment rolls.

If you have a net worth of $700k and inherit $300k you = millionaire.

“750,000,000,000! That means millions of ~60yr old retiring boomers are about to become millionaires”

2 million boomers x 1 million $ = 2 trillion…. not 750 Billion… That makes your exaggeration factor on this data … 2.66.

Now if I apply this factor to your optimism about the current bubble one can assume that you actually agree with me… this market is about to tank.

If BC Assessment deems 901 Hampshire to be unsuitable for analysis then we should be able to confirm that at some point correct? My suspicion is that exceptionally low sell prices get thrown out while the exceptionally high prices stay. Just a hunch 😉

“That is not true in the slightest. Victoria/Vancouver pays so much less.”

Disagree – show me where you’re getting your data? The info I have (from Towers Watson/Watson Wyatt and people in the industry) shows they’re about the same, but of course it depends on your position, experience and the company you work for. Vancouver/Victoria startups can’t always compete with Microsoft. Even Google software engineer salaries for Vancouver & Seattle and you’ll find it.

Now …. Gregor Robertson warns Vancouver’s economy at risk due to housing prices

http://www.cbc.ca/news/canada/british-columbia/gregor-robertson-luxury-tax-flipping-tax-1.3617636

“On Sunday he released a statement amplifying his support for a house flipping tax as a measure to reduce speculation and a luxury sales tax.”

“First and foremost, housing needs to be for homes, not just treated as a commodity.”

“‘These trends are not sustainable and we need to be wide awake to the risks they pose to the stability of our economy, let alone the impact they have in pushing local residents, especially young people, families, and seniors, out of our neighbourhoods,’ said Robertson.”

That’s the problem with real estate prices that are out of whack with people’s salaries – it affects the general functioning of the economy. Even if boomers/millennials inherit $180k (as in BNN article), that’s not going to pay for home to raise their kids in.

“True, if we’re talking about international investment. If we’re talking relative to local salaries, then Seattle is still cheaper, eg., a typical software engineer’s salary in Vancouver/Victoria is same number as it is in Seattle, they’re just paid in different currencies. (as LeoM pointed out it’s also important to compare neighbourhoods)”

That is not true in the slightest. Victoria/Vancouver pays so much less.

If there was any doubt that our retirement city will rocket higher over the next decade…

Canada’s Boomer generation to inherit $750-billion over next decade

http://www.bnn.ca/News/2016/6/6/Canadas-Boomer-generation-to-inherit-750-billion-CIBC-.aspx

750,000,000,000! That means millions of ~60yr old retiring boomers are about to become millionaires, if they weren’t already.

Jetpack comments spontaneously broke. Had to disable them which means no more wordpress.com logins for the moment. You can continue to comment using the basic comment form (which may be better in the long run anyway as it doesn’t depend on a third party service to be working).

Investigating some commenting issues… If I don’t see any comments here in a bit I’ll assume it’s broken for everyone else too.

@AskWhy,

You answered the question when you mentioned the split would be ridiculous. BC Assessment would just consider the sale at 901 Hampshire unsuitable for analysis.

The sale would probably not used to determine values in the neighborhood as it is a statistical outlier. The purchase/market price would not be considered at fair market value.

Essential to the assessment of properties is that the assessed value must meet the test of being fair and equitable to other properties that have sold.

When you look at all of the sales within a half kilometer radius that have occurred over the last five months it is obvious Hampshire is well above the curve of market value on a price per square foot of finished floor area rate even after accounting for newness.

Then there is the issue of the GST which amounts to some $117,000 on this sale. BC Assessment does not include taxes such as the GST or Property Purchase Tax in the calculation of actual/market value.

In the end, the sale would most likely be marked as being unsuitable for sales analysis and not used in the calculation of property values in the area.

That international migration number was a major drop of 40% from previous year numbers as well. Keep pumping Mike, someone might buy your flophouse in Vic West.

“Net international migration was again the key drag on population growth, which fell to 11,100 persons during what is typically the most active quarter for migratory gains. This marked a 40% drop from the same quarter in 2014.”

Great chart Mike, most of the newcomers have no jobs, many from Alberta low skilled manual laborers, some may be down in tent city by now.

Meanwhile all the doctors, anesthesiologists, and other professionals we need that are in major shortage are moving the other way due to out of control cost of living.

Looks to me like the Feds will implement currency restrictions on the banks, it’s the only way to control the beast that will eventually blow this up.

Meanwhile renters live happily watching the gong show time bomb tick away.

Confessions of a committed Gen Y renter: ‘It’s exactly what I want’

“Personal finance orthodoxy says that renting is throwing your money away and that buying means building equity in an investment that will rise in value over time. This is the weakest of oversimplifications, but let’s say you believe it. How can you reconcile the financial benefits of ownership with the fact that housing is so overheated in some spots that the chief executive officers of two banks last week called for the government to cool things down?”

http://www.theglobeandmail.com/globe-investor/personal-finance/genymoney/confessions-of-a-committed-gen-y-renter-its-exactly-what-i-want/article30280991/

@ash I guess they are on the extreme eccentric side. I recall the article mentioning health challenges with the wife which would have been their priority. But 2 good incomes, with DB pensions would mean good cash flow, low risks. Their car situation was similar re: eccentric. The retired prof seems like a guy who is satisfied with life and proud of his grown kids – so what more can a person really need?

Newcomers often lease for a year before buying, so the market should remain jalapeno hot for the rest of the year.

http://i.imgur.com/klLmW8S.png

LeoM,

Desire is an emotional urge. FOMO is fear of losing that chance and of being priced out forever. That fear has been proven to be bullshit for the last 40 years. Mr. Market always takes care of that and the market corrects severely or out right crashes. The odds of that happening have never been higher.

Buckets of cash is a myth and is all margined leverage from other margined deals. It’s nothing but a massive ponzi scheme. Economics 101.

I would think that a new build replacing a junker in a neighborhood that’s gentrifying would contribute to higher land values for surrounding properties. Say if an abandoned eyesore shack in fernwood is replaced by a luxury new build.

The G&M articles about the $2m crack shack in point grey seems odd to me. They rocked the property ladder in Van for a few years, working up to the best neighborhood in the city by ’83. Then completely neglect the place from top to bottom for decades?

“We weren’t worried about getting the gutters cleaned or getting the roof done. But my sons are immensely successful.”

Huh?

They seem like cool people and all but I still can’t make sense of it.

New builds in place of tear downs raise land values when the sell price is exceptionally high like 901 Hampshire. The reason for this is that the tax assessment has to assign a reasonable amount of the sell price to the building and the rest to the land. With 901 Hampshire the land and property cost <$600k before the tear down and new build. Therefore the land value wouldn’t, and couldn’t, be assessed at any more than the total price. Now that the new build has sold for a price of $1.79 Million that amount will be split between the land and building in the new tax assessment. Even if the building value is assessed very high, let’s say a million dollars (which would be ridiculous), that still means the land is now assessed at $790,000. These changes get factored into BC Assessment’s next tax assessment calculations and everyone’s land value is potentially bumped up accordingly. That is one reason why a lot of tax assessment’s in Oak Bay jumped up significantly between 2014 and 2015; tear downs / new builds bought for exceptionally high prices. I believe those tended to be on larger lots and didn’t affect smaller lots as much. 901 Hampshire may introduce a new dynamic.

Michael said; “Keep in mind LeoM, most Canadian cities has been dead for a couple years. Wouldn’t it be more of a migrational boom?”

Migration is likely one part of the equation, but only one small part. As someone else mentioned, it’s a perfect storm of desire to own real estate. Everyone wants in for their own reasons. Millennials want in because they are starting families, anyone who already owns a home who can scrape together a 20% downpayment wants to be a real estate investor, wealthy want in to get a better return than a savings GIC, foreign folks want in because they have buckets of cash, launders want in to convert ill gotten gains to legitimize, immigrants want in because real estate represents security today just as it did for the Italian and Portugese and Chinese immigrants of 40 to 70 years ago, I want in again but I’ve already cashed out my last rental property, and Hawk wishes he never cashed out so early. It’s mania as Marko has said many times. And one final word of wisdom: Hawk only needs to be right once but all the paper wealthy people need to be right every month until they sell and if everyone decided to sell simultaneously then it will be chaos for the lemmings.

Doesn’t make any sense to me. Sure any higher sold price will raise land values, but a new build won’t by itself.

@askwhy you have got me thinking about land values with your comments on 901 Hampshire. Is that true, that a new build will increase land values of the houses around it? Why doesn’t the land value remain the same when a new house is built?

Sure Vicinvestor, everyone is loaded to the tits with nothing to do with their boat loads of money and Victoria is the only clean place left on earth. Meanwhile 100’s of junkies and mental health cases invading the city by the day and nothing is done. The homeless capital of Canada. Keep on pumping bud.

@Hawk: yeah I’m sure the foreigners, retirees, & cashing-out vancouverites have no cash languishing. Come one dude, Victoria = best place in Canada for quality of life. It’s not just easy credit.

Seattle is a world class city with major sports teams,concerts ,real tech and a major port. Victoria is a small city isolated on an island. There is no cash “languishing”,it’s all easy credit in a bubble which can blow up at any time.

AG,

Did you go knocking on every door ? I see Chinese in Oak Bay without even trying.

“To an american with stronger currency that’s about the same to buy the average Seattle as Victoria. ”

True, if we’re talking about international investment. If we’re talking relative to local salaries, then Seattle is still cheaper, eg., a typical software engineer’s salary in Vancouver/Victoria is same number as it is in Seattle, they’re just paid in different currencies. (as LeoM pointed out it’s also important to compare neighbourhoods)

… which also makes a strong case for what we’ve all been saying – that real estate is now more global than local.

To an american with stronger currency that’s about the same to buy the average Seattle as Victoria. LeoM makes a good point, Clyde Hill averages over 2M US$ and I don’t think as nice as Oak Bay.

Keep in mind LeoM, most Canadian cities has been dead for a couple years. Wouldn’t it be more of a migrational boom?

Be careful how you compare Seattle to Victoria. Seattle has many mediocre neighbourhoods. If you want to compare the two cities you need to compare similar neighbourhoods; for example compare Clyde Hill or Mercer Island to South Oak Bay and Uplands. Zillow website has all the data on American cities real estate activity.

Seattle and other desirable coastal cities worldwide are in the same pattern as Victoria and Vancouver, blind auctions and over asking selling prices. This is a global trend to convert languishing cash into hard assets that appreciate at rates that exceed inflation.

This is the first time in my long memory when the entire world is having a real estate boom simultaneously; and there is no end in sight.

Interesting thing with the Seattle activity is that the median cost of a house in Seattle is still “only” $560k, which is $200k less than Victoria (average $760k according to June 2 TC article), of course, $1M less than those of Vancouver.

Great story StepbyStep – good example of how wealthy people often haven’t lived in flashy houses, they’ve had other priorities, eg, kids or travel or hobbies. HGTV has been an amazingly effective propaganda machine 🙂 and in some circles (eg., if you’re a CEO or property developer) you have to “prove” your success for business reasons, but often it’s not necessary

http://bottomlineinc.com/millionaires-have-big-houses-and-fancy-cars-right-wrong/

Then again, at least people in the 80s/90s had a choice of whether to spend $ on fixing up a house – nowadays they can barely afford the house.

901 Hampshire was a new build so presumably the $585k price last year was for the tear down. New builds in Oak Bay typically fetch a significant premium. My issue with this is that the value of the land portion of everyone’s tax assessment gets hiked up proportionally. In others words, even if your property is located somewhere would it would never be a prime candidate for a tear down / new build it still gets valued as such for tax purposes.

There is definitely an increase of HAM. Teakwood was HAM. But much less prevalent than Vancouver.

@Hawk

I think it’s far more likely to be Vancouver exiles. I’ve hardly seen any Chinese around Oak Bay.

Sounds like dirty money moving into Oak Bay. No one can be that stupid.

Ghost Bay will be the new tag as your neighbor goes AWOL for years as the papers pile up and the grass grows knee high.

Anyone know who bought 901 Hampshire? Seems like an insanely high price..

That one sold for 585k late last summer.

Nice story – when real estate was about homes and raising families and other priorities and not granite, stainless steel, etc. Note that parents helped them get into the market in the ’80s.

http://www.theglobeandmail.com/real-estate/vancouver/the-story-behind-vancouvers-24-milliontear-down/article30278810/

This weather is going to cause an absolute buying frenzy. Mainland Chinese love hot weather.

901 Hampshire Road sold for 1.785m before it even got listed. 5600sf lot, 2100sf living space. Only 3 bedrooms! It was going to be listed at 1.6m.

If it cost 500k to build, that pushes the value of a 6000sf South Oak Bay lot to about 1.25m I reckon…

Very similar stuff happening just southeast of us, in Seattle:

Bidding wars: Homebuyers fight to pay more for Seattle homes

Across the Seattle metro area, about 75 percent of home sellers have received multiple offers so far this year. That’s pushed the majority of homes to sell above their list price, and has left many buyers frustrated and shellshocked by a process that’s often swift and secretive.

In today’s ultracompetitive local housing market, there are now more home-bidding wars than at any point this decade. The result? For the first time during the economic recovery, the majority of homes are selling for above the list price in Seattle and surrounding cities.

And, Just Jack, don’t nod off; this will interest you:

Tapping into buyer frustration over what can be a secretive bidding process, startup businesses have even been launched to address the phenomenon, including Kirkland-based Faira, which offers transparent eBay-style online auctioning of homes.

At Faira, the founders went through frustrating bidding wars themselves and wanted to open up the opaque process by posting bids publicly online. That way rebuffed bidders would know whether they lost a house by $10,000 or $100,000.

http://www.seattletimes.com/business/bidding-wars-homebuyers-fight-to-pay-more-for-seattle-homes/

@vicinvestor1983 – thanks for sharing that quote – simply amazing. Phrased in those terms – this is an incredible time in real estate history. We are one of those people who would have sold our house in Victoria to relocate but we are completely ‘frozen’ by this environment. We are afraid to make any decision which is out of character for us. If the market crashes (anticipating Hawk’s comment) we would be able to deal with the fall-out. It’s this lunacy that has us immobilized.

The real estate industry is under attack from all sides this month; but it might be all bluster.

On CBC News:

Toronto Real Estate Board ordered to open up online sales data

Order from Competition Tribunal could have impact across Canadian real estate markets

http://www.cbc.ca/beta/news/business/treb-competition-tribunal-order-1.3616564

@SweetHome: Wow, a $505,000 increase in value! It doesn’t look like the work done could have cost much more than $100,000-$150,000. Anyone who bought a house to flip before this major upturn in prices and is putting it on the market now must be laughing.

2014-2015 assessment year increase in residential real estate price exceeded all of Vancoucer’s personal income for that time period:

https://itunes.apple.com/ca/podcast/the-jon-mccomb-show/id916861100?mt=2&i=369971243

“Now, he is a confidante of Premier Christy Clark. Not only does he help raise gobs of money for her, a lot of it from those who attend his UDI chats, but he also fills her ear with his views on the heated discussion over housing.”

As I mentioned, corruption in government at it’s worst.

Did you read the linked article: http://www.theglobeandmail.com/news/british-columbia/dont-expect-action-on-vancouver-housing-crisis-maybe-a-task-force/article30279445/

I don’t imagine anything will happen in the near term.

“Mr. Zhou said the agents who found the documents said they do not understand why investigators did not follow up right away. The complainant received an e-mail from the regulator asking for the pictures only after The Globe contacted the council on Wednesday about the matter.”

Agreed LeoVictoria, this could be a major catalyst, corruption at it’s worst. This province has gone down a very dark hole.

@Leo S From the link you posted the sad truth: “I am not surprised at all that I have not been contacted [by the council],” Mr. Bassi said. “We Canadians live in a society where there are almost no consequences to bad behaviour.”

More failures to self regulate. http://www.theglobeandmail.com/news/national/no-action-taken-on-vancouvers-new-coast-realty-complainants-report/article30279257/?service=mobile

This could very well be the catalyst to major regulatory change in the RE industry

@VicRenter – “I had my eye on 3119 Somerset as a non-view, non-prime location (within its neighbourhood – ie, not on Smith’s Hill) Hillside/Quadra house that had been fully renovated and had a suite.”

To make the price jump even worse, this house sold for $360K in December 2015. From that to $865K: talk about a flip!!

It’s not just here. My wife’s sister just sold there place. 36% over asking. In Rotterdam….

A rate hike is not happening bitches. The Obama stagnation continues and if Hitlary gets elected it will be permanent.

Lingo,

You referred to it as a bubble. Bubbles eventually pop and there is no guarantee the banks will be there to help anyone when it does. Just the opposite, they are not your friend when things go south.

The banks are still in the 5th inning (by Scotia’s word) trying to contain the oil losses. That’s alot of innings left.

Banks don’t control buyer psychology which is exhibiting classic market blow off top behavior. The US banks didn’t help anyone when it blew up. Canada is not some insulated system and the US rating agecies have us under a microscope which effects their ability to lend.

No wonder Scotia had the guts to ring the bell first,they see the serious danger in an extreme out of control market.

Many millions went bankrupt and lives were destroyed in the US in 2008, far from nothing really happened. Canada got off light, not this time.

PS Mike, shorts have increased on 4 of big 5 banks last month on a range from 20% on CIBC up to 46% on TD. Not a good sign for perma bulls.

Good post Vicbot. It’s disgusting how corrupt the BC Liberals are with all the corporations and the condo king in their back pocket. Clark will do squat which will be the end of her and her cronies.

Mike has to keep beating the dead horse of the TSX as if it was just invented in January. It’s still 1500 points off the high from 2 years ago. Gold was the only reason it’s up today as the US has wonder if a recession is coming.

The big shorts are just lining up now, they know with banks holding 50% of loans in mortgages that things could get real ugly when inevitable intervention kicks in and the bubble pops.

Hawk, what you don’t understand is that the more parties raising the “bubble alarm,” the less likely we are to see it pop. This isn’t 1929. We are far better at using financial bandaids in the form of bailouts and small policy shifts. Nobody likes precipitous dips or climbs, and regulators & lenders have become very, very good at smoothing these things out through various mechanisms and policy decisions. Nobody in decision-making positions fails to see the risk here. Realtors and speculators are the only ones pumping the tires of this alleged bubble, and they have such little influence on policy that it’s basically negligible. It might seem like realtors and speculators are driving this bus, but really they are just the ones yelling out the window. Banks and governments have a vested interest in keeping everyone, including themselves, afloat. Worst case scenario IMO is a 30% “correction” – and that wouldn’t even be a big deal for most people. The crash of 2008 wasn’t actually all that bad. 8 years later and it’s like it never happened. We are very good at keeping the world financially afloat.

I don’t think anyone is telling anyone not to buy. You buy when it makes sense to you.

In your case it made sense to you. But as you have said if you’re over leveraging or your debt service is off the chart – why do you want to do this to yourself.

And getting a gift of a hundred grand is just going to propel you into making a really bad decision.

There have been several “ballistic” sales in condos since the beginning of the year too.

But there is some commonality to the ones that have vastly sold over their government assessed values. They are located in complexes that have historically been under performing due to a bad layout, location, being in a hotel rental pool, etc.. All of them were purchased by out-of town buyers, that I assume, had no knowledge of the history of the complex or the area

In contrast I worked earlier this year with a client from Alberta that was looking to buy a condominium. I did value runs on a dozen properties that he short listed, checking into their past history for things that might limit appreciation or sale-ability.

As one poster said awhile back, this might be the market to get rid of some of your under performing dog properties. Especially condos because most out-of-town buyers are not going to know that a Money Mart is around the corner or the homeless camp under the awning at the back of the building each night. Or my favorite where an out-of-town couple bought an expensive second floor condo in a renovated building with the original single pane windows. Right along the street that the drunks parade back and forth on the week-ends in the wee hours of the morning.

That one will be back up on the market in 6 months at a loss.

@JJ: over-leveraged to me is anyone with fully borrowed down payment & housing costs exceeding 1/3 gross income. I’m in the camp that R/E risk is high at this time. The major disagreement I have with Hawk is his market-timing & predictions. I just don’t think anyone can predict market directions. Hence, if you have a healthy income & need a house to live in, no point waiting for a crash. This is because the ‘crash’ may never materialize, especially here in Victoria. But if you’re being greedy & buying based on speculation, you better be prepared for losses.

We’re professionals with a high income. We needed to buy a house to live in for the next 30 years. We decided that there was risk on both ends (boom & bust) based on multiple variables. So we jumped on an entry level luxury property that we bought close to assessment & under-asking. Although the house was more expensive than we wanted, we had 20% down & a mortgage:gross income of 4:1. I just didn’t see value in the hyped-up market of $500-1 million. A home was saw for 1.2 went for 1.6; another listed at 1.25 went for 1.45.

One has to wonder how all those ‘big shorts’ are feeling that began shorting Canada in January.

A look at the TSX since beginning of the year:

http://stockcharts.com/h-sc/ui?s=%24tsx

The herd of financial ‘experts’ certainly make it easy for the rest of us.

Yes there’s some influence from boomers helping their kids with downpayments, but that may be a reaction to the higher prices, instead of the cause.

Unfortunately I think we’re all pawns in a big game played by property developers & BC policians, which is then exacerbated by demographic shifts. It’s been so easy to predict “it’s going up!” for the last 15 years of BC Liberal rule because BC is controlled by the real estate industry.

Can’t understand why it would ever a source of pride (?) that we’re one of the most unaffordable places in the world to live compared to salaries – that makes our communities and economy weaker. Canada is most similar to Australia, and they have much stricter regulations.

http://vancouversun.com/opinion/columnists/douglas-todd-how-much-does-the-real-estate-industry-influence-b-c-politicians

“For a long time Kurland couldn’t understand why the B.C. government would stubbornly ignore polls … that capture the anger of voters, most of whom are shocked there is no longer any connection between Metro Vancouver’s wages and housing costs.”

My research shows it’s only B.C. that allows foreigners to donate to political parties,” Travis said. “I have not found anywhere else in the Western world where that happens.”

“Martyn Brown, a former insider with the B.C. Liberal government: ’No corporation, no industry, no union gives the level of money that they give to politicians without expecting special consideration in return, and they do get it.’”

In the decade up to 2016, the B.C. Liberals took in $70M in large corporate and business donations … Roughly $12M … came from the real estate industry, more than double the rate of contributions from the next biggest donor sectors, mining and forestry.”

“Two of the foreign-based property developers … are Onni Contracting … and The Holborn Group … owned by one of Malaysia’s wealthiest families, … is also building 10 residential towers on prime land next to Vancouver’s Little Mountain, which it bought from the B.C. government.”

http://www.integritybc.ca/

“Corporate & union donations to BC political parties: $60M. To federal parties: $0”

3520 Parandeh Lane… listed at 188,888,888. Seems like the market really took off today!

Wonder how much it will sell over list.

“Yeah, I told people months ago that condos were next to go ballistic.”

So how many condos did you rush and buy Mike ? None I assume, just a lucky guess.

I like BOC chief Poloz comment: “There’s a crater under every bubble.” This crater will be fricking massive.

Credit unions now calling bubble, 2 big banks calling bubble, keep your heads in the sand tho, “millions” are moving here as Mike says. 😉

The auto loan bubble will add to the housing bubble woes when it blows up soon.

US Auto loan bubble hits $1 trillion

“The auto loan bubble has gone full nut bar thanks to broke undisciplined consumers, reckless lending from dumb yield starved investors and willfully blind leaders at central banks. This report is on the US market, but similar antics have dominated in Canada and many other countries as well. The end result is a world awash in dinosaur (‘ICE’ internal combustion engine) vehicles that have been booked as ‘sales’ by auto-makers but not actually paid for that will end up in debt write-offs, investment losses and probably more taxpayer bailouts.”

http://jugglingdynamite.com/2016/06/02/us-auto-loan-bubble-hits-1-trillion/

When you say over leveraged would that mean a down payment that came from the parent’s home equity line of credit?

That’s the thing I don’t understand. If the down payment is also borrowed then is the purchase fully leveraged?

I don’t understand why people bother to mention Turner’s opinions. He has been wrong for so many years, I would say he credibility is less than zero!! Those who followed his advice have missed out on big R/E gains. The market is frothy, and, yes, the major players are now really worried. I don’t think it’s prudent to go & over-leverage or buy buncha ‘investment’ properties. However, Turner is not the ‘expert’ I would listen to. Tune him out.

Things will change when individuals believe we are seeing the last of the price increases. Then people won’t want to risk getting into the market or stepping up in price range in the market. If you are coming from a foreign country and you need a safe place for your money you may not be as sensitive to this bubble-talk and Canada will still be an appealing place because of our currency level, schools, safety, etc.

I’m fairly sure Turner was writing his bearish books as far back as the 90s warning people on real estate.

Yeah, I told people months ago that condos were next to go ballistic. May had something like a 97% increase in sales over last May. I think parts of the Cowichan valley for SFH are about to feel the ripple too.

So where should you buy if prices are flat for housing in the core.

As people are priced out of houses in the core districts they may look at buying a condominium in the core?

Condominium in the core districts.

Month Sale Price, Median

Jan $272,700

Feb $305,250

Mar $289,400

Apr $299,000

May $325,450 an 8.8% increase

Volume of sale for condominiums in the core districts

Sales, Number of

Month Sales, Number of

Jan 120

Feb 176

Mar 224

Apr 232

May 306 which is a 32% increase in sale volume in just one month.

But did the major players say that in 2001?

Didn’t ‘Turner’ say the same thing in 2001? 🙂

If you are going ignore the obvious Mike you deserve to have your ass handed to you. The major players are now saying it, the past year they haven’t said a peep. Game over.

‘We’re in a bubble’: Record home sales in Toronto and Vancouver intensify fears of overheating

“While some still only cautiously refer to Canada’s hottest housing markets as being in a “B-Word”, Ryan Lewenza says “bubble” very clearly describes the trend in Vancouver and Toronto real estate.

“I would define it as a bubble,” the Turner Investments portfolio manager said on BNN Friday morning. “When you look at the year-over-year increases relative to rents, relative to underlying fundamentals – we’re at stratospheric valuations, if you will. So I would say we’re in a bubble.”

Sherry Cooper, chief economist with Dominion Lending Centres, also told BNN she was “getting very worried… because the price acceleration is increasing.”

“These things generally don’t end well,” Cooper said”

http://www.bnn.ca/News/2016/6/3/Another-record-breaking-month-for-Toronto-housing-amid-fears-of-overheating-.aspx

Sorry Mike, your numbers are all bullshit. The party is over. Tick, tick, tick…..

It’s not ‘if,’ it’s ‘when’ Vancouver’s housing bubble bursts

“Concerns about Vancouver housing are mounting as the average price of a detached home in the city tops $1.5 million. Vancouver-based CCEC Credit Union’s CEO Ross Gentleman says the market is in a bubble. He joins BNN to discuss this, how concerned he is about foreign buyers and why intervention is needed now.”

http://www.bnn.ca/Video/player.aspx?vid=883607#.V1HOXcMgrMk

It’s not happening “through out most of Canada at the same time”, just take a look at the prairies vs. BC.

Q1 GDP = 2.4%.

But that’s the great thing about Canada eh, prairies can be in a depression while BC is rocking!

The median Boomer is only age 56-57 this year, so the greatest wealth transfer is probably from the Depression Parents who were savers to their Boomer children.

Like I said, it would have to be different this time.

Michael, there will always be a not necessarily.

Just as rising interest rates might not necessarily cause prices to increase.

Historically in recessions house prices drop. If we are in a recession, then that should have happened unless there is another factor compensating for the economy.

And again I think it could be the transfer of wealth.

Vicbot, that’s reasonable but why did it happen through out most of Canada at the same time? And It is unlikely that everyone got a substantial pay raise at the same time to qualify for a bigger mortgage.

The Baby Boomers started turning 71 this year, so I suspect it may be the transfer of inter generational wealth. Claiming an inheritance early. And that can be a lot of money but it is also spread out over children and millennial grand-children. Give to one – you have to give to all.

Not necessarily. Large corrections often occur when there’s no inflation. Examples would include times when the inflation rate suddenly drops lower than borrowing rates, and central banks can’t react quick enough in dropping overnight borrowing rates. Of course in our fiat world, the game plan is to always maintain inflation rates slightly higher than borrowing rates, ie. controlled expansion.

One of the posters wanted to know how the house sales are distributed by price range in the core.

Sales, Number of

Sold Price 2015 2016

$0 – 200 1

$200 – 300 5 1

$300 – 400 69 31

$400 – 500 201 118

$500 – 600 314 228

$600 – 700 243 239

$700 – 800 169 212

$800 – 900 82 174

$900 – 1,000 51 114

$1,000 – 1,250 61 119

$1,250 – 1,500 28 73

$1,500+ 41 91

The high end market has doubled in size from last year and that has had a substantial impact on averages and to a lesser degree medians.

I think the $100k-$200k price jump happened because of all the different lines intersecting in 2015/16 – Vancouver buyers bidding up houses after years of being outpriced (or bought out) by foreign buyers (a breaking point), the millennial wave coming onto the market with kids and needing more space than a small condo, & boomer retirees from other parts of Canada. Also, too much past focus by builders until 2008 on small condo construction.

The reason it all came together in 2015-16 is because of demographics (double whammy of millennials & boomers), low Canadian $ fueling foreign investment, and Canada’s recession, which gov’ts don’t want to admit we’re in because they’re trying to get the last squeeze out of the real estate industry.

That’s why I think it’s hard to predict what’s next – because we’re in a precarious spot with the economy & gov’t policies. Here’s a link to Conference Board of Canada’s graphs on how China’s GDP affects Vancouver real estate:

http://www.conferenceboard.ca/economics/hot_eco_topics/default/13-03-11/vancouver_housing_markets_cannot_fully_escape_the_chinese_dragon.aspx

This is the data for median prices for house sales in the core for 2013. What we had this year was not the same as 2013. This year was a seemingly an overnight explosion in house price in the core.

Month Sale Price, Median

Jan $540,000

Feb $590,000 increase 9.2%

Mar $574,750 decrease 2.5%

Apr $610,000 increase 6%

May $551,250 decrease 9.6%

Jun $585,000 increase 6%

Jul $570,000 decrease 2.6%

Aug $556,100 decrease

Sep $575,000 increase

Oct $579,500 increase

Nov $555,500 decrease

Dec $571,750 increase

Just so that we can compare apples to apples

Sale Price, Median detached houses in the core

Month 2013 2014 2015 2016

Jan $540,000 $576,250 $542,500 $655,500

Feb $590,000 $579,000 $597,500 $681,500

Mar $574,750 $568,950 $625,000 $740,000

Apr $610,000 $599,450 $631,200 $758,000

May $551,250 $609,450 $620,250 $760,450

Jun $585,000 $583,000 $629,450

Jul $570,000 $576,000 $610,000

Aug $556,100 $595,000 $659,500

Sep $575,000 $585,000 $640,000

Oct $579,500 $570,000 $677,250

Nov $555,500 $569,000 $620,550

Dec $571,750 $561,250 $672,500

And here are the averages

Sale Price, Average

Month 2013 2014 2015 2016

Jan $572,096 $638,272 $619,555 $736,731

Feb $700,293 $631,135 $665,536 $776,810

Mar $630,782 $697,516 $705,337 $857,915

Apr $733,764 $701,092 $698,202 $883,311

May $637,494 $681,651 $703,989 $890,941

Jun $682,160 $645,682 $719,005

Jul $638,435 $656,549 $781,363

Aug $652,905 $689,180 $812,136

Sep $635,213 $673,535 $706,817

Oct $651,472 $630,884 $794,051

Nov $615,849 $643,875 $708,030

Dec $668,663 $637,256 $826,360

And when I regrouped the data into blocks of 500 sales the data showed the seemingly overnight explosion in prices more clearly in that 16 day period from Feb 20 to March 7.

01/22/2015-04/12/2015 the median was $615,000

04/13/2015-06/06/2015 the median was $630,000 for a 2.4% increase

06/07/2015-08/14/2015 the median was $629,000 for a 0.2% decrease

08/15/2015-11/05/2015 the median was $655,000 for a 1.0% increase

11/06/2015-02/19/2016 the median was $650,000 for a 0.7% decrease

02/20/2016-03/07/2016 the median was $742,000 for a 14.2% increase

03/08/2016-04/18/2016 the median was $751,000 for a 1.2% increase

04/19/2016-06/02/2016 the median was $755,000 for a 0.5% increase

Really not that unusual. Average SFH price increased 11.89% from Feb to March 2016.

Other big changes:

Dec 2015 13.34%

Nov 2015 -11%

Jun 2013 12%

May 2013 -13%

Apr 2013 12%

Feb 2013 13%

Jan 2013 -11%

There definitely seems to be times when average prices are more volatile while other times they are more steady, but big jumps are not unprecedented. Interestingly enough it was extremely volatile when the market was terrible in 2013, and volatile again when the market is insane like now.

I am one of those parents that would like to see their grandchildren live in a home that is owned. I have no problem helping the kids out with a down payment. I view it as our responsibility to an extent. We complained about affordability and house prices when we purchased, but the kids will step into a much harder market. Given that many parents who own in this area have a windfall of equity, are at peak earning power, and would hope their kids might stay close by, I don’t think the parental/grandparent offers with down payment/co-signor help will be cut off any time soon. That doesn’t mean that I don’t recognize that prices don’t go up forever and rates don’t usually stay low forever – unless you live in Japan.

Yes Leo S, but we have to wonder what likely caused that incredible jump in prices over such a short time span. Because it is totally out of character, to have a 14% increase in one month or two, in Victoria. And then can that event happen again?

Let’s say for the moment that this was due to CMHC changes and the bank of mom and dad stepped in and “gifted” a down payment of $100,000. For this price increase to happen again, then mom and pop are going to have to increase the gift to $200,000.

And personally I don’t think this $100,000 gift is going to last forever. Any benefits to the kids by a lower mortgage payment has been mostly wiped out by higher prices. So for the core housing market, I am of the opinion, that we might be looking at a trend of stable to decreasing prices for the rest of the year. And that is likely to be illustrated with declining month over month sales in the stand alone housing market in the core.

“realtors say letters, pictures and even baked goods are being dished out to curry favour – and get the sales.”

Won’t be long til the sellers are making cookies and writing letters to buyers. “Please buy my shack I overpaid by $300K and blew my family’s financial future.”

No rate hike by summer as US job report sucked bigtime, gold popping bigtime. How come not a mention of Victoria’s so called red hot job market Mike has been silent on since February ? Even the TC can’t bring themselves to even mention the word “jobs” in months unless it’s in a real estate pumping article with no stats to back it up.

The job growth here is on the decline last I looked since beginning of they year.

“50% drop completely within the realm of possibility”

http://www.bnn.ca/Video/player.aspx?vid=882958&hootPostID=a8e4ef331f90ba585949c52fdb783909

Michael, obviously real estate also likes it when there is no inflation too.

There has been trillions of dollars floating around the world due to Quantitative Easing. If that money had made it into the pay checks of the people then we would have had an incredible amount of inflation. Instead the money was locked in the vaults of the banks and spread out in mortgages as debt pledges.

Where did all those trillions of dollars from Quantitative Easing go. They went in your mortgage and your neighbor’s mortgage.

Quite ingeniously done. Houses are storing that QE money as big bags of inflation spread out among millions and millions of home owners.

The banks know that people will not sell their homes even if they owe more money on the mortgage than the home is worth as we all think prices will rebound. In fact the banks likely won’t give permission to sell. So we will keep on making those mortgage payments on an asset even when the debt is more than the value of the home.

And all that QE money created evaporates along with equity, but home owner’s still will pay that debt back to the bank.

Historically real estate has been seen as a hedge against inflation. However this time, real estate has been used to soak up all that inflation from QE and keeping most of the world out of a recession. Our house prices have already been inflated raising the interest rate won’t make them go higher.

True although it’s hard to say whether that will continue or if there will be a jump. When prices can jump from $650 to $740 from one batch of sales to another, I wouldn’t put a lot of weight on a few months of flat.

Prices may very well flatten out, but then we would see the MOI rise significantly at the same time.

I had my eye on 3119 Somerset as a non-view, non-prime location (within its neighbourhood – ie, not on Smith’s Hill) Hillside/Quadra house that had been fully renovated and had a suite.

Assessed: $432,400

Listed: $779,000

Sold: $865,000

That neighbourhood has seen gigantic price jumps in the last 2 months. The only other neighbourhood that has shocked me as much is Camosun.

http://www.pwccn.com/home/eng/tax_hk_stampduty.html

In Hong Kong, which is SAR of China, and where people from all over Asia use to park their money, this is the following tax regime for non residents. Note buyers are not just Chinese, but all of the rich in Asia.

The tax adds 20% to the price of property.

NOTE: 1MM$ CDN = 6MM$ CDN.

Rate hikes mean inflation, and real estate loves inflation. There’s a connection with 2016’s crazy hot market and the Fed starting a new rate cycle a few months back.

All 7 rate-rise cycles that we have historical data, witnessed our prices rise in tandem.

The cycle most similar to today saw mortgage rates go up 40% over a period of 3 years as prices rose approximately 50%.

Unless it’s different this time.

“In ultra-competitive Victoria, house hunters aim for the heart”

http://vancouverisland.ctvnews.ca/in-ultra-competitive-victoria-house-hunters-aim-for-the-heart-1.2929261

“realtors say letters, pictures and even baked goods are being dished out to curry favour – and get the sales.”

Rate hike. Yeah right – RBC was giving me a .35 spread on fixed vs variable over 5 years at renewal. They’re betting on less than 2 increases over 5 years, unless you believe that they’ll reverse at the same .15 they came down on. Sure.

Rate hikes won’t do much to the Dunbar retiree who’s selling at 3 and buying at 1. They’re hoping for a rate increase, because that 2m in cash is going to rot otherwise. I’m not saying that’s the whole market, but it’s part of it.

Affordability is often gauged here in terms of SFH. It’s entirely possible that SFH becomes unaffordable for most and that the market doesn’t correct for that. Instead, the market builds higher density. We’ll see.

Rate hike? Please provide evidence that we will have a meaningful mortgage rate hike in the near future.

Beside saying “why wouldn’t it?”, you did not answer why a luxury tax would slow down Victoria’s <$1.5 million market. Our market is not being pulled up by higher-end homes. The fierce competition has been in the non-luxury market.

@ VicInvestor1983: why wouldn’t it? Combine that with the upcoming rate hikes, and we could have quite the change in the market. Don’t assume these price increases will go on forever.

@Bizznitch: how is a luxury tax on homes >$2million going to slow down the craze in our $500K-1.5 million market?

I’ve shown the data by month and by grouping of 500 sales and the data didn’t vary.

House prices in the core are not appreciating at a faster rate. They are slowing down.

That may be different for condos in the core or houses in the Westshore and Peninsula and that’s why the overall numbers might look different.

And the number of house sales in the core was 10 percent less in May than in April of this year. And that is different from last year when sales increased between May and April in the core.

Sales, Number of

Mnth 2015 2016

Jan 90 122

Feb 164 228

Mar 231 318

Apr 235 377

May 284 340

Thanks everyone who responded. I think maybe we will hang on until spring. Worst that happens is prices go down and we don’t sell at all and we are okay with that. Although I have to say the house seems the type to get bid up right now when looking at the other high sales (area, fully renovated, large 6 bed 3 bath, 200 amp, new kitchens and bathrooms, professionally sound proofed suite with it own laundry and electric meter) but it would mean spending time improving the landscaping over the next couple of months and making sure it is all perfect. I’m surprised prices have risen so much and was prepared for a much lower roi so I’m more relieved at not feeling rushed with it all than I am worried. But still a bit concerned there won’t be a better time than now. I like the idea of only needing to show it for a couple days..

Here’s a good one…

http://globalnews.ca/news/2738797/feds-considering-luxury-tax-on-foreign-buyers-of-multi-million-dollar-homes/

Might be a good time to sell if you subscribe to the notion that the Chinese are flying in here via Airbus A380 to buy up whole neighbourhoods sight unseen. 🙂

I know Mike, I know. 😉

Did you catch the 6 o’clock Global news from Vancouver Mike? Banks are worried about the bubble popping and crashing. National Bank now calling for higher down payments like Scotia wants.

The tone of the news and statements from lenders and the usually hard core bull pundit housing pros like Somerville they trot out has clearly shifted negative. Lots of massive household debt talk as well.

Not what you see at the beginning of a bull market but at the end. Keep on clicking your heels together hoping for your 40%.

Hawk, you’re the greatest 🙂

JJ, I agree that conclusions can vary depending on how you slice and dice the data.

Just IMHO I don’t think that 500-block increments define better quality or quantity of data – because, for me, it misses important milestones in the year that affect demand & sales prices for SFHs. Christmas is a good example, along with long weekends & summer holidays.

I probably shouldn’t have said seasonal factors are the “biggest” impact because I agree that political & economic factors determine long term trends.

But seasonal factors always modulate the signal, whether that signal is drifting lower or higher in the long term. If someone were looking to buy a home, I just hope they’re aware of this pattern that prices & demand typically follow over the course of each calendar year, so they don’t panic in the spring rush.

http://www.timescolonist.com/news/local/greater-victoria-housing-prices-expected-to-keep-rising-through-2017-1.2269353 Prices to continue up.

From the previous thread:

Every city has nice people. Not every city is a giant shit-hole located in the middle of nowhere.

Also, no one has ever said it was their dream to retire to Edmonton.

Funny how since Scotia announced the mortgage lending is getting hacked back due to high risk, Mike has been posting his little charts and numbers out of Vancouver like a mad man. Paranoia much ? Maybe his clients are getting antsy and want to dump. 😉

As the CEO stated:

“It is not sustainable and I don’t think it is healthy, there is a bit of an aberration here. I know OSFI (the bank regulator) is concerned about it, the CMHC is concerned about it, the Department of Finance is concerned about it… so I think there are more things the government can do.”

totoro, if I were in your shoes, I’d hang on to the property until next spring — unless there are overriding personal reasons to sell sooner.

Totoro,

If you’re going to put the tenant’s needs ahead of your own needs, then why even think of selling. If you think in a year from now the market will be slower, rentals will increase to help out your tenants, the dumb over bidders will be long gone and you miss out on the easiest $200K ever, then sell.

We’re one step away from new foreign investment laws that will expose all the money laundering in this province, not to mention the high possibility the Chinese markets crash on their own.

Here’s the yearly leader #s for Van:

Tsawwassen 48.2%

Richmond 45.7%

Burnaby E 41.1%

Coquitlam 40.6%

Burnaby N 40.4%

Ladner 40.2%

PoCo 40.0%

I think I’m now convinced Vic will reach the 40+% club.

Wow, even westVan condos are now pushing 40%.

@Totoro, Personally I would hang on to the house and see what happens next year. Unless there is a black swan event I just can’t see the market taking a serious dive in the next year or so. It will likely slow down a bit, but will prices in a year be less than now? Incredibly unlikely.

Infographic summary of the Vancouver insanity:

http://www.visualcapitalist.com/vancouver-real-estate-mania/

Totoro, I don’t think there is any rush to sell your home in Saanich East. The market conditions are all in your favor. The only thing you might not be able to capitalize on, might be some of the outlandish over bids.

The crazy over bids are a small segment of the marketplace and it would be necessary to look at your specific property to determine if it would go to multiple bids well over asking price. Averages, medians and the HP Index won’t help you on that.

You need to have the right house in the right hood. And the right agent.

Vicbot the grouping is using blocks of 500 sales not by months.

A month to month comparison is what I was INTENTIONALLY avoiding. Instead I’m comparing blocks of 500 sales to the previous group of 500 sales.

You missed the point I was making about quantity versus quality of data.

As you mentioned there is usually seasonal variations but not always. And like this year prices started to appreciate much sooner than what is traditionally the spring market. Man has moved over the centuries away from the solar cycle that governed our planting and harvesting times. We live in artificial sunlight and we can eat bananas is the winter so what happens in a spring and a summer market can vary considerably from one year to the next. Political, economic and social factors are more of a determinate than the season..

What sparked all this giving across Canada at the same time?

I think we would have to look at changes made to CMHC and Genworth making it more difficult to obtain high ratio financing around that time. That may have prompted the parents or grandparents to step in.

And yes I’ve noticed the new baby syndrome by parents and grandparents. I suppose up until the baby is born most consider the millennials as just playing house and getting funky Celtic and Haida tattoos.

I noticed this in a coffee shop the other day. The grand-parents were sitting with the millennials and a new baby. Obviously it was the wife’s relatives because the husband was shut right out of the conversation about improving the home “they” just bought. He did his part and donated the sperm and he can keep quiet now. But the house is the security for the wife and the baby.

I was mentally urging this male millennial to stand up for himself but I only heard the clink clink sound as his balls fell off and rolled under the table. And I thought how meddling parents and grand-parents that footed the down payment will come between him and his wife. Those that control the purse strings control the world.

JJ, interesting analysis. That grouping of months is unusual, though, ie., Jan-April 2015 (4 months), then 3 month periods until Feb 2016.

It’s a 14 month period instead of a 12 month period, and not based on quarterly, monthly, or seasonal data.

In some cases, your months start at the 7th & end on the 14th, but others months may start on the 22nd & end on the 12th. That’s not standardized because a lot of monthly sales are finalized on the last day of the month (Feb 28, Apr 30), regardless of Pend Date, to standardize data collection.

If you divide it up Jan-Mar, 3 month periods until December, and start-to-end-of-month sales, you’ll come up with a different set of medians.

The reason I mention this is because I’ve seen analyses on seasons & they seem to have the biggest impact on buying behavior: the school year, weather & daylight hours (even in Victoria). September definitely starts to slow down with SFH sales because parents are busy with kids.

Then buyers really only come out in force after Easter.

If people had access to more sales data about types of SFHs they’re interested in, they could do their own monthly or yearly trend analysis. That’s why the competition ruling on TREB is going to be interesting!

From JJ: “And if you give to one child, then you have to be fair to the others at the same time.”

That’s funny. I know of a couple who have just, what they call invested together, in an investment property with one of their sons. The son and his wife live in it. The other son heard about this and now he’s jealous and doesn’t talk to his family.

And @LeoM, No kids yet, but probably in the works.

The parents felt that the jealous son doesn’t really need the bank of Mother and Father as he basically married into money.

-Man! How money always seems to ruin things in our modern society. When can we do away with the monetary system?!?

JJ– regarding those inter-generational gifts from parents to their children; I’ve noticed with the people I know, that downpayment gifts only happen after the grandkids are born. I don’t know any parents who gave the downpayment gift when their adult children were just a ‘couple’ who were renting; but I know several parents who kicked in a substantial portion of the downpayment after grandkids were born. Seems that grandparents want their grandkids living in an owned home.

A little more dribble for Michael to contemplate.

The problem has always been one of quality over quantity.

What I’m measuring is just the single family market in the core districts. That is very selective rather than a composite of all areas and all types of properties.

A month to month analysis may be deceptive since the volume of sales can drop off or increase significantly and that increases the error. That’s why a running three month median or longer provides substantially more data and accuracy. But that also tends to mask what is happening to prices on a shorter time span.

A better way may be to group the sales in blocks of 500 sales for detached homes in the core districts.

01/22/2015-04/12/2015 the median was $615,000

04/13/2015-06/06/2015 the median was $630,000 for a 2.4% increase

06/07/2015-08/14/2015 the median was $629,000 for a 0.2% decrease

08/15/2015-11/05/2015 the median was $655,000 for a 1.0% increase

11/06/2015-02/19/2016 the median was $650,000 for a 0.7% decrease

02/20/2016-03/07/2016 the median was $742,000 for a 14.2% increase

03/08/2016-04/18/2016 the median was $751,000 for a 1.2% increase

04/19/2016-06/02/2016 the median was $755,000 for a 0.5% increase

After an initial spike in house appreciation in the core around February to March this year appreciation has slowed to what we experienced last year. The difference between today’s market and this time last year is that we are in an extreme sellers market. That’s making me go Hmmmmm? Why are median prices still not hurtling to the moon?

The year over year increase went from $630,000 to $755,000 or 19.8%. If the median remains unchanged at around $750,000, as the median for the last 1500 house sales in the core seems to indicate, then the year over year increase would decline to 15% as we compare the fall market at $650,000 to a projected fall market this year at $750,000.

A $125,000 difference between then and now is likely due to bigger down payments. Perhaps an inter-generation “gift” . Parental love for their children may be unconditional but this is about money. The parents are possibly siphoning off $125,000 in their home equity to “give” to their children. And if you give to one child, then you have to be fair to the others at the same time. That means there is a limit to parents gifting and that might be why median prices for stand alone houses in the core districts have leveled off.

https://youtu.be/Abx45Ozceko

Totoro, just in general, if it were me, I wouldn’t sell after July of any year, whether it’s a bull or bear year. But you know your situation better than I do. I always use spreadsheets to make decisions, with scores for pros & cons, if that helps! 🙂 If you need the equity for something else, then that is a good reason to use this time to sell. (prices are unpredictable, can go up or down). If you tried to sell and you didn’t find offers that you like, you can always decide not to go through with it.

Totoro, only you know if it’s the right time for you to sell; but a well known billionaire stock investor is quoted as saying; “I made my fortune by buying late and selling too early.”

It would be neat to see a something like a 30-year composite of Vic price velocity to see what month we normally decelerate. For instance 2015 it looks we hit our seasonal deceleration in April.

Just so we are clear. Victoria core market is up 20% in 8 years. West shore is probably flat. Up island flat/ down. Real big bubble going on here.

We are thinking of selling a house in Saanich East and have been considering it for about a year – before the market went crazy! We don’t need to, but there are some other things we would like to do with the equity. We’ve held on because we are concerned about the tenants finding something else and the hassle of getting it ready to show, but we’ve talked with the tenants and they’re okay with it and can’t afford to buy it themselves. I’m interested in opinions on whether we should hold onto it longer or sell in the next few months. What would you do?

To be fair to you Hawk, I will say that although I don’t agree with you 100%, you do provide a valuable view that is particularly valuable to young people who want to buy into this crazy market. Without your views there would be too many voices saying “This is a great market and sustainable for another two years!” It’s not sustainable.

Agreed. I think a tool with those metrics applied across regions would be useful.

I don’t see it. When people can’t buy in Vancouver Vancity doesn’t make money.

Sorry to burst another of your fantasy bubbles Hawk, but I’m not leveraged at all, no mortgage, zero debt, and good cash flow. I’m too old for any risk.

Note the price acceleration is comparing this month to 3 months ago. If we look at just month to month acceleration, then there is a slight deceleration from April to May. So there is an argument to be made that at the leading edge, price acceleration is reversing, but that chart tends to swing wildly enough I think it ended up being more noise than signal.

Love the price velocity & acceleration chart additions. They may even decelerate Jack’s daily decelerating dribble 🙂

The video showed the pathetic situation Vancouver and Victoria is in. Past government policy has created a time bomb that could explode at any time. It’s a one trick pony of foreign money that can be turned off with the right legeslation which I believe the Feds will do soon.

Those over leveraged like LeoM who rant about nothing and refuse to acknowledge this is not an economic expansion built on a normal business cycle like back in early 2000’s. It’s a Vegas crap shoot.

A big 5 bank who lends major mortgage money just took a major shot across the bow that the party is over.

Credit lending is tightening yet the bulls are too arrogant to get it. Banks don’t pull back on lending at the early stages of a bull market.

BTW: Triple A rated’s post yesterday deserves a sticky on how to buy a home. That post is absolutely mint.

“For those who missed it in the comments, this Vice video posted by Hawk on Vancouver real estate is worth a watch.”

It’s just an extended advertisement for Vancity. The “Calling all the dreamers” approach is bait; the video is just an extension with a “take back the city” tone and a splash of fear thrown in.

Vancity are happy every time someone signs over their financial freedom and future. And with this kind of advertising, they are also quite happy to fuel the fire. Total bullshit, my apologies admin – I see this video through a different lens.

Push for more transparency gets Vancouver realtor thrown off the professional standards board. http://www.theglobeandmail.com/news/british-columbia/oversight-of-british-columbias-housing-market-is-a-sham/article30227434/

I think the real estate industry is at serious risk of having their privilege of self regulation revoked, and they seem to be doing nothing to avoid it.